Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMore UK stocks have exposure to Russia than you think

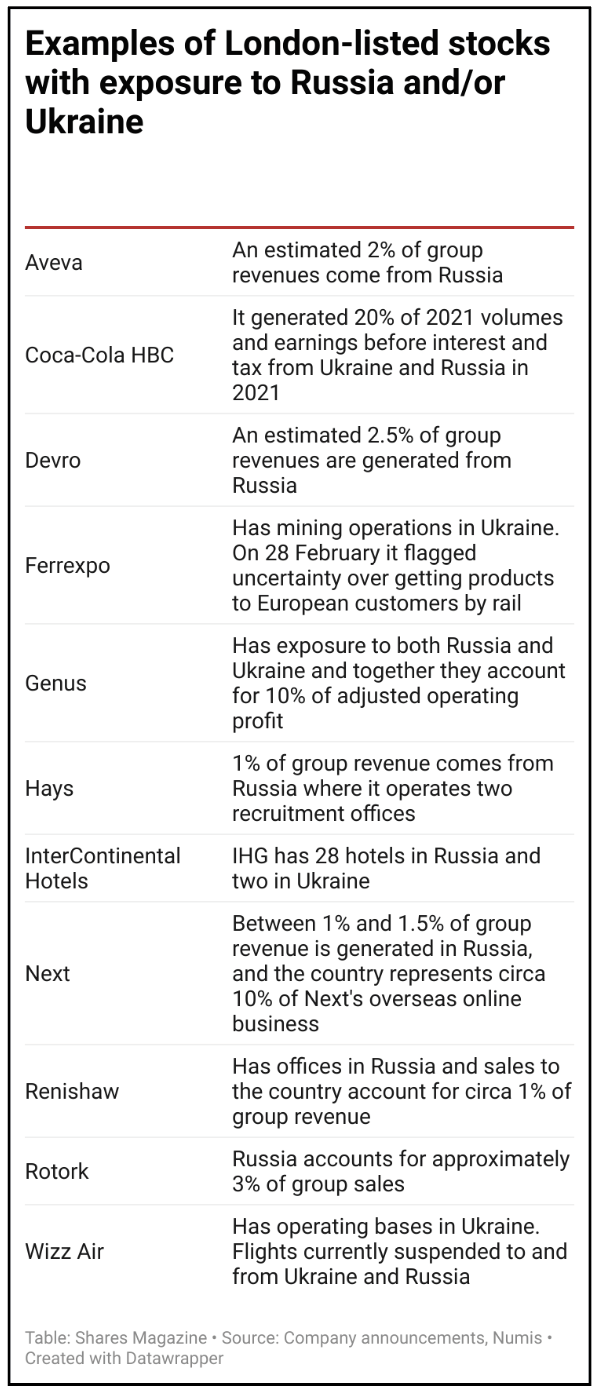

The advent of globalisation has helped to drive considerable earnings growth for companies on the UK stock market thanks to them doing business with an ever-growing number of countries. Unfortunately, widespread geographical expansion means the list of UK stocks with exposure to Russia is bigger than you might think.

Many professional and retail investors have raised a moral objective to having money in Russia-related investments and have been pulling out of various stocks since the country launched a full-scale invasion of Ukraine on 24 February.

Some of the worst hit stocks have had the bulk of their operations and assets in Russia, such as miner Polymetal (POLY) and Raven Property (RAV). Others have taken pre-emptive moves to distance themselves from the country, including BP (BP.) and Shell (SHEL).

We’re now at the stage where investors are looking closer to see which other stocks have exposure to Russia. Selling goods or services in the country, or sourcing product from it, could be viewed negatively by Western investors and therefore weigh on the share price.

Even those who do halt business in Russia still have to contend with likely downgrades to earnings forecasts, something that has historically driven down a share price.

ASOS (ASC) is best known as a seller of clothes in the UK and increasingly the US. Less appreciated is that fact that Russia has been an important sales region for the business. On 2 March the company announced that it had suspended sales in the country, having already done the same in Ukraine where it became ‘impossible to serve customers’.

The retailer says Russia and Ukraine represented 4% of group revenue in 2021 and contributed approximately £20 million to group profit. ‘The territory has always been relatively profitable (implied contribution margin 13%) given the VAT advantage and very low returns rates,’ says Jefferies analyst Andrew Wade about ASOS.

It could miss out on £7 million in profit and £85 million in revenue should the two countries be off limits for sales for the next six months, according to Wade. The key question is whether this is a short-term issue or whether ASOS will decide to stop selling completely to Russia permanently.

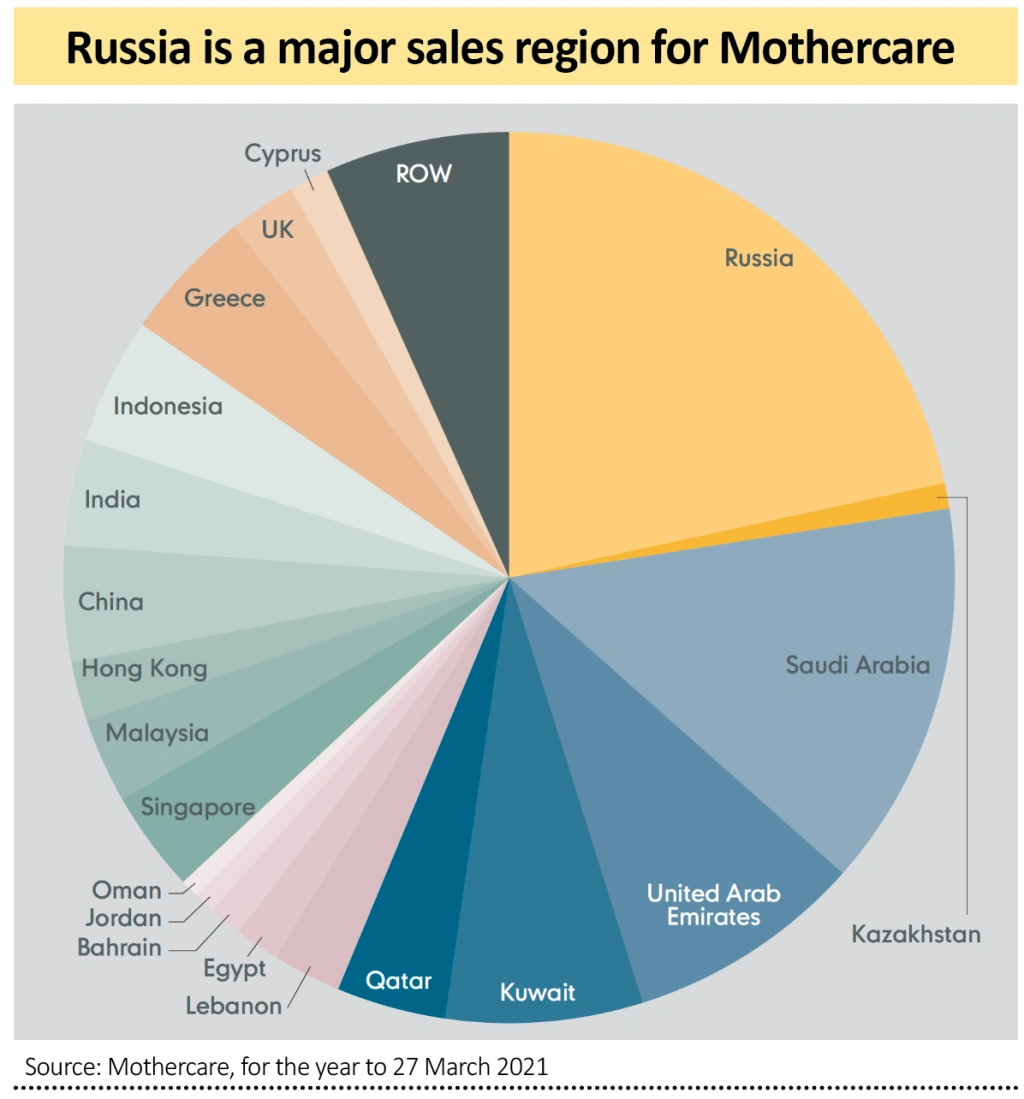

Also exposed in the retail sector is Mothercare (MTC) which announced on 9 September it had suspended its Russian operations, with an expected hit to annual profit of £6 million. It has changed shape as a business in recent years, with the closure of its UK physical stores and a greater emphasis on overseas operations via franchisees. Russia hasn’t been one of its best performing regions of late, but it still accounted for one fifth of the group’s global retail sales in its 2021 financial year at £77 million, according to stockbroker Numis.

FTSE 100 packaging group Mondi (MNDI) says its Russian operations have generated about 20% of the group’s underlying earnings over the last three years. Unlike many Western companies which have halted operations in Russia, Mondi says it continues to operate in the country. It has, however, suspended production at a paper bag plant in Ukraine.

Car distributor Inchcape (INCH) derives an estimated 9% of group revenue and 4% of group earnings from Russia, says Numis. ‘With revenues and costs locally denominated, weaker currency would present a headwind to earnings. The weaker currency and any potential trade embargoes are also likely to impact the demand for imported new vehicles which Inchcape over-indexes in and we would estimate new vehicles account for c.35% of Russian gross profits,’ adds the broker.

AG Barr (BAG) holds the secret to one of Scotland’s most-prized drinks, Irn-Bru. While Russia is not mentioned in its most recent set of half-year and full-year results, the drinks company does sell into this territory. An article published 20 years ago by the BBC said at the time Irn-Bru was the third most popular soft drink in Russia, with its popularity perhaps down to it resembling old Soviet-era drinks.

Russia is one of AG Barr’s only export markets for Irn-Bru, where it typically sends syrup to a local bottler and receives a royalty on sales. Numis says this accounts for less than 1% of group revenue, so not meaningful to its finances but there is still a risk of being associated with this sales territory.

There are reports that some people in the US are boycotting drinks brands which they wrongly perceive to be Russian. This includes Smirnoff vodka which is owned by UK drinks group Diageo (DGE).

FUND MANAGERS COULD BE VULNERABLE

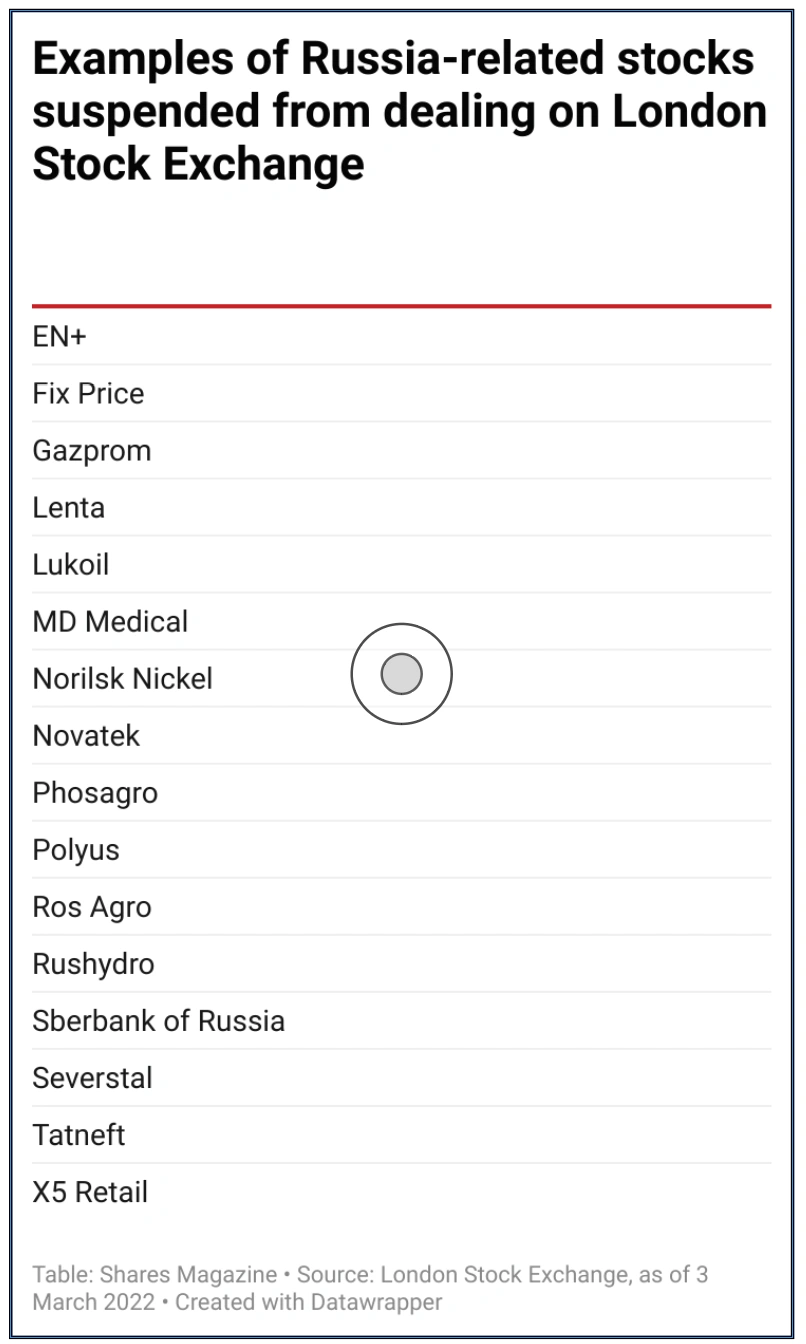

Investors are likely to look hard at their portfolios and question if they want to continue with exposure to Russia given its current actions. Several Russia-focused funds have already suspended dealing including Liontrust Russia (B86WB79) after the temporary closure of the Moscow Stock Exchange and the temporary ban on foreign investors selling local Russian stocks.

Emerging markets-focused fund manager Ashmore (ASHM) is at risk of seeing outflows from some of its funds given that an estimated 4% of assets under management were exposed to Russia and a further 4% to Ukraine as of January.

In other sectors, EKF Diagnostics (EKF:AIM) generated 3.6% of its sales and 3% of operating profit in the first six months of 2021 from Russia via its laboratory diagnostics business. Expect more details on any impact to its business when it reports full year results on 29 March.

From an ownership perspective, it is worth noting that TUI’s (TUI) largest shareholder with a 34% stake is Unifirm, controlled by Russian billionaire Alexei Mordashov. He has been hit by sanctions from the EU and on 2 March resigned from TUI’s supervisory board.

While the sanctions have no impact on TUI as a business, the company’s association with Mordashov might not go down well with other shareholders who have a moral objection to Russia.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.