Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDoes a 60/40 portfolio work in the face of rampant inflation?

For much of the past five decades a conventional balanced portfolio made up of 60% shares and 40% bonds has served its purpose.

The rationale behind this approach has been that bonds cushion volatility and provide income, and act as a counterbalance during a bear market. Conversely stocks provide the capital upside during a bull market.

More recently the two asset classes have become more correlated and the income available from bonds has fallen significantly.

In recent decades the confluence of several drivers including ageing demographics, globalisation and the re-emergence of China as an economic powerhouse have acted as a brake on inflation.

This has circumvented the need for central banks to be concerned about rising consumer prices. Consequently, recent economic history has been characterised by low inflation and declining interest rates. This has benefited bonds.

As yields have fallen bond prices have risen – there is an inverse relationship between interest rates and bond prices, as interest rates decline the price of a bond will rise.

Given the resurgence of rampant inflation within the UK and America, it appears we are entering a new economic regime, where these conditions could reverse.

The Bank of England has already implemented two successive interest rates rises and the Federal Reserve in America looks set to follow suit imminently, notwithstanding the war in Ukraine.

This new economic environment of rising interest rates and high inflation means it is important for investors to re-evaluate the suitability of the 60/40 portfolio model.

WHY 60/40?

Historically on average when equities have fallen the price of bonds has gone up, so holding both asset classes has smoothed out volatility; 60% shares and 40% bonds quickly became accepted as the benchmark for a moderate risk portfolio.

And it has largely done the job, particularly given the strong run for bonds. Look at the performance of the Vanguard LifeStrategy 60% Equity (B3TYHH9) fund – which is set up as a classic 60/40 portfolio with exposure to stocks and bonds through a basket of Vanguard funds.

In the past 10 years it has delivered an annualised return of 7.7% compared with 6.1% for the FTSE 100 and FE Fundinfo data shows it has a beta of 0.78 for the last three years. Beta measures how much an investment moves when the overall market rises or falls by 1%, so a beta of 1.5 would see an investment move 1.5% for example.

The beta on this fund shows it has been less volatile than the wider market and therefore lived up to its portfolio protection credentials.

IF IT AIN’T BROKE, WHY FIX IT?

Given its successful track record, investors may naturally ask why not stick with this formula?

Phil Huber, chief investment officer for wealth management firm Savant Capital, provides a clear response in his book, The Allocator’s Edge.

He says: ‘There is a high probability that the 60/40 portfolio that worked tremendously in the past will ultimately fall short in meeting the return targets and objectives of investors in the decades ahead. There are two main culprits to blame here: high valuations of the 60%, and paltry rates on 40%’.

Hubert outlined the potential risks of having a 40% weighting in bonds: ‘As of March 2021, the 10-year Treasury rate sits at around 1.5% (a year later it is 1.8%). This is materially higher than the low of 0.52% reached in 2020, but still historically low.

‘Assuming realised inflation of 2%, investors are set up for negative expected real returns for an asset class that has historically acted as a ballast against equity volatility and generated mid-single-digit returns in the process.’

Hubert’s comments have proved to be prescient, given that the personal consumption expenditure price index which the Federal Reserve uses for its inflation target jumped 6% in January from a year earlier, according to a recent Bloomberg survey of economists.

Charles Hovenden, portfolio manager at Square Mile, echoes Hubert’s sentiments regarding the potential overvaluation of bonds, but within a UK context. He suggests the magnitude of this valuation anomaly can be determined by comparing bond yields the last time the economy was in a recession.

Amid the 2007-8 global financial crisis yields on 10-year UK government bonds were closer to 5% than the current 1%.

The answer to what replaces 60/40 is not necessarily a straightforward one. For some it involves increased exposure to stocks and shares, however others have turned to alternative assets like property, commodities and infrastructure, opting for a mix of 45% stocks, 25% bonds and 30% in alternatives. Below we look at some options for investors looking to diversify a traditional 60/40 portfolio.

DIVERSIFICATION OPTIONS

– REAL ESTATE –

Real estate as an asset class warrants a place in a diversified portfolio. The case for strategic allocation to property is strong given the benefits of capital appreciation potential, coupled with inflation protection and an income stream.

As well as helping you to achieve diversification, a fund or listed property firm can provide access to a wide variety of different types of property including shops, offices, warehouses, homes and alternative assets like healthcare facilities and student accommodation.

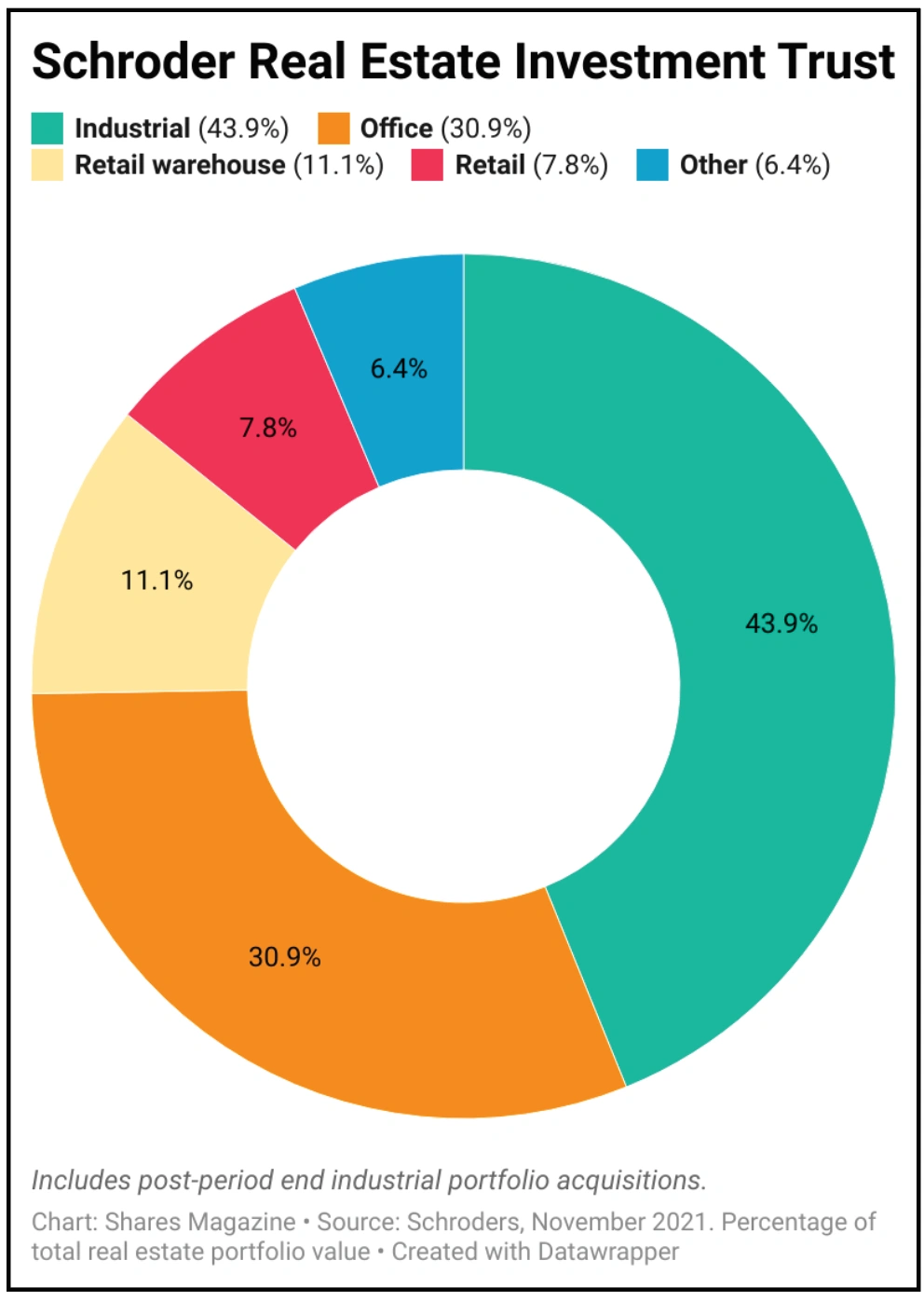

For example, Schroder’s Real Estate Investment Trust (SREI) has 73% of its portfolio in industrial and office assets and its retail holdings include almost zero exposure to structurally challenged shopping centres.

The real estate investment trust is trading at a 21.7% discount to net asset value, and offers a 4.3% dividend yield.

Nick Montgomery, Schroders’ head of UK real estate investment, is focused on so-called ‘Winning Cities’ – urban areas with characteristics that will make them attractive places to live and work in the long term.

– INFRASTRUCTURE –

Infrastructure assets are another way to diversify a traditional 60/40 equity/bond portfolio. They offer high barriers to entry, relatively inelastic demand and are typically resilient to economic cycles. They also generate relatively stable and predictable cash flows and have a positive correlation to inflation.

Pantheon Infrastructure Investment Trust (PINT), which came to the market in November 2021, targets an 8% to 10% annual return. It is diversified across different types of infrastructure assets. In comparison, many other infrastructure trusts listed on the London Stock Exchange specialise in either government-backed projects or renewables.

Pantheon’s focus is on investments in infrastructure businesses that provide essential services to the public including assets such as mobile phone towers. The asset manager is an established global investor with long standing relationships with leading private market infrastructure investors.

It invests alongside these partners to construct a diversified portfolio of direct co-investments in five different categories. These are utilities, transportation, social infrastructure, digital infrastructure and renewable energy.

The trust currently trades at a 7.65% premium to net asset value, which reflects the current demand for infrastructure assets.

– MULTI-ASSET FUNDS –

If bonds will no longer cut it in an inflationary world, investors need to transition into an array of alternatives which include inflation-linked bonds or gold, as well as property, infrastructure, carbon credits and commodities. Multi-asset funds are an option for investors who want exposure to these types of investments under a single roof.

In September 2021, Ruffer launched the LF Ruffer Diversified Return Fund (BMWLQT5), aiming to generate positive returns in all market conditions. It states: ‘We try to first protect, then grow the value of the fund. If we can do this, we should outpace inflation, protecting and increasing the real value of our investors’ income and capital.’

Co-manager Duncan MacInnes believes we are entering a world in which bond and equity prices look poised to fall in tandem. He says: ‘In this environment true diversification and a lack of correlation to other asset classes or strategies will be absolutely vital to portfolio construction.’

From an asset allocation perspective index-linked gilts feature prominently in its portfolio, as do gold and shares in gold miners. The largest equity holdings include Shell (SHEL), NatWest (NWG), BP (BP) and GlaxoSmithKline (GSK).

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.