Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTesting times: What the Ukraine crisis means for investments

For now, the escalating conflict in Ukraine shows no signs of easing. After the initial shock, markets were hopeful the economic impact of the war might be contained as the West’s opening salvo of sanctions in response to Russia’s invasion (24 Feb) were weaker than some had anticipated.

However, any relief soon dissipated as Ukraine put up stiff resistance against the Russian invaders and sanctions towards Russia became much more punitive.

Sentiment wasn’t helped by Vladimir Putin’s decision to place Russia’s nuclear force on high alert. This appeared to be a message to the West to not go any further in its intervention in Ukraine, using the country’s nuclear arsenal as leverage.

However, even if the move is only intended to send a message it heightens risks of a nuclear clash to levels arguably not seen since the 1980s.

BAD FOR CONSUMER SENTIMENT

This is unlikely to be constructive for consumer sentiment which is already weakening amid pressure on personal finances from a rising cost of living.

Disruption to energy and food supplies, with Ukraine and Russia accounting for a large proportion of the world’s supply of wheat, corn and vegetable oil, will only add to inflationary pressures. The region also produces a significant quantity of rare earth metals used to manufacture already scarce semiconductors.

HOW WILL CENTRAL BANKS REACT?

This puts central banks in a fix as they look to balance the need to control rising prices with a potential role in easing the economic impact of the Ukrainian conflict.

Phil Milburn from Liontrust Asset Management’s fixed income team told Shares the bond market has reduced average expectations for US Federal Reserve rate hikes from 7 to 6.3 increases in 2022 and the chance of 0.5% rise in March has fallen from 50% before the invasion to around 25%. Milburn added that the impact from rising energy prices meant peak inflation would be extended by a couple of months.

US VERSUS EUROPE

Arguably the US is better placed than Europe to weather the current crisis. Seema Shah, chief global strategist at Principal Global Investors, notes that while trade with Russia is negligible for both, as a net energy exporter, the US is less vulnerable to a rise in oil and gas prices.

Shah adds: ‘Europe, however, is a net importer—over 40% of EU gas and 20% of EU oil originates from Russia. Any disruption to the supply of oil and/or gas will have a significant impact on energy prices across Europe and, therefore, on growth and inflation, leading to a preference for US based investments.’

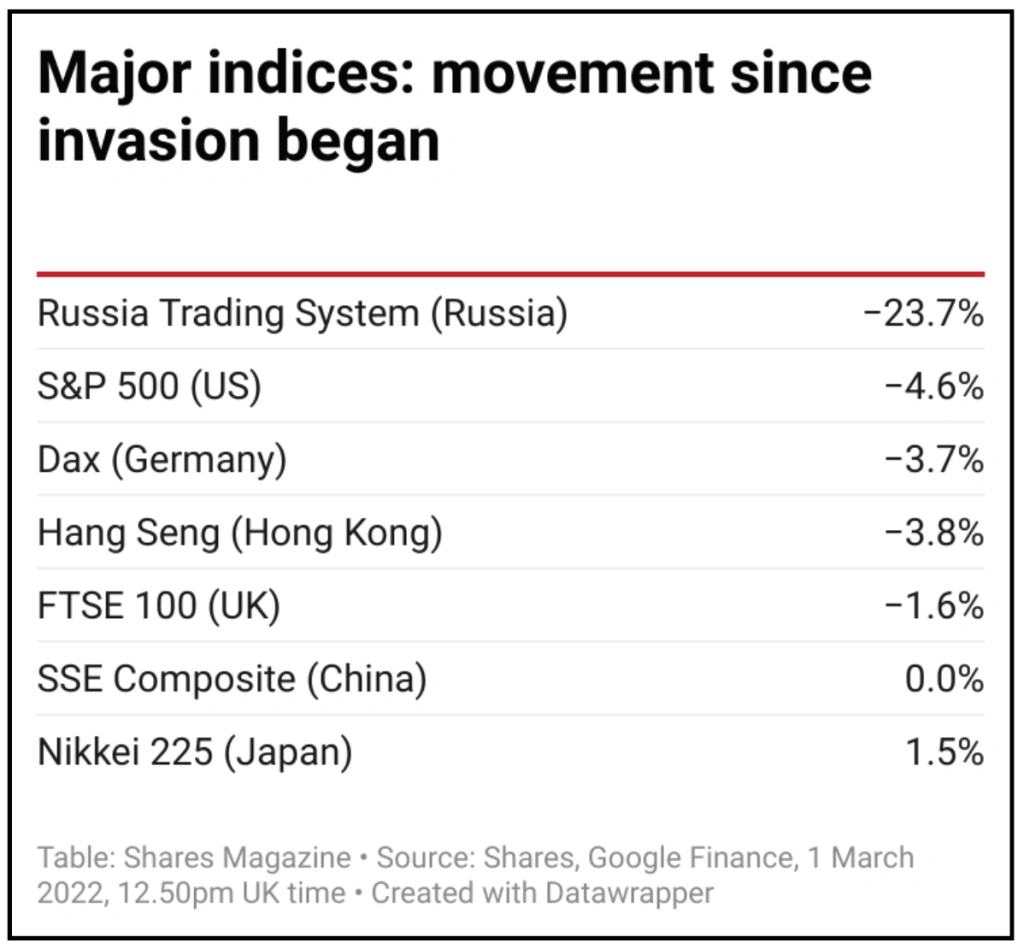

WHICH SHARES HAVE DONE WELL DURING THE CRISIS?

Commodity producers and explorers, cyber security experts and defence companies are among the best performing stocks since the market close on 23 February, being the night before Russia kicked off its full-scale invasion of Ukraine.

Disruptions to supplies of oil, gas and iron ore have pushed up the respective commodity prices and served to also raise the value of relevant companies, including Zanaga Iron Ore (ZIOC:AIM) which is up 73%.

Cyber security threats became elevated as soon as the conflict broke out, which explains why shares in cyber expert Darktrace (DARK) have jumped by nearly 30% in less than a week.

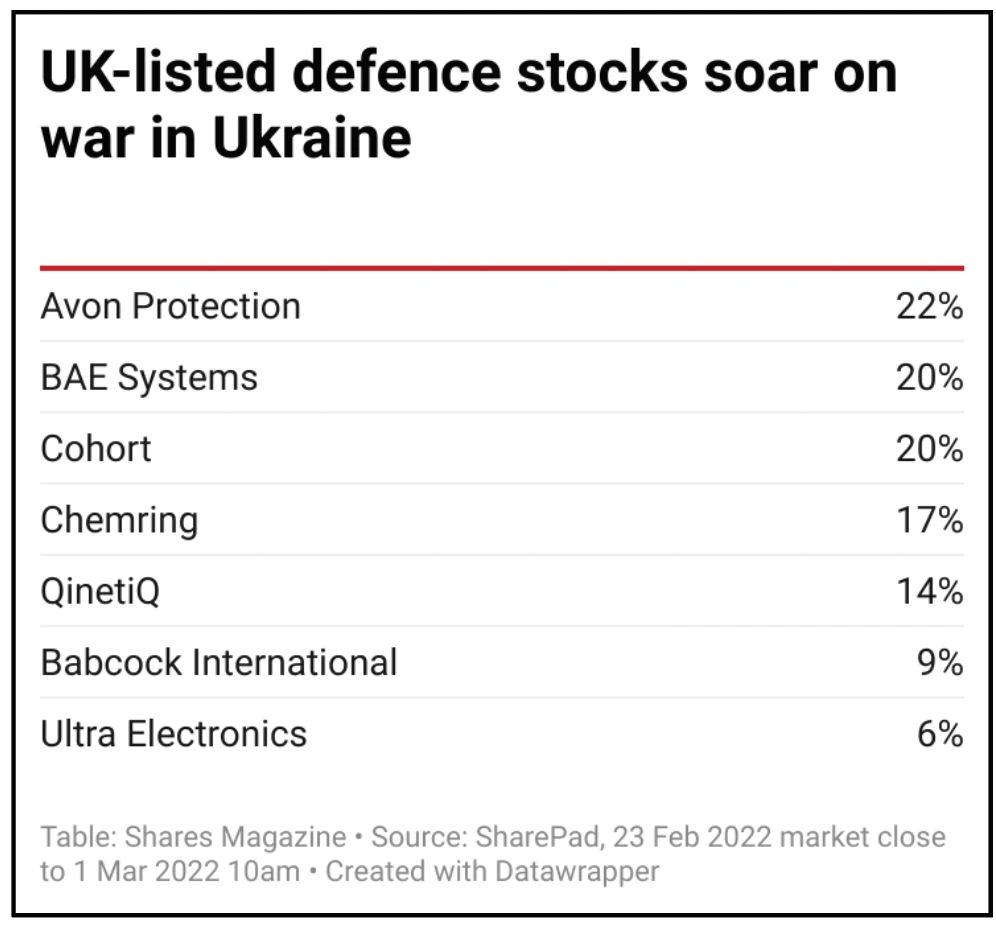

HOW HAVE DEFENCE COMPANIES FARED ON THE STOCK MARKET?

A Russia-related shift in the calculus for European countries when it comes to defence spending has seen a share price surge in defence companies.

In some ways this was predictable but the extent to which countries like Germany, which has committed to meeting the requirement for NATO members to spend 2% of GDP on defence, have changed tack seems to have surprised the market.

Jefferies analyst Chloe Lemarie comments: ‘For all NATO members to reach 2% of GDP spent on defence would imply a 25% increase overall, excluding the US, which would trigger significant benefits across the entire industry.

‘Outside of NATO, Sweden, Finland and Eastern European countries also appear likely to drive a significant acceleration in defence spending in coming years,’ Lemarie adds.

On the UK market, Avon Protection (AVON), BAE Systems (BA.) and Cohort (CHRT) have all increased by approximately 20% in value since the Ukraine invasion began. Overseas-listed companies either in the defence sector or with customers in this space have also been in demand, including Rheinmetall (+49%), Thales (+30%) and Leonardo (+29%).

WHAT DOES THE CRISIS MEAN FOR BP AND SHELL?

Both BP (BP.) and Shell (SHEL) have unveiled plans to sever their ties with Russia. BP’s interests in the country were more direct and material.

Its 19.75% stake in Russian producer Rosneft was a significant contributor to earnings and cash flow, accounting for 17% of its preferred measure of profit in 2021. Investment bank Jefferies had estimated BP would bank a $1.6 billion dividend from Rosneft in 2021, 6% of its forecast cash flow.

Non-cash impairments of up to $25 billion could be taken in BP’s first quarter results on 3 May with a sale back to Rosneft emerging as the most likely way the company can realise any value from its stake in the Russian business.

Shell is selling out of its 27.5% interest in the Sakhalin 2 gas development and will also face write-downs, with its Russian assets valued at around $3 billion at the end of 2021.

BP and Shell have been praised by the public and investors for taking swift action in cutting ties with Russia, despite the financial setbacks caused by their actions.

HOW HAVE DEFENSIVE STOCKS HELD UP?

Traditional defensive stocks like utilities National Grid (NG.), SSE (SSE) and United Utilities (UU.) as well as healthcare products provider Reckitt Benckiser (RB.) and groceries-led retailers like Sainsbury’s (SBRY), Tesco (TSCO) and B&M European Value Retail (BME) have held up well since Russia launched its invasion, most of which have seen positive share price movements.

Whatever the backdrop people will still need to power their homes and businesses, look after their health as well as purchase food and sundries.

HOW HAVE FINANCIAL TRADING COMPANIES PERFORMED?

War creates fear, volatility and uncertainty. Intuitively, one might expect the cohort of online trading exchanges to benefit from this environment as investors trade more to adjust their portfolios to the changing circumstances of war. Share movements imply it’s not so clear-cut this time, perhaps suggesting that day traders are too nervous to play the markets given the crisis is still unfolding.

Plus500 (PLUS) is down 5.6%, IG Group (IGG)

has fallen by 1% but CMC Markets (CMCX) has risen by 3.2%.

HOW HAVE CAPITAL PRESERVATION FUNDS PERFORMED?

Investors seeking safety amid the recent market rout would have generally done well by sheltering among the stock market’s capital preservation funds, which are positioned to help investors avoid large losses.

Since the market close on 23 February, Personal Assets Trust (PNL) has risen 1.9%, helped by its gold exposure and investment in low-risk US and UK government bonds, while RIT Capital Partners (RCP) is up 1.6% and Capital Gearing Trust (CGT) is trading 1.9% higher. Shares in Ruffer (RICA) trade 1.9% lower.

WHAT ABOUT NON-CORRELATED ASSETS?

Certain investment companies that are non-correlated to equity markets have fared well in share price terms since the invasion, among them property-focused investment trusts such as healthcare facilities landlords Assura (AGR) and Primary Health Properties (PHP), whose shares are up 1% and 1.7% respectively.

Also trading higher are supermarkets property investor Supermarket Income REIT (SUPR) and warehouse investor Tritax Big Box REIT (BBOX), both up around 3% to 4%.

HAS GOLD (AND BITCOIN) BEEN A SAFE HAVEN?

The performance of gold miners has been solid rather than spectacular since Russian tanks began rolling into Ukraine. The main exception is Russian producer Polymetal (POLY) whose share price has fallen by 76% in less than a week. It is hard to see this company retaining a listing on the London Stock Exchange for long.

The precious metal itself, a traditional ‘safe-haven’ at times of war and strife, had been steadily moving higher ahead of the invasion and is trading above $1,900 per ounce for the first time since summer 2021.

Tempering gains could be speculation Russia might sell its stockpiles of gold to help fund its war efforts.

Bitcoin, touted in some quarters as an alternative defensive asset to gold, was slow to react but moved higher on 28 February amid expectations Russia will turn to the cryptocurrency as it is shut out of the Swift international payments system and sanctions are imposed on its banking system. Bitcoin has now risen by 17% in value since the invasion began to $43,528.

WHICH UK STOCKS ARE RELEVANT TO UKRAINE/RUSSIA-DRIVEN COMMODITY PRICE CHANGES?

Ukraine is known as the breadbasket of Europe and the world’s largest exporter of sunflower oil and the second biggest producer of barley. Russia and Ukraine produce more than a quarter of the world’s wheat exports.

Pressure on soft commodity prices from the disruption of supply could increase all vegetable oil prices. This could benefit palm oil producer MP Evans (MPE:AIM) from an earnings perspective.

Low inventories and disruption to supply for industrial metals could drive a spike in related commodity prices. Russia accounts for around 11% of global platinum output and supplies 6% of aluminum and 4% of refined copper.

The biggest supply challenge is likely to be in palladium with Russia controlling around 25% of the market.

Glencore (GLEN), Tharisa (THS), Jubilee Metals (JLP:AIM) and Sylvania Platinum (SLP:AIM) are among the stocks on the London market involved in platinum and/or palladium production outside of Russia.

The spike in oil prices to seven-year highs and surging gas prices are likely to provide an earnings benefit to those companies with limited hedging, with a high proportion of their production not on fixed prices. These include Capricorn Energy (CNE), Gulf Keystone (GKP) and Jadestone Energy (JSE:AIM). Companies with exposure to UK gas prices include Serica Energy (SQZ) and Harbour Energy (NBR).

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.