Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGlencore is a stock to own amid strong commodities demand

Despite a 40% advance for the shares in the past 12 months, resources firm Glencore (GLEN) continues to look cheap.

Based on current commodity prices and forecasts from investment bank Jefferies the stock trades on a 2022 free cash flow yield of 19% with a significant chunk of cash set to be returned to shareholders.

With its commodities focus leaving it well placed to withstand inflationary pressures we think Glencore is worth buying at these levels, though we acknowledge there are risks associated with the company’s previous governance failings.

In this article we’ll look in some detail at the business, its current strategy, and the outlook on some of the key issues it is facing around coal ownership and corruption probes.

UNDERSTANDING GLENCORE

Glencore is something of an outlier in the mining sector. Starting out as a pure commodities trading operation its merger with Xstrata in 2013 greatly increased its position as an owner of mining assets.

This more complex structure, plus brushes with bribery scandals and a somewhat chequered wider history, have often seen its shares trade at a discount to the wider sector.

Founded in 1974 by commodities traders Pincus Green and Marc Rich, Glencore, an abbreviation of ‘Global Energy Commodity Resources’, listed on the London Stock Exchange in 2011 and now makes its money in two ways.

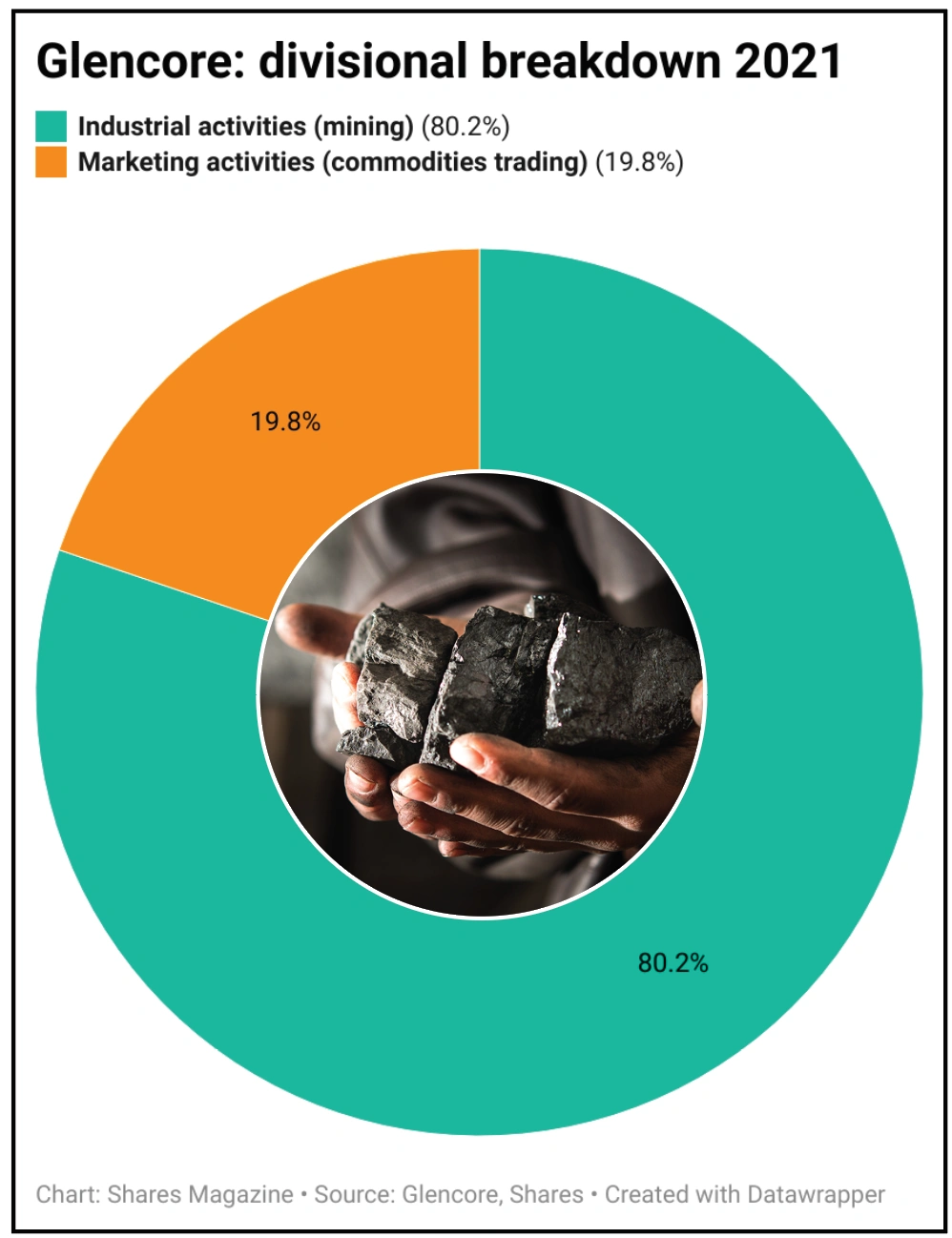

The trading operation accounted for around 20% of 2021 earnings. It physically sources commodities and products from a diversified base of global suppliers and transports these commodities by sea, rail and truck, storing, processing and delivering them according to the specifications of its customers. Products include metals, oil, natural gas and coal.

Glencore’s marketing arm makes its money through what are known as ‘arbitrage opportunities’ buying a commodity at a certain price and selling it at a higher price, making a profit after covering its costs.

Christopher LaFemina, mining analyst at Jefferies, observes that in 2021, ‘Commodity market fundamentals were strong, with significant dislocations creating arbitrage opportunities for this business.’

The company also has an interest in an agricultural commodities trading business.

Hidden value for Glencore in Viterra

Glencore holds a 49% stake in crop trading outfit Viterra – a firm which snapped up US rival Gavilon in a $1.13 billion deal in early 2022.

Officially spun out of Glencore as a standalone entity in 2020, with a group of Canadian investors having taken a stake in 2016, a full sale of Glencore’s remaining holding in Viterra has been rumoured.

According to a report, UBS has arrived at a $7 billion to $10 billion transaction value for Viterra, encompassing net debt of $2 billion. However, this assessment was based on historic deals in the space and does not reflect a likely surge in food prices linked to the war in ‘bread-basket of Europe’ Ukraine.

Artemis fund manager Jacob de Tusch-Lec holds Glencore in one of his portfolios. He says: ‘The trading operation is essentially like a hedge fund in the sense that profits are volatile and not predictable. It’s almost like a Goldman Sachs where there’s one multiple applied to the investment bank and another to the trading arm.’

Essentially Glencore’s argument is that combining marketing and mining activities gives it an inside track on commodity markets, underpinning strong strategic decisions.

STRONG PERFORMANCE FROM MINING ASSETS

A robust 2021 performance from the mining or ‘industrial activities’ division saw it account for around 80% of earnings. This part of the business saw a 118% rise in adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) to $17.1 billion, underpinned by ‘significantly higher commodity prices with many reaching record or multi-year highs, amid widespread supply/demand deficits,’ the company said.

These substantial earnings were matched by cash generation which helped reduce net debt below the targeted range of $10 billion to $16 billion.

As Jefferies LaFemina observes: ‘The Glencore deleveraging story is over. It is now a capital returns story, and we expect rising prices for some of its key commodities and continued outperformance of its marketing segment to lead to growing free cash flow and capital returns.’

CHANGE AT THE TOP

The company was led between 2002 and 2021 by Ivan Glasenberg. His successor and compatriot Gary Nagle, the former head of Glencore’s coal operations, may not be as outspoken but he is quietly making some significant changes, in particular on environmental, social and governance issues.

On the ‘E’ side of the ESG equation, Nagle has committed to more aggressive total emissions reductions with a new short-term target of a 15% reduction by 2026, and a 10 percentage point increase in its medium-term target to a 50% reduction by 2035, with a net zero ambition by 2050.

The mining operation also focuses heavily on metals like copper, zinc and nickel. All of these will be key to the transition away from polluting fossil fuels thanks to their role in building the electric vehicle and renewable energy infrastructure required for this shift.

THE COAL ISSUE

A key sticking point, and a contributor to Glencore’s discounted equity rating, is its interests in thermal coal. Activist investor Bluebell Capital, which has a stake of undisclosed size in the business, has pushed for these assets to be spun off, in a similar way to how Anglo American (AAL) demerged its own coal assets to create Thungela Resources (TGA) in June 2021.

However, when acquiring BHP’s (BHP) stake in the Cerrejon coal mine in Colombia in 2021 for $294 million, Glencore’s then-CEO Glasenberg observed that ‘disposing of fossil fuel assets and making them someone else’s issue is not the solution and it won’t reduce absolute emissions.’

Glencore’s argument is that it will be a responsible steward for the assets and wind them down gradually over time.

Bluebell’s demerger proposal would allow for this with a dual share class structure for a ‘Coal NewCo’, which would allow Glencore to maintain control over the assets.

Artemis’ de Tusch-Lec notes: ‘Right now the whole company is punished because some investors cannot invest in coal. There may be a clever solution, but it needs to be more than just disposing to a worse operator.’

RESOLVING CORRUPTION SCANDALS

In terms of governance issues Nagle has allocated $1.5 billion to resolve corruption probes in the US, UK and Brazil with the aim of putting these to bed in 2022.

The key questions for investors to weigh are whether this sum be sufficient to cover all potential liabilities and are there any, as yet unaired, skeletons in Glencore’s closet? It is also worth noting that the current provision does not encompass investigations in Switzerland and the Netherlands.

For his part de Tusch-Lec adds: ‘By buying Glencore we are supporting the company in embarking on a journey to higher standards; not ticking boxes, but accelerating the move to net zero without destroying shareholder value.’

GLENCORE IS A MAJOR PLAYER IN THE WORLD METALS MARKET

COPPER:

Glencore is one of the world’s largest producers and marketers of copper. In 2020, it produced 1.26 million tonnes, and sold 3.4 million tonnes through its marketing business. The company is also one of the world’s largest producers of cobalt.

It mines and processes copper in Africa, Australia and South America. Scrap copper is recycled by Glencore in North America and Asia. It also smelts and refines copper in various parts of the world.

OTHER METALS:

Glencore produces nickel in Canada and Norway, and zinc and lead in Australia, South America, Kazakhstan and Canada. It processes and sell products including bauxite from a range of third-party aluminium and alumina producers. The company also markets iron ore from third party producers, primarily selling to Asia.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.