Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine6 great stocks for your ISA

The deadline for using up this tax year’s £20,000 ISA allowance is fast approaching. You have until 5 April to use it or lose it, so now is the time to think about topping up your account.

Clearly there are reasons to be nervous as an investor amid rising inflation and tensions in Ukraine, but you do have the option of putting cash into an investment ISA now and sitting on it until you’re ready to put it to work in the markets.

In doing so, you would lock in those ISA benefits which mean you don’t pay tax on any future capital gains or income inside the account.

For those happy to invest now, Shares has six investment ideas which are compelling regardless of the wider backdrop. Using screening tools, we have selected six stocks which fit several different themes including income, growth, quality, and value matched by earnings momentum. Read on to discover the names and why we like them.

You can invest up to £20,000 across Stocks and Shares, Cash and Innovative Finance ISAs in a tax year.

Lifetime ISAs have a limit of £4,000 a year, and this allowance counts towards the overall £20,000 annual ISA limit if you’re also using Stocks and Shares, Cash and/or Innovative Finance ISAs. You can put money into one of each kind of ISA each tax year.

Junior ISA accounts are available for children under 18 and have a limit of £9,000 a year.

Value and earnings momentum

Kenmare Resources (KMR) 432p

Dublin-headquartered Kenmare Resources (KMR) is on the cusp of substantial cash flow generation from its 100%-owned Moma mineral sands operation in Mozambique and yet the shares are trading at bargain basement levels.

With catalysts in place, this represents a stunning value opportunity for investors and one they should seize with both hands.

The company extracts three key minerals – ilmenite, zircon and rutile – from sand in a substantial section of the Mozambique coast. It uses dredging equipment to collect the sand and then separates out the minerals in processing plants.

Kenmare, which made its first shipments from Moma in 2007, previously encountered some problems with sub-standard work by contractors but operations are now running more smoothly. Despite significant progress on site, the share price is still a long way below the peaks enjoyed in the late noughties and early 2010s.

Kenmare is currently valuated at a mere 3.4 times 2022 consensus forecast earnings per share which looks far too cheap.

Having just completed a significant programme of capital expenditure, Berenberg forecasts Kenmare will generate free cash flow of $182 million for 2022. This translates into an eye-catching free cash flow yield of more than 30%. The company could end the year in a net cash position and this rich cash flow should underpin generous returns to shareholders.

The equity valuation seems at odds with Kenmare’s growing production profile as well as resilient global demand for ilmenite, zircon and rutile and relatively limited supply.

Ilmenite is the main source of titanium oxide, used in paints, printing inks, fabrics, plastics and sunscreen. Zircon is employed in areas like foundry casting, nuclear fuel rods, catalytic convertors and air and water purification systems, while rutile has applications in the production of titanium metal.

The main risks for the company and its share price include any big decline in global economic demand which could hurt commodity prices, and the company’s single-asset focus so it cannot afford to suffer any major operational setback. [TS]

Somero Enterprises (SOM:AIM) 484p

You might be surprised to find a genuine world technology leader listed on the AIM market but this is how you could describe Somero Enterprises (SOM:AIM) which is trading on an attractive valuation. The 2022 price to earnings multiple stands at 10.3.

Somero is the world number one when it comes to concrete levelling kit. Its success was to develop laser-guided technology over the last couple of decades that is accurate to within fractions of millimetres. This is becoming increasingly important for major construction projects like building skyscrapers, but Somero has a digital economy slant too.

As we increasingly shop online, nations everywhere need large numbers of modern warehousing and fulfilment centres. With these vast sheds increasingly embracing robotics and automation, much like the car industry did years ago, these properties need level flooring to the nth degree.

Somero has a range of products, and its training, fast turnaround servicing and general advice to buyers about getting best performance both operationally and from capital expenditure make the company stand out. This is what protects its high margins in an industry where cheaper, reverse engineered copycat machines exist but can’t do the job to the same standard.

Over the past five years Somero’s shares have averaged annual returns of nearly 18%, versus about 4% for the FTSE 100. A trading update on 26 January flagged better profit and cash than management expected, leading analysts to increase forecasts, a second upgrade in two months. [SF]

Great income

Rio Tinto (RIO) £55.86

Miner Rio Tinto (RIO) is getting its act together after being beset by corporate governance concerns. Strong drivers for the metals which the miner extracts and processes should sustain attractive cash flow and generous dividends for shareholders in the medium term.

The company, which derives a significant chunk of its earnings from iron ore, copper and aluminium production, recently announced 2021 dividends worth $16.8 billion, the second highest in UK corporate history.

While dividends aren’t expected to match this monumental sum going forward, the shares still offer a 2022 prospective yield of 9.2% based on consensus forecasts.

While such a high yield would typically ring alarm bells that the dividend is unsustainable, in Rio’s case it is underpinned by prodigious cash generation and a strong balance sheet with the company sitting on net cash upwards of $1.5 billion as at 31 December 2021.

Under the leadership of Jakob Stausholm, the company is trying to improve its previously patchy track record on governance issues. In February a survey covering its workplace culture revealed shocking revelations of racism, sexism, bullying and harassment.

However, by owning up to its problems Rio Tinto has taken an important first step in addressing them and the report also acknowledged improvements had been made in the previous 12 months, roughly coinciding with the start of Stausholm’s tenure.

Stausholm has also outlined an ambitious strategy on climate change, in the company’s own words ‘combining investments in commodities that enable the energy transition with actions to decarbonise our operations and value chains’. As with several firms in the resources sector there has been more talk than action so far.

While revenue and profit are expected to moderate from an exceptional 2021, recent under-investment in the mining industry, plus demand from significant planned investment in electric vehicle and renewables infrastructure, has created positive conditions for metals prices and this should make Rio an excellent income pick for years to come. [TS]

Going for growth

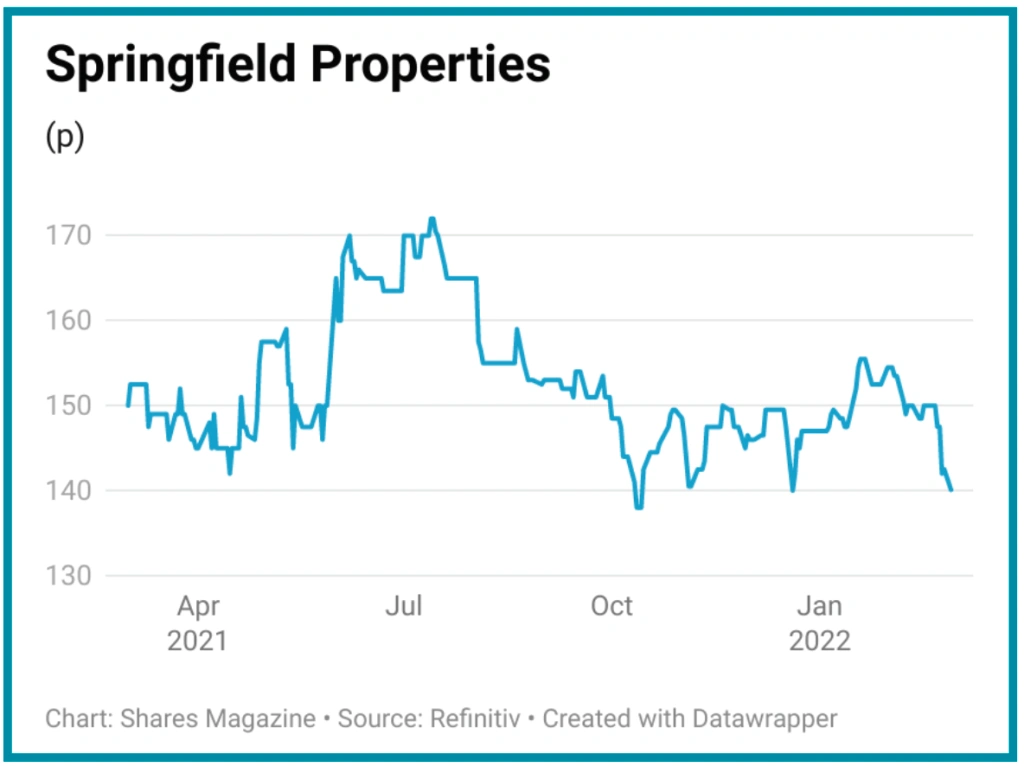

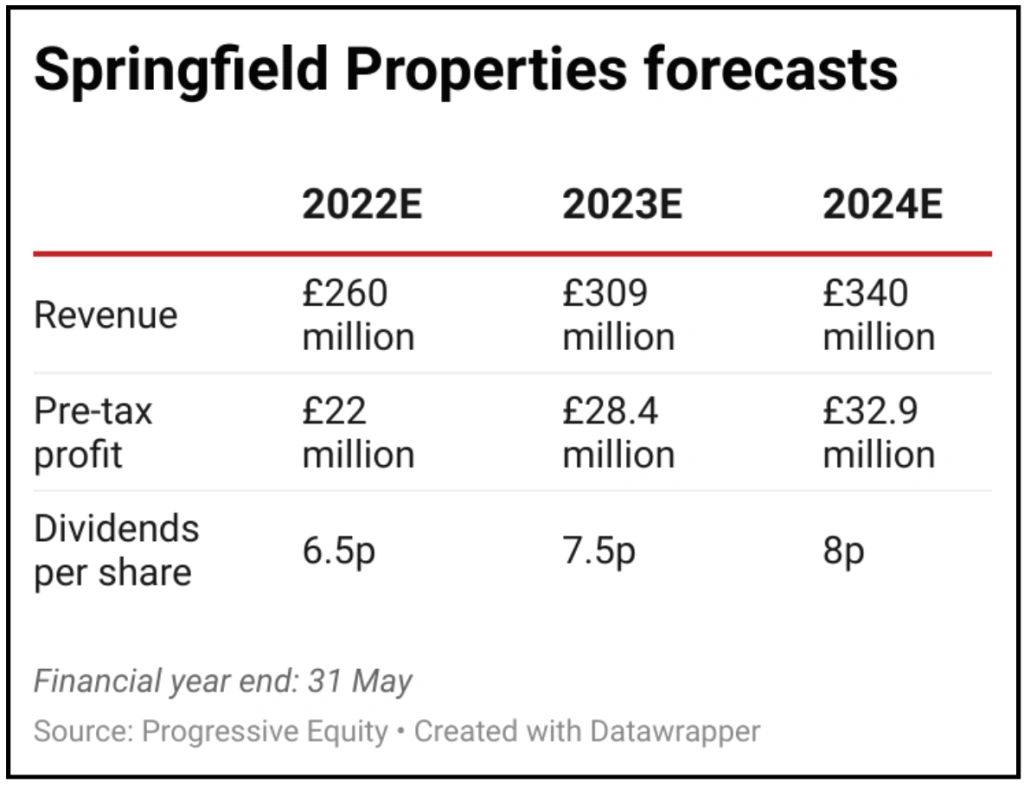

Springfield Properties (SPR:AIM) 138.55p

Scottish housebuilder Springfield Properties (SPR:AIM) has an impressive growth record and is on track for plenty more of the same over the next few years. This doesn’t look fully reflected in a rating of 7.2 times consensus earnings for the year to 31 May 2023.

The firm, which specialises in affordable housing, is enjoying excellent demand with record sales in the six months to November 2021.

It also has significant visibility over future sales thanks to the ‘missive’ system which operates in Scotland.

Missives are the written exchange of terms and conditions between a buyer and seller of a property. Once the missives have been ‘concluded’, neither side can back out of the deal.

This means Springfield can reliably forecast its sales pipeline with greater certainty than housebuilders in England. The firm’s current order book is the highest in its history.

Springfield is working with the Scottish government on the development of new ‘villages’ in semi-rural areas including the commuter belt of key cities.

The recent acquisition of Tulloch Homes increases Springfield’s already considerable land bank and gives it a presence in the Highlands.

Tulloch is already profitable and highly cash generative with no debt, so the acquisition is earnings-positive for Springfield.

The firm has also expanded into the private rental sector which will provide additional revenues on top of affordable and private housing.

Houses are built to a fixed-cost design for its partner Sigma Capital, which owns, lets and manages the properties.

Management recently confirmed earnings would meet full year expectations thanks to its substantial order book and high level of missive sales pending. [IC]

Top quality stocks

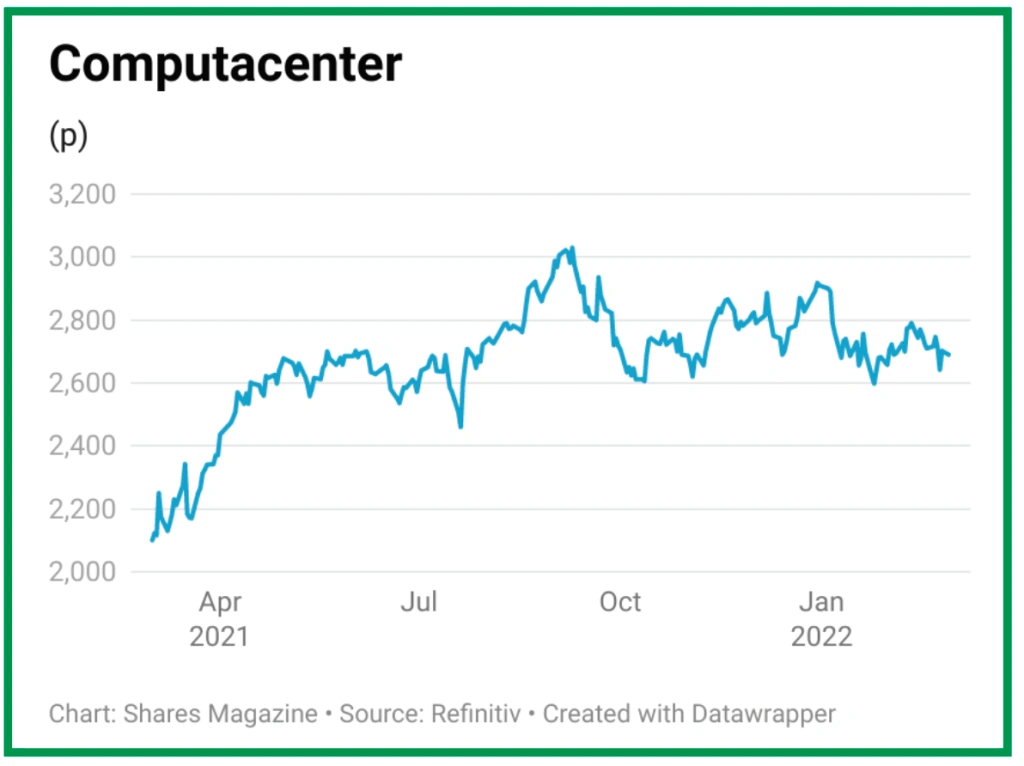

Computacenter (CCC) £26.86

What price to earnings multiple would you pay for a stock that has returned nearly 20% a year over the past decade in share price gains and dividends, and continues to see forecasts upgraded? 25? 30? Computacenter (CCC) is currently trading at less than 17 times 2022 earnings.

In an era of unprecedented technological change there are thousands of organisations needing help with adaption and adoption, and Computacenter is there to help. It is a pan-European IT enterprise operator whose 16,000-odd staff annually ship more than 25 million products to 4.5 million end users, providing valuable advice, support and services in 30 different languages.

The company has been part of the FTSE 250 index for most of the last 10 years and has been an astonishingly reliable investment for shareholders on both capital growth and income fronts. Analysts calculate that in the decade or so before the pandemic, Computacenter handed back something like £350 million to shareholders in regular and special dividends.

Group operating margins are low in the region of 4%, reflecting the fact it sells a lot of third-party computer software and hardware and takes a small cut. But one of the fastest growing parts of the business is providing managed services – namely remote IT support – where margins are estimated to be closer to 20%. Given the strong growth in this arm, overall group margins should improve as the years go on. [SF]

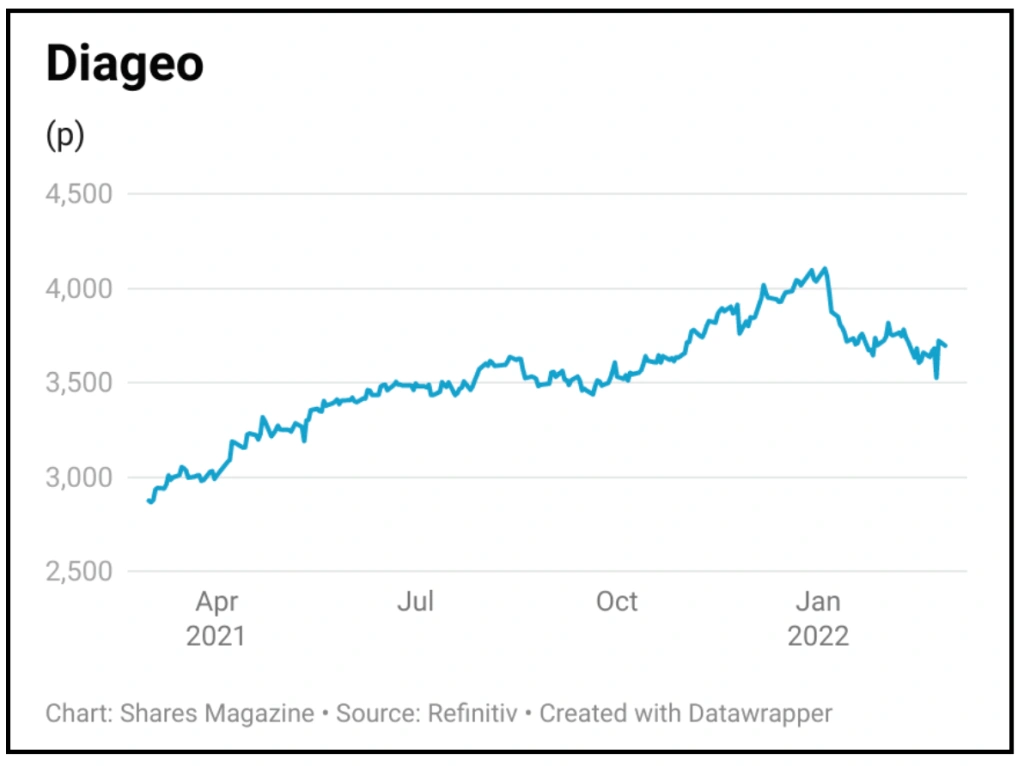

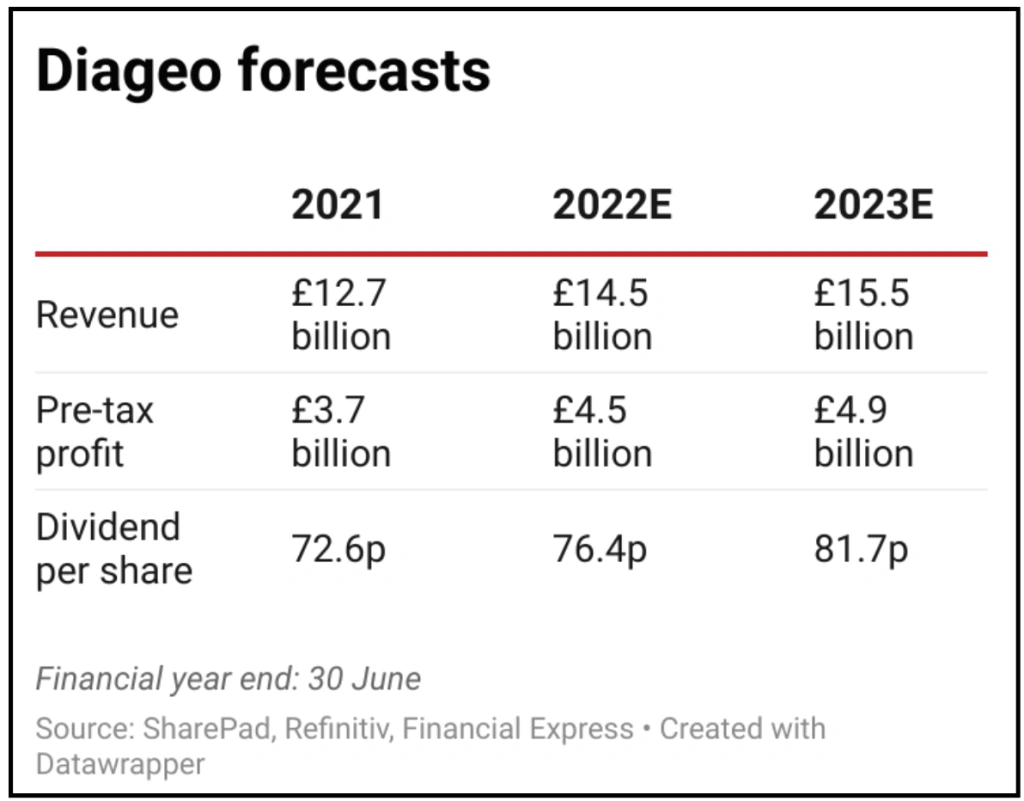

Diageo (DGE) £36.96

Drinks-maker Diageo (DGE) is a high-quality business which owns an outstanding collection of some of the world’s most prestigious spirits and beer brands, including Johnnie Walker whisky, Don Julio tequila, Smirnoff Vodka and Baileys liqueur.

Investors looking for quality in a business expect certain financial characteristics including consistent profitability and pricing power and Diageo satisfies these expectations.

Despite many years of consistent growth Diageo still only commands around 4% share of the global alcohol market. By 2030 management want that share to rise by 50% to around 6% share.

One of the key competitive strengths of the company is its global reach and dense distribution network which has cost advantages that allow the company to spend more on advertising and promotion, creating a virtuous circle.

These strengths also mean Diageo is an attractive home for upcoming new brands looking for global reach and maximum promotion.

Over the last seven years the company has delivered an average return on equity of close to 30% a year while free cash flow has grown by nearly 10% a year. Free cash flow is what is left after paying all operating costs and servicing financial liabilities.

Return on equity represents the investment return attributable to shareholders and is simply net profit divided by shareholder’s equity. A typical return for a UK company is around 12%.

High return on equity provides both defensive and growth advantages not available to ordinary businesses. In less rosy times, even if profitability falls, there is a bigger financial cushion.

In good times, there are more options to increase value for shareholders through investment in the business, dividends, share buybacks or acquisitions. Diageo has used all these advantages to consistently grow the business. [MGam]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.