Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSurviving the market sell-off

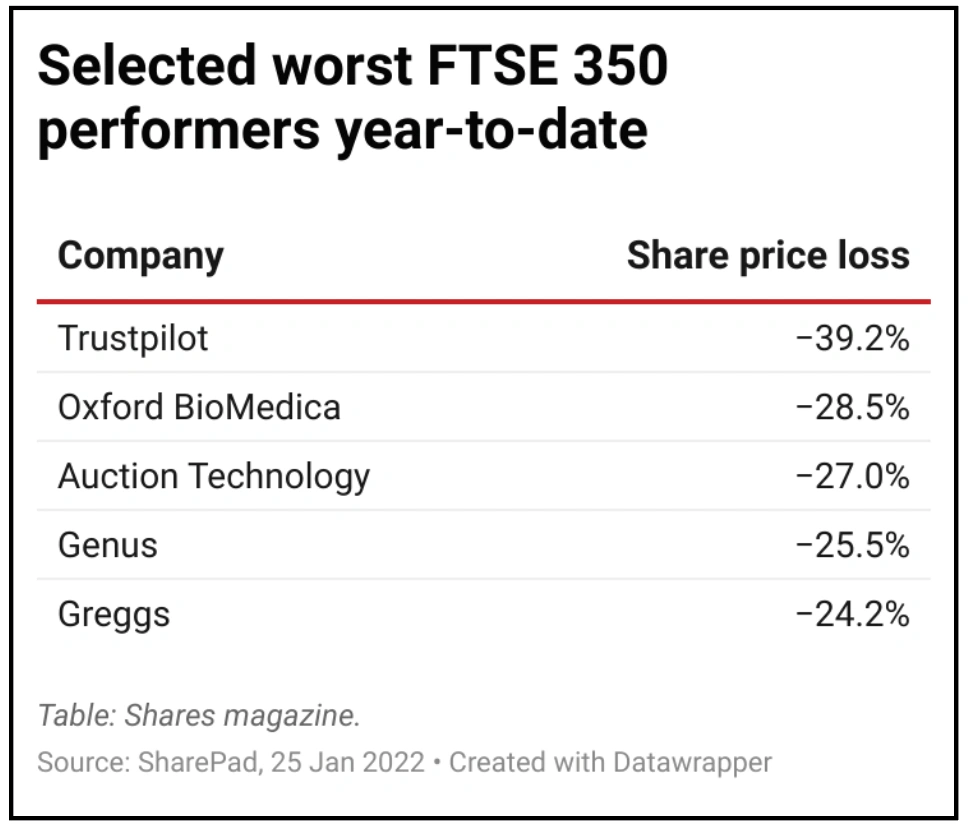

It has been a tricky start to the year for investors. Some popular stocks and funds have fallen by more than 20% in less than a month, leaving portfolios battered and bruised.

At the time of writing (25 Jan), the technology-rich Nasdaq index in the US was down 12.5% so far in 2022. This compares with the MSCI World index which is down 6.9% and the FTSE 100 which has fallen 1.9%.

It is too early to say if the sell-off is over. Markets in the US initially slumped on 24 January but ended the day in positive territory. European markets pushed ahead the day after, but stocks in China, Hong Kong and Japan went in the opposite direction. Investors need to stay alert that further pain could be around the corner.

In this article we explain why markets are behaving this way, why there is no cause for panic, as well as reflecting on how, if at all, you should respond.

A SHIFT IN THE MARKET

There are several factors behind the market jitters including geopolitical considerations as tensions build between Russia and Ukraine, as well as oil price volatility and the ongoing threat posed by Covid-19.

However, the central concern has been inflation and interest rates. A long-delayed tightening of monetary policy, accelerated by mounting inflationary pressures, is affecting how different stocks are valued and driving a shift in the market away from so-called growth stocks and into value.

This can be seen in microcosm in the performance of two US car stocks year-to-date. Electric vehicle company Rivian Automotive created a buzz at its November 2021 stock market debut and it briefly captured a $100 billion valuation.

However, Rivian has to date only manufactured a very small number of vehicles so buying the shares at such an elevated valuation meant making big assumptions about its future growth and ability to generate cash flow.

Ford, which owns an 11.3% stake in Rivian, can already point to a healthy stream of profit and cash generation and has its own electric vehicle ambitions. Year-to-date shares in Rivian are down 37.8% versus a 6.3% decline from Ford and this example helps capture the dynamics at work in the market.

The market has really gone off businesses that don’t make money and which trade on sky-high valuations. Rivan is the loss-making growth play and Ford is the profitable value play.

THE INFLATION PAIN

Interest rates are being hiked because of inflation, which itself is usually accompanied by economic growth. In this environment investors don’t have to pay a high price for the long-term potential offered by sectors like technology when they can get much cheaper growth today from industries like oil, mining and banking.

It is the dominance of these sectors in the FTSE 100 which helps explain why the UK’s leading stock index hasn’t fallen by as much as many other major indices globally this year.

To put it even more simply you don’t have to pay up for ‘jam tomorrow’ when you can get ‘jam today’.

The appeal of lower risk assets like cash and bonds are also boosted when rates are rising, meaning more speculative stocks can be out

of favour as lower risk assets stand to deliver higher returns.

DISCOUNT RATES

There is a further technical reason why rising interest rates are bad for growth stocks. They impact the discount rate which is used to calculate what a cash flow in the future should be worth today.

The scenario now playing out is a direct reversal of the situation for the last decade or more, where rates have largely been either falling or flat.

The discount rate is based on the so-called risk-free rate, which is the yield available on government bonds (which typically goes up when interest rates are being hiked) and the extra return you expect from a riskier asset known as the risk premium.

Because this discount rate has an incremental impact over time, firms with a decent and reliable level of cash flow today are less affected by it than companies promising rapid growth and lots of cash flow in the future.

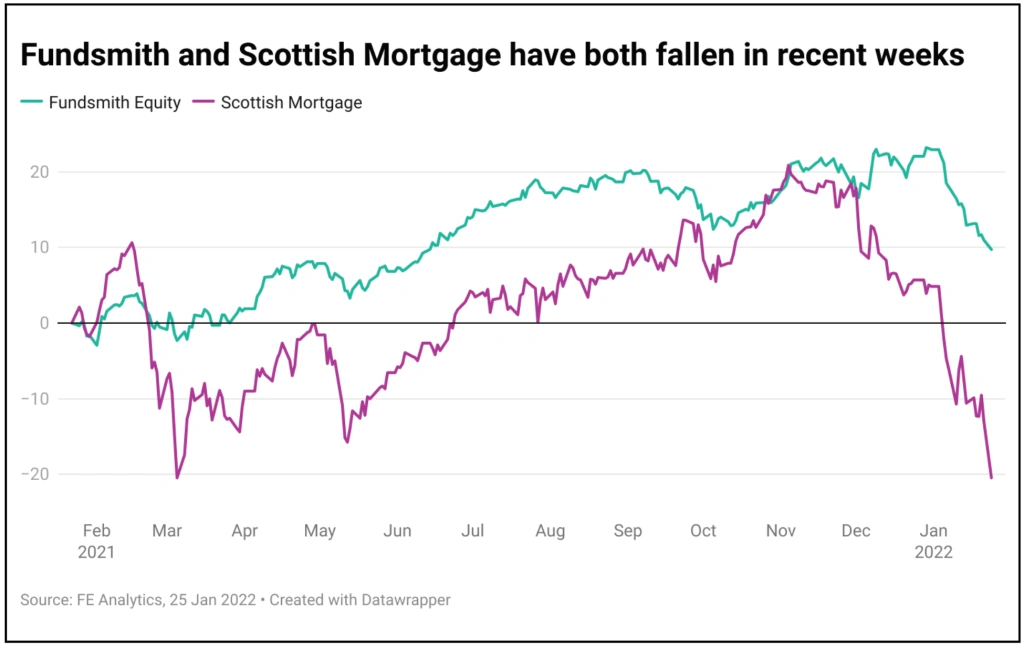

TOP FUNDS STRUGGLE

The diminished valuations of growth stocks can be used to explain why some popular and successful funds have struggled of late.

Previously vehicles like Fundsmith Equity Fund (B41YBW7) and Scottish Mortgage (SMT) benefited not just from the earnings growth delivered by the companies in their portfolio

but also these shares being ascribed an increasingly higher multiple of earnings – in essence investors have been prepared to pay more to own these companies.

There is a risk that rising interest rates put the brakes on global growth and create conditions where corporate earnings fall and investors want to pay less for stocks, known as multiple contraction, which create two negative forces for a share price.

WHO HAS BEEN SWIMMING NAKED?

Fundsmith manager Terry Smith observed in his letter to investors at the beginning of January 2022: ‘We find it difficult to outperform in particularly bullish periods where the market has a strong rise, as a rising tide floats all ships, including some which might otherwise have remained stranded and that we would not wish to own.’

If, as Smith says, a ‘rising tide floats all ships’ then, to borrow another well-worn saying, when the tide goes out you discover who’s been swimming naked. Or, put another way, which shares have been rising on little more than hype rather than anything of any substance.

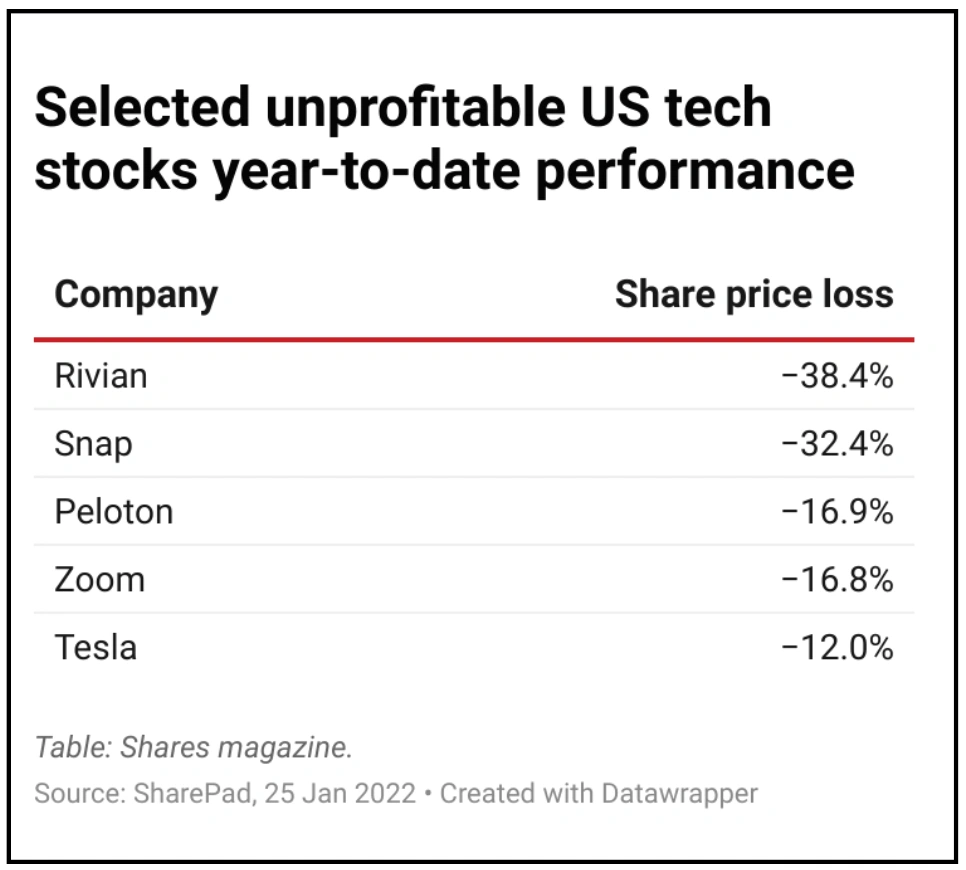

Initially when there is a shift in the market, selling is often indiscriminate but that won’t last forever. Not all growth stocks are created equal. There’s a big difference between a company like Google-owner Alphabet which posted free cash flow of more than $18 billion in its latest quarterly update and a business such as Snapchat parent firm Snap which is still hunting for its first profit since its IPO in 2017.

Seema Shah, chief strategist at Principal Global Investors, notes: ‘Investors have been rewarded by the “overweight tech” trade for the better part of the past decade. And while conditions for the sector are becoming trickier, strong companies with robust balance sheets and pricing power still have further to run. For the profitless ones, technically speaking, the period ahead may not be so pretty.’

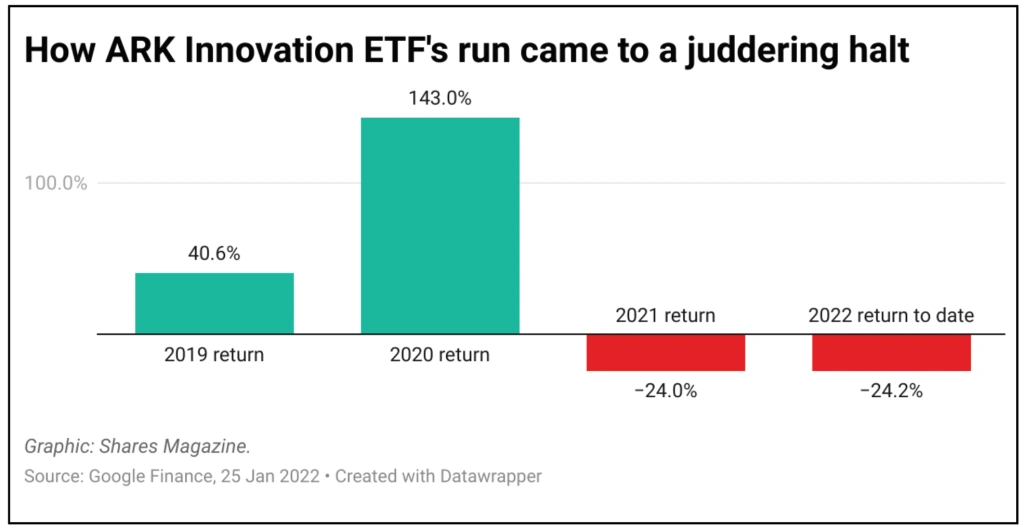

This is reflected in the performance of a basket of unprofitable technology stocks created by investment bank Goldman Sachs whose performance has collapsed since the back end of 2021 after an extraordinary run. Cathie Wood’s ARK Innovation ETF which tracks a collection of disruptive and innovative businesses, is also under severe pressure, down nearly 25% since the start of January.

A correction in these areas of the market was probably overdue and is quite a healthy development, though that offers little compensation if you are directly exposed to it.

BENEFITS OF A DIVERSE PORTFOLIO

The sell-off in stocks and shares, also known as equities, has acted as a reminder for investors to ensure they have a diverse portfolio. That means having a mixture of assets that hopefully don’t all move in tandem.

While equity markets have been weak this year, having exposure to bonds, gold and property would have been beneficial. For example, year-to-date, Allianz Strategic Bond Fund (B06T936) which invests in basket of bonds is only down 0.5%, iShares Physical Gold ETF (SGLN) which tracks the gold price is up 1.3% and BMO Commercial Property Trust (BCPT) which has positions in various offices, shops and warehouses is up 10.8%.

WHAT YOU SHOULD DO NEXT

As an investor the best advice is not to over-react to short-term fluctuations in stocks and shares. However, it could be a good time to consider selling anything too speculative in your portfolio as sentiment towards this type of investment is unlikely to improve in the near term.

Any cash you can generate from these sales could then be used to take advantage of buying opportunities in quality shares caught up in the sell-off. We plan to look at some of these opportunities in an upcoming issue of Shares. Think hard about diversification in your portfolio and consider adding some bonds, gold and property if you don’t already have any.

Otherwise, and assuming you can remain invested to give your portfolio time to recover, you should avoid selling any positions that

have been weak in recent weeks. Markets have historically bounced back fast from sell offs, although there is no guarantee that will happen now.

Continue to drip feed money into the markets if that’s what you are already doing. Given it is difficult to time the market effectively you are better off having ‘time in the market’ instead.

DISCLAIMER: Daniel Coatsworth who edited this article has a personal investment in Fundsmith Equity Fund

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.