Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineScottish Mortgage share price down 33%: buy more or sell out?

It’s no exaggeration to say Scottish Mortgage (SMT), managed by the team at Baillie Gifford, is the UK’s favourite investment trust. With assets under management of nearly £21 billion as of the end of December it dwarfs the next-biggest trusts, and its long-term performance record is unbeatable.

Over five years to December 2021, net asset value per share with debt at fair value increased by 333% against an 82% total return for the FTSE All-World index in sterling. Over 10 years, the increase was 1,007% against 271% for the index.

So, why have the shares performed so badly since the interim results on 17 November and what course of action should investors take after a 33% fall in the value of their investment since the peak last year?

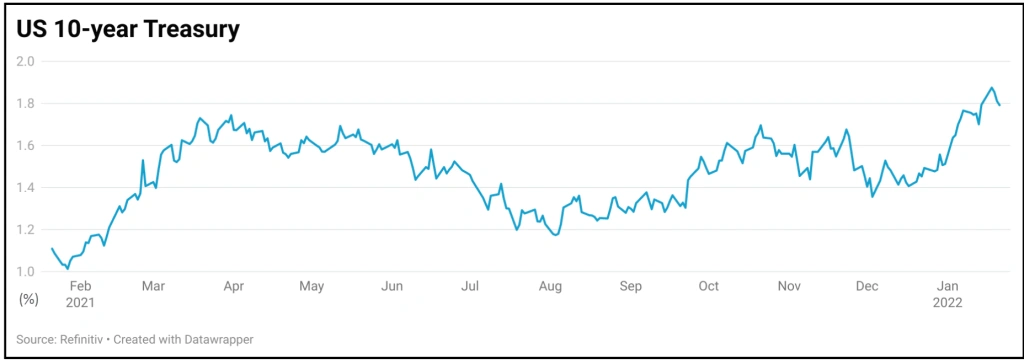

THE RISK-FREE RATE

It is important to look at the US 10-year Treasury (government) bond for global markets and in particular the yield it offers investors.

For most investment firms, the US 10-year government bond is considered the only true ‘risk-free’ asset which all other investments are measured against.

Given stocks are by their nature riskier than US government bonds, they have to offer a higher return than the ‘risk-free’ rate on Treasuries. This doesn’t just apply to Scottish Mortgage; it applies to all stocks.

The higher the perceived risk associated with an asset class, the higher the return investors will demand. For example, emerging market equities are seen as riskier than developed market equities so they should offer a higher return, which typically means a lower price to earnings multiple.

Technology stocks, especially those which must invest heavily in their business to generate growth, meaning profits are still years away, should in theory offer a higher return than boring plain-vanilla stocks as they are riskier.

The problem is that during the pandemic investors have chased growth stocks up, and especially profitless technology stocks, so their returns no longer look attractive compared with Treasury bonds.

If we then factor in a rise in the ‘risk-free’ rate from below 1.4% to nearly 1.9% in a matter of weeks over Christmas and the New Year as investors anticipate rising rates at the central bank, the Federal Reserve, then riskier assets begin to look even less attractive.

Given its reputation as a big investor in technology stocks where profits, in many cases, are still some way off, it’s hardly surprising that Scottish Mortgage has seen its share price fall although the scale of the sell-off is surprising.

TECHNOLOGY EXPOSURE

While technology stocks were ‘collateral damage’ during the recent spike in Treasury bond yields, it’s important to bear in mind that ‘not all tech is created equal,’ says Seema Shah, chief strategist at Principal Global Investors.

Profitless firms such as those represented by the Goldman Sachs Non-Profitable Technology Index are particularly vulnerable to rising rates as they derive almost all their present value from future cash flows.

In contrast, ‘mega-cap technology firms which generate huge cash flows, have strong balance sheets, exhibit strong pricing power and offer impressive earnings delivery, are far more resilient,’ argues Shah.

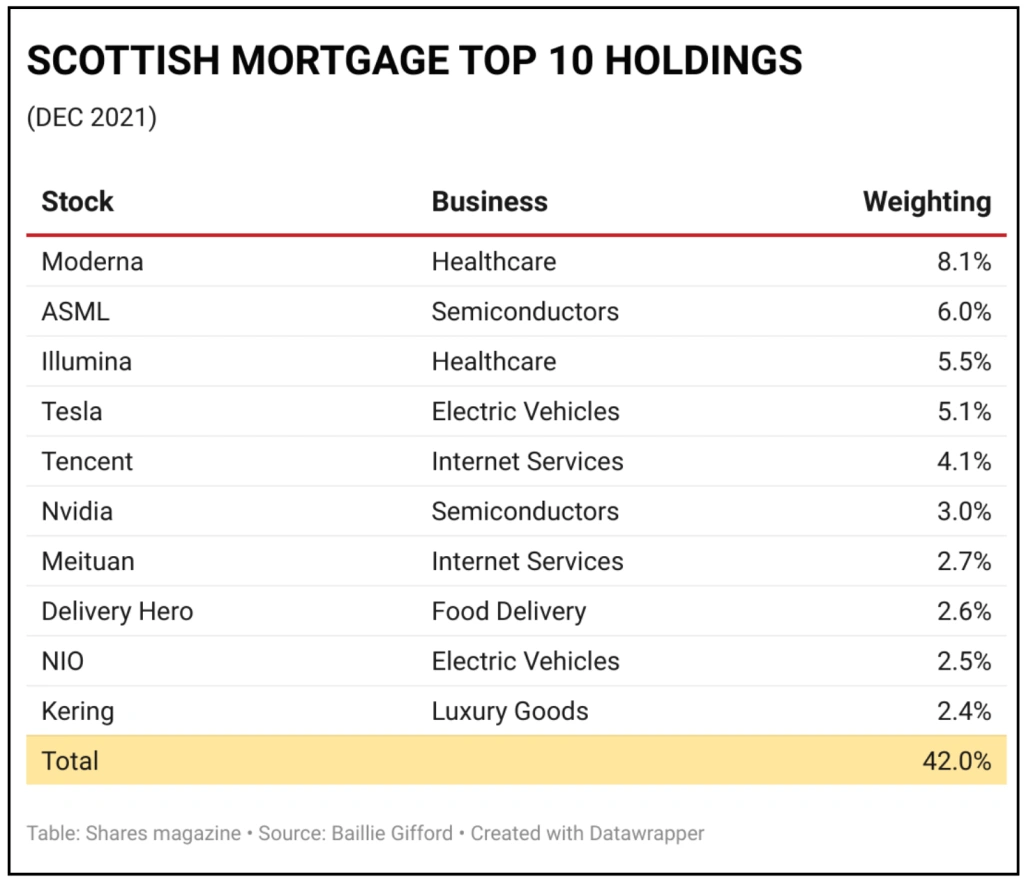

If we look at the top 10 holdings in the Scottish Mortgage portfolio, which at the end of December accounted for 42% of the total assets, six of the 10 stocks can be classified as technology.

The largest, Dutch firm ASML, is the world’s leading manufacturer of machines used to make semiconductors with a strong record of profitable growth. Whereas making chip equipment may have been a cyclical business in the past, the industry is going through the biggest structural growth phase in its history.

Lead times for chips are up to 25 weeks compared with 10 to 15 weeks on average over the last five years, and according to ASML’s chief executive Peter Wennink the firm is running at 100% capacity, yet demand is still 50% above what it can deliver.

Scottish Mortgage also has a big position in US chip maker Nvidia which makes the gold standard processors that have become essential for cloud service providers Amazon, Alphabet and Microsoft in running apps and processes.

According to Stephen Yiu, manager of the Blue Whale Growth Fund (BD6PG78) which also includes the stock in its top 10 holdings, Nvidia ‘lies at the confluence of three major secular trends over the next decade – artificial intelligence, augmented reality and 5G’, which could drive profitable growth for years to come.

Famously, Scottish Mortgage was also an early backer of electric vehicle maker Tesla, and although it has pared its stake the investment trust still has a sizeable holding in the company’s shares.

For all the hubbub around the stock, Tesla posted record sales and earnings in the third quarter of 2021 as global demand for electric vehicles enters what the firm believes is a structural shift to higher growth.

CHINESE EXPOSURE

Another concern investors may have around Scottish Mortgage is its exposure to Chinese stocks, which for the most part have lagged developed market equities over the last year for a variety of reasons.

There are three Chinese stocks in its top 10 holdings, accounting for 9.3% of the portfolio, covering sectors such as technology, social media, electric vehicles and e-commerce.

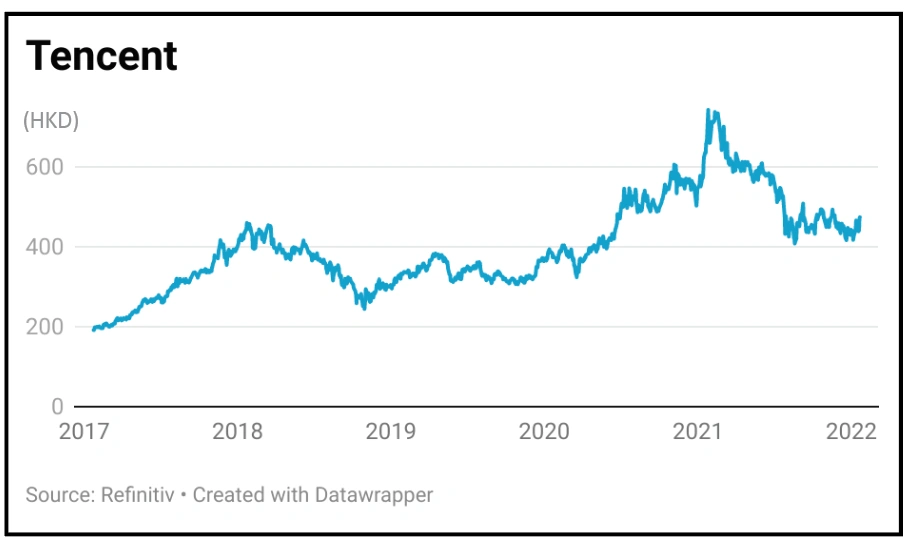

The largest holding is Tencent, the hugely successful and highly profitable internet services and gaming company, whose share price was last year hit by regulatory pressures on the business.

While its shares lost 20% in 2021, the company itself continued to rack up increases in sales and operating profits as it adapted to the new regime and invested in new growth initiatives, and this month it was ranked the most valuable company in China.

Scottish Mortgage fund managers James Anderson and Tom Slater say they are assessing the long-term implications of China’s new regulatory approach for their holdings, but they are still confident of their growth potential.

FOCUS ON HEALTHCARE

What many investors may have overlooked is Scottish Mortgage’s ability, despite its size, to shift its focus as and when it finds more attractive growth areas.

A prime example is the healthcare sector, which a year ago accounted for just 12% of the fund but is now the biggest exposure at 21% of the portfolio.

Part of the increase is down to the stellar performance of some of its holdings during the pandemic, while part is due to the managers’ appreciation of the intersection between medicine and technology.

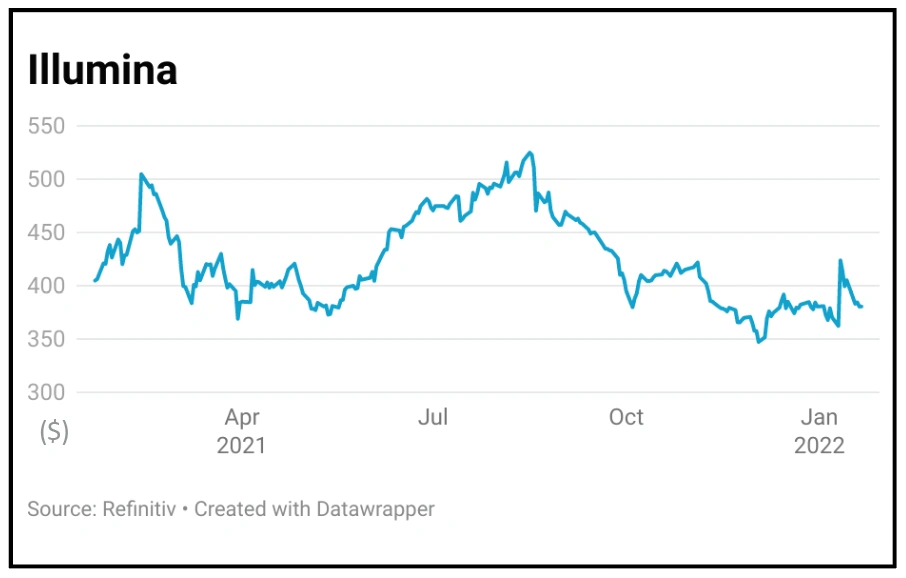

The fund’s two biggest healthcare holdings, in US firms Moderna and Illumina, accounted for 13.6% of net asset value at the end of December, but the managers are still enthused about their growth potential.

Between them, Illumina and Moderna took just four days to crack the codes to Covid. Illumina took two days to sequence the novel coronavirus, with Moderna taking an additional two days to translate that sequencing into an mRNA molecule which is the basis of its vaccine.

‘It is sometimes crudely assumed that Scottish Mortgage invests in technology companies, but that misses the point here, as it does with our other holdings,’ say the managers.

‘What we’re interested in is where technology is applied to enable new ways of doing things and, by doing so, creates new business models in industries – such as healthcare – which perhaps haven’t yet seen that transformational pace of progress.

‘It’s not just about the technology, it’s that in combination with the right people driving it: it takes revolutionary thinkers with an innovative mindset to see their vision through and make this progress happen. That’s what excites us about Moderna and Illumina.’

Both companies have already proved to be fruitful investments, and we note both recently raised their 2022 guidance, despite which their shares have lost ground in recent months.

Whether or not the managers add to their holdings, investors who take the opportunity provided by the sell-off to buy Scottish Mortgage shares are therefore getting exposure to both stocks at unusually low valuations.

EARLY-STAGE INVESTMENTS

While the fund can invest up to 30% of its assets in unlisted (also known as unquoted) companies, for the last two years or more that proportion has been around 20% and as of December it was 21.3%, although numerically unquoted businesses make up almost half of its holdings.

The advantage of owning shares in companies before they come to the market will be clear to long-term holders of Scottish Mortgage given its success down the years with companies like Alibaba, which has returned more than 800% on the initial investment, and Ginkgo Bioworks, which has returned more than 1,900%, not to mention Tesla.

However, it isn’t unreasonable for newer investors to worry about the lack of visibility in unlisted holdings and we understand the concerns over the potential for valuations to suffer if the risk-free rate rises.

According to analysts at investment bank Stifel, valuations for around a third of the unlisted holdings are updated each month, which means the whole unquoted portfolio is revalued every quarter.

Just under half of the unquoted holdings are valued either on recent deal multiples or expected multiples where deals have been announced.

Moreover, there is no question of the managers going ‘off-piste’ with their unquoted holdings in terms of stock or sector selection. Each company is subjected to the same rigorous analysis, with the result that, unsurprisingly, the vast majority are in the same areas as the quoted holdings, namely technology, internet services, software, gaming, electric vehicles and healthcare.

For those that still have concerns about the fund’s exposure to unlisted companies, a simple calculation may help put things in perspective. At the end of December, the top four quoted holdings, i.e those in companies which are already listed on a stock market, accounted for 24.7% of net asset value, more than the entire weighting of the 49 unquoted holdings.

ACTIVE SHARE

The managers are unapologetic about their investment approach, rightly so in our view. The team seeks out genuine outliers – superior, scaleable, long-term growth companies, both quoted and unquoted, with the potential to generate a return many times the size of their investment.

The managers say they ‘think in terms of owning companies rather than renting shares and are first and foremost stock pickers, selecting investments based on an individual company’s fundamental characteristics’. That inevitably means the portfolio deviates hugely from its benchmark.

This gap, known as the ‘active share’, is typically above 90% meaning the fund has less than a 10% correlation with the index. That means there are periods when it will underperform the index by a big margin, but as the managers say it is wrong to measure returns on a six-month or even a one-year basis as they are investing with a longer time horizon.

The managers believe ‘it is only over periods of five years or longer that durable competitive advantages and managerial excellence within companies are truly reflected in returns’.

WHAT SHOULD INVESTORS DO?

We’ve assumed throughout the article that readers are either current holders of Scottish Mortgage or potential buyers and are therefore wondering whether they should own the shares or not.

Our view is they should, and if they have scope – in other words as long as they own the fund for the long term as part of a diversified portfolio – they should actually add to their holdings now.

It’s rare for a fund of this calibre to suffer a 25% drawdown, especially in such a short space of time and when the managers haven’t put a foot wrong.

Like the managers, we don’t claim to have any special skill in timing markets, so rather than go all-in we would suggest setting up a regular monthly investment to feed money in and take advantage of the sell-off.

Considering the managers’ exceptional track record, it’s worth noting the fund’s fees are among the lowest in the investment trust sector with an ongoing charge of 0.34% of assets, which for us makes it even more appealing as a long-term holding.

DISCLAIMER: The author (Ian Conway) owns shares in Scottish Mortgage Investment Trust

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.