Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

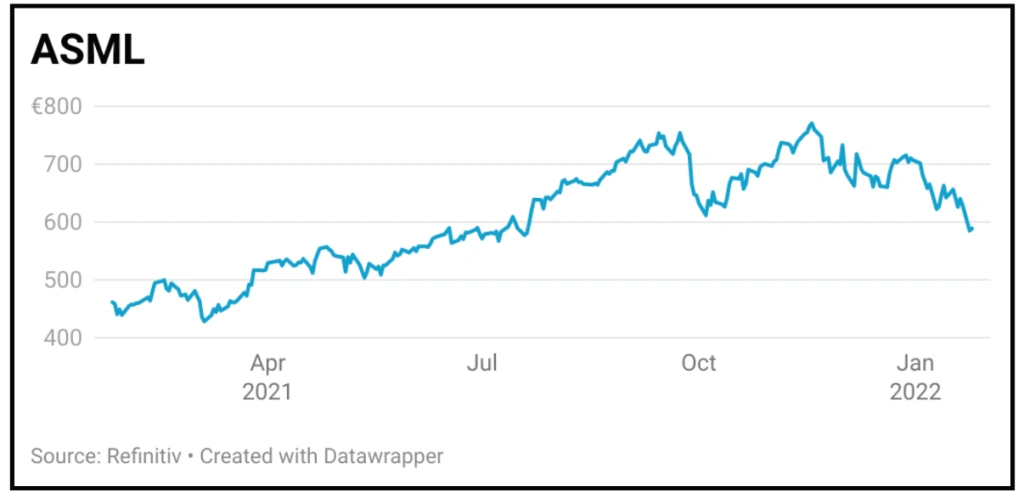

magazineDespite doubling ASML remains one of our top picks

ASML (ASML:AMS) €592

Gain to date: 123.7%

Original entry point: Buy at €264.60, 23 April 2020

It isn’t often we recommend that readers continue to buy shares in a company when they have more than doubled but Dutch semiconductor equipment maker ASML isn’t like other companies.

Recent weakness, linked to a wider market correction, has created a compelling buying opportunity.

The firm is the global leader in chip lithography machines, the kit that makes chips, and is the number one supplier to the world’s largest chipmakers in the US and Asia such as Micron, Samsung Electronics and Taiwan Semiconductor.

Moore’s Law, which says that the number of transistors on a silicon chip will double every two years, has driven the growth of computing power and therefore global economic growth for 30 years.

As the power of chips has grown, so their applications have expanded benefiting all kinds of industries. For example, the cost of generating solar energy has fallen by 20% every year for the last decade thanks to advances in chips, so the price per kilowatt-hour today is where a decade ago the International Energy Agency thought it would be in 50 to 100 years from now.

The current surge in demand for chips is largely due to what is known as ‘edge computing’, where data processing is done at or near the source of the data rather than at a remote centre.

Managing traffic systems or an oil rig are prime examples of new ‘edge’ applications where data needs to be managed on-site and be available in real time.

ASML has been at the forefront of pushing chip-making technology forward for decades, and with its extreme ultraviolet or EUV machines the firm believes it has ensured at least another decade of progress in computing capacity, and its customers can’t get enough of its equipment.

According to the company’s latest update (19 Jan) it is already running at 100% of capacity and it still has orders for 50% more machines than it can make. This demand is not just for its state-of-the-art EUV machines but also for its deep ultraviolet or DUV machines which are based on 30 year-old technology.

In fact, customers are so desperate for its kit that they are asking the firm to ship it to their factories so that final testing and certification can be done in situ, which has never happened before.

Even after last year’s exceptional 33% sales growth the firm expects them to grow 20% this year, meaning revenues will have doubled since 2019. That makes ASML a very rare and valuable company indeed.

SHARES SAYS: Long-term investors should keep buying.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.