Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

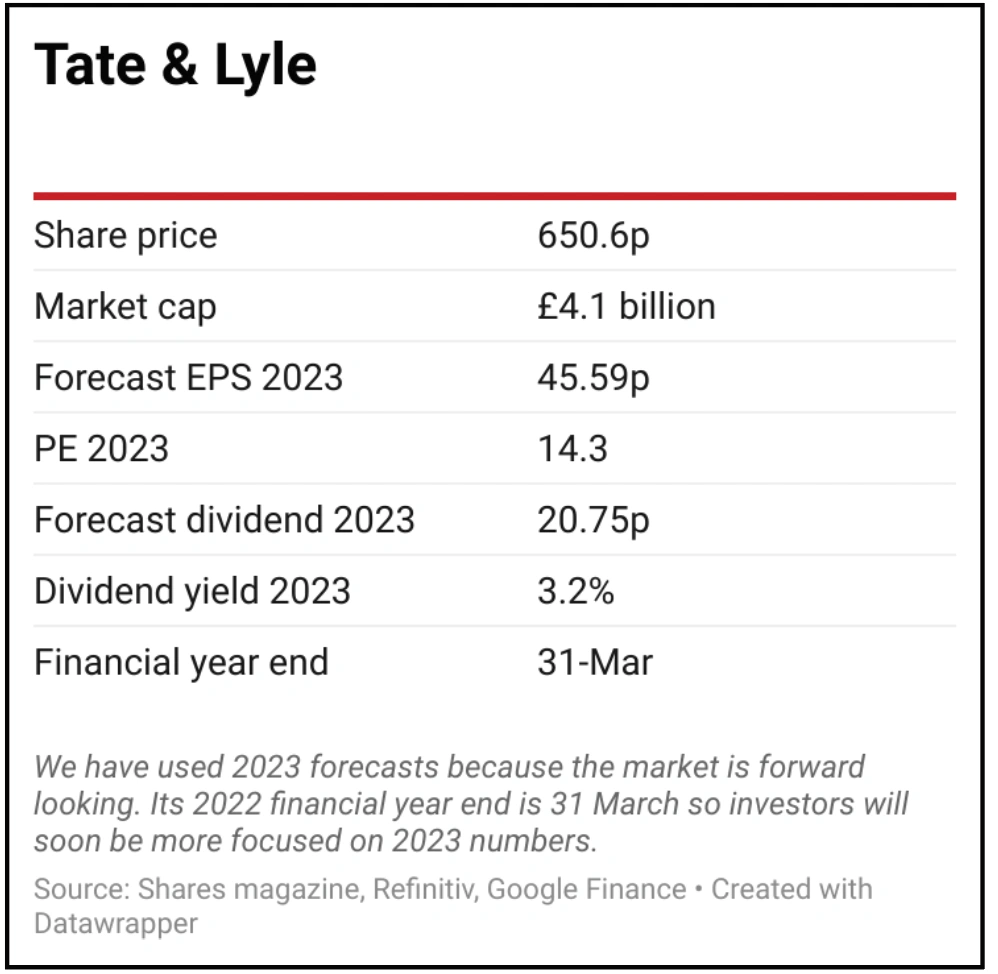

magazineStock pick for 2022: Tate & Lyle

Investors have an opportunity to buy Tate & Lyle (TATE) at an approximate 50% discount to ingredients peers. The FTSE 250 constituent’s imminent sale of a controlling stake in its North American Primary Products business will create a higher quality, ‘new’ Tate & Lyle with superior growth prospects which should drive a material rerating of a misunderstood stock.

Tate & Lyle is a global provider of corn-based sweeteners, starch ingredients and sucralose zero-calorie sweetener. The core business going forward is its specialty ingredients arm, Food & Beverage Solutions, which produces sweeteners, texturisers, fibres and stabilisers for beverages and dairy products, soups, sauces and dressings.

Concerns over cost inflation and the complexity of the business separation have weighed on sentiment towards Tate & Lyle, but the split will result in a sharper focus on fast growing, higher margin operations and allow Tate & Lyle to accelerate investment in innovation.

The company will split into two during the first quarter of calendar 2022, then pay a special dividend of around £500 million. Although the refocused, new-look Tate & Lyle plans to reduce the dividend to reflect the reduced earnings base, the payout ratio and progressive dividend policy will be maintained.

Robust first half results (4 Nov) for new Tate showed adjusted pre-tax profit up 20% to £85 million. Food & Beverage Solutions delivered double-digit organic growth across all regions, while revenue from new products rose by almost 50%. The results also confirmed that Tate & Lyle is managing cost pressures through price increases and productivity measures.

The trends driving Food & Beverage Solutions’ growth should continue, principally consumers’ demand for healthier foods and drinks that are lower in sugar and calories, with cleaner labels and added fibre. Acquisitions, notably the Sweet Green Fields stevia business, are also helping to accelerate new product revenue growth.

Risks to consider include new Covid variants, which could halt the recovery in out-of-home consumption, as well as dollar weakness, as the bulk of the group’s revenues are generated in the greenback and it reports in sterling.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG