Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStock pick for 2022: Pets at Home

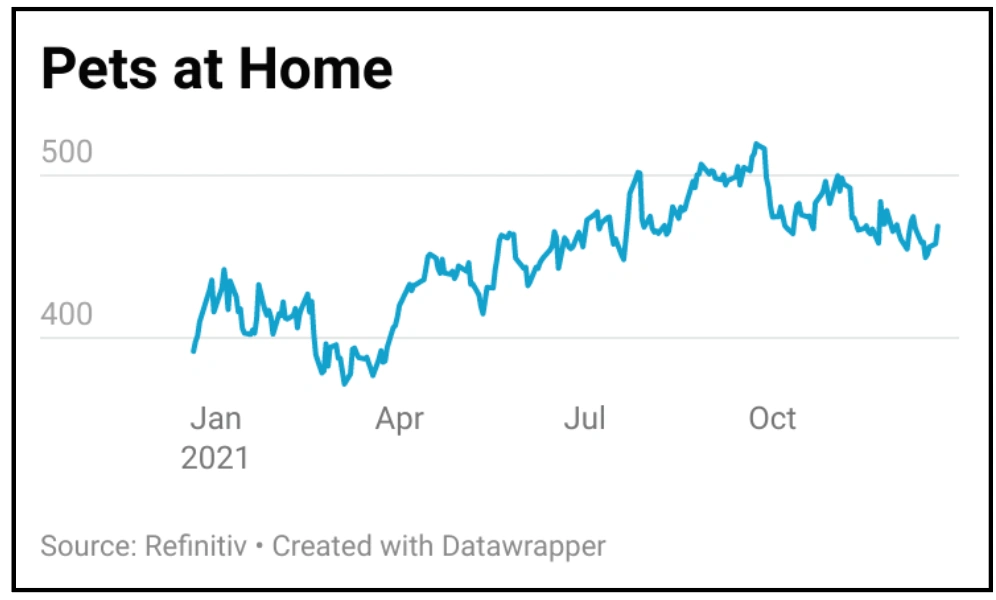

Pets at Home (PETS) is in an excellent position to take advantage of the opportunities created by an expanded pet population.

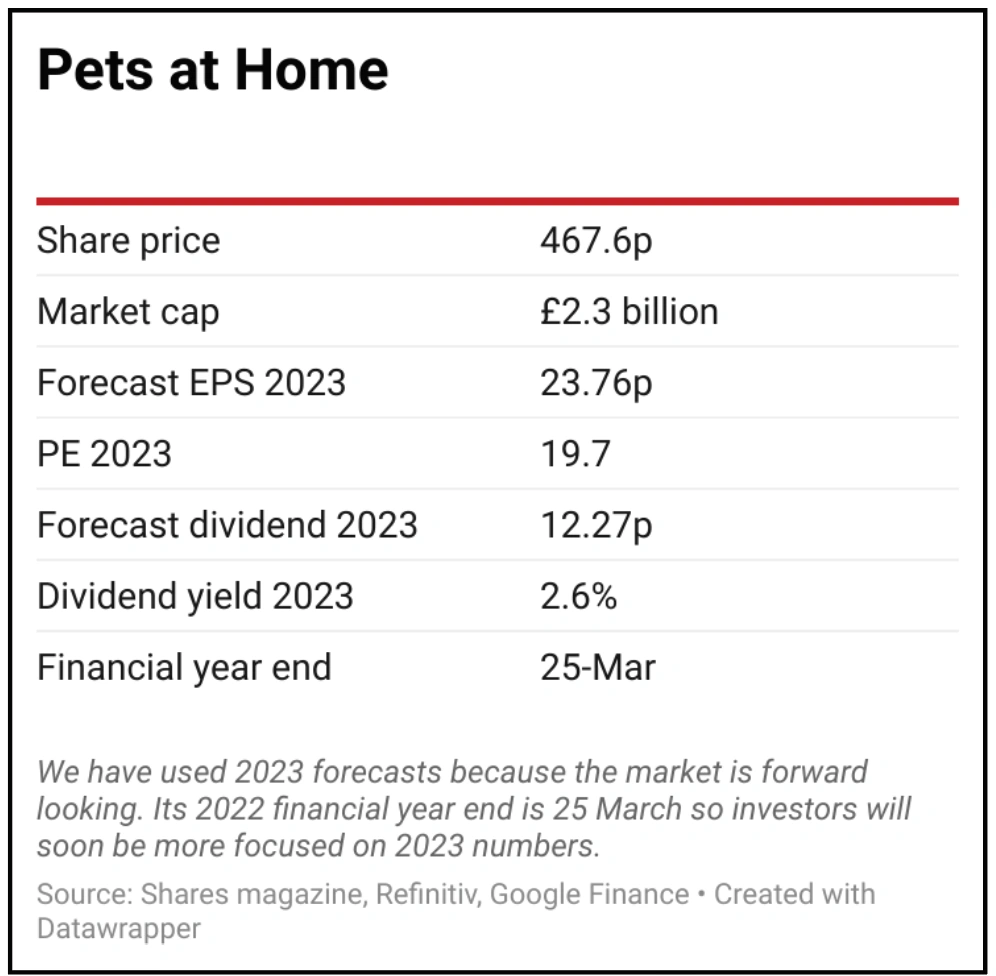

It’s one of those stocks easily dismissed by some investors given that the share price has already been a strong performer. We view it as a great business with plenty of room to continue growing earnings and where the valuation is still reasonable.

Unlike some other activities which gained popularity during lockdown, taking in a new pet is a long-term commitment for most people, not a fad.

There are three main ways Pets at Home will benefit from this market opportunity. First through people buying food, treats, bedding and toys for their animals; second as people look to keep their furry friends tidy at its in-store grooming salons; and third by offering veterinary services.

The veterinary business, under the Vets4Pets banner, is high margin and includes directly owned practices, both inside Pets at Home stores and in standalone locations, as well as those operated through a recently launched partnership model.

By agreeing joint ventures with vets, Pets at Home can grow this part of the group rapidly without incurring significant costs.

The firm’s VIP, Puppy and Kitten Club memberships are a smart way of securing customer loyalty. Effectively you gain access to things like in-store discounts and advice, a network of other members who you can call on if your pet goes missing and a donation to an animal charity every time you shop.

These initiatives should help Pets at Home to protect and grow market share, which stood at 23% in the most recent financial year according to the company, by warding off non-specialist rivals like the supermarkets, which are probably the clearest competitive threat.

The company has done a decent job of mitigating supply chain issues, helped by the fact its product range is sourced in the UK and is not perishableor seasonal.

The man behind Pets at Home’s successful strategy, Peter Pritchard, is set to leave in summer 2022. He hands over a business in great shape.

The company is forecast to report £135 million pre-tax profit for the year to March 2022, rising to £152 million in 2023 and £168 million in 2024, according to analyst consensus estimatespublished by Refinitiv.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG