Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy machines beat managers in 2021

2021 has been a pretty grim year for active managers, with passive funds ruling the roost and delivering better returns for investors on average.

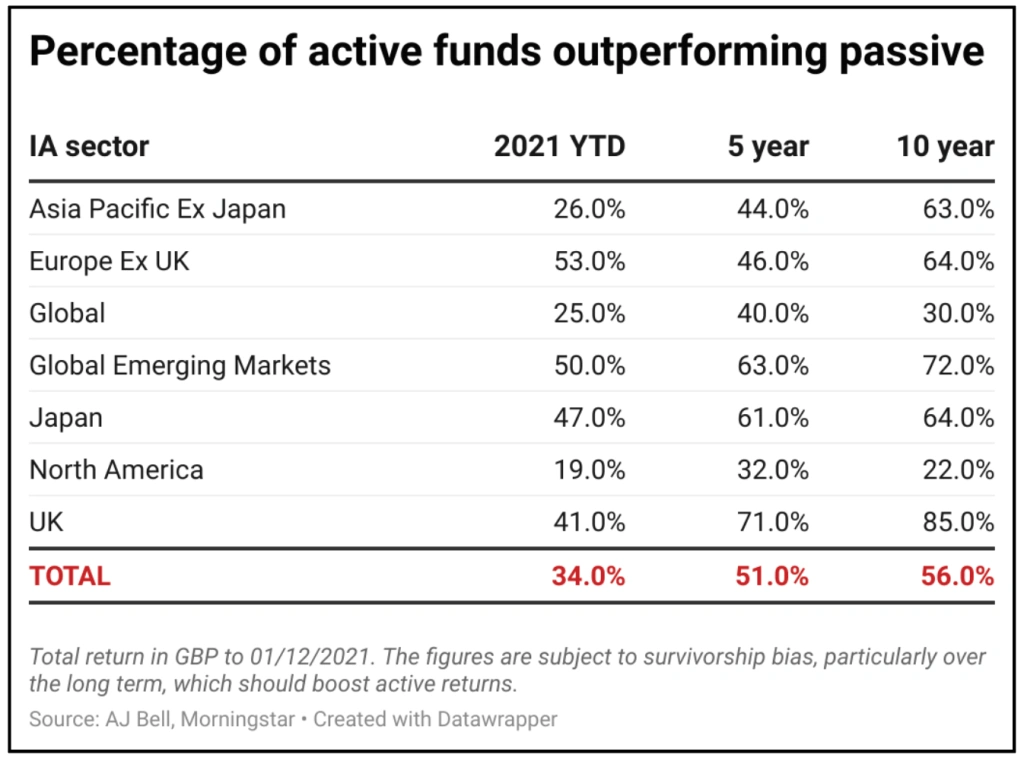

AJ Bell’s latest Manager versus Machine report shows that only a third of active equity funds, 34% to be precise, beat a passive alternative this year. Outperforming active funds were particularly sparse in the Global and North America sectors, which are hugely important because they are two of the most popular areas for investment, accounting for £270 billion of investors’ money.

In the North America sector, fewer than one in five active funds outperformed a passive alternative in 2021, and the picture is not much improved when looking over a 10-year period. This is no doubt partly down to the fact the US stock market is poured over by so many analytical eyes, that active managers naturally find it more difficult to find an edge.

But the continued market domination by a small number of large tech stocks may also be feeding into the equation, reinforcing the implicit passive principle that big is beautiful, and punishing those who take a dissenting view with their portfolios.

Seven tech companies command the top of the US stock market, including Apple, Microsoft and Nvidia. While not all have prospered over 2021, as a group they have tightened their grip on the US stock market. Together they now make up 27% of the S&P 500, up from 24% at the beginning of 2021.

BETWEEN A ROCK AND A HARD PLACE

US active managers find themselves between a rock and a hard place when it comes to participating in the continued ascendancy of these tech titans.

In order to have a neutral position, an active manager running a US fund would have to allocate 27% of their portfolio to these seven companies. That would still leave more than a quarter of their portfolio simply pegged to the market, which would actually be losing ground against a comparative tracker fund because of higher charges.

On the other hand, any US active manager who dared not to hold any of these stocks over the course of 2021 would have found themselves facing some uncomfortable questions around performance.

LEAKAGE INTO GLOBAL SECTOR

The issues affecting active managers in the US have increasingly leaked into the Global sector, seeing as the US stock market has grown to such an extent that it now makes up around two thirds of the world index.

Global tracker funds therefore increasingly resemble US trackers, making it more difficult for active funds to compete in this arena while the US maintains its ascendancy. If the raging US bull market comes a cropper though, this performance differential could get turned on its head, particularly seeing as the average global active fund is around 8% underweight the US compared to passive peers.

The UK funds market, by contrast, has been a bright spot for active managers over the longer term, with the average active fund returning 134% compared to 95.6% from the average passive fund over 10 years. However some structural factors in the funds market go some way to explaining this differential.

UK ACTIVE MANAGERS SHINE

The UK All Companies sector is home to a significant number of funds which focus on the small and mid cap area of the stock market. Not only have small and mid-caps significantly outperformed the big blue chips over the last 10 years, they are also a fertile hunting ground for active managers to pick out hidden gems, as they are not as well scrutinised by the wider market.

There are also a fair number of older tracker funds investing in UK shares, which charge higher fees, and therefore drag down the performance of passive funds in this market.

As ever, averages and aggregate data don’t tell the whole story, and individual investors do have the opportunity to improve their own lot through fund selection, both active and passive.

For active investors this means picking seasoned fund managers who have proved their performance potential, or their ability to deliver a set outcome such as a high level of income or a low level of volatility, though of course there can never be a cast iron guarantee of future performance.

For passive investors, selection entails picking funds that effectively track appropriate market indices at the lowest price possible, as charges will be a key determinant of returns.

Many investors of course choose to mix and match passive with active funds, and AJ Bell’s Manager versus Machine analysis suggests where each strategy might be in its element. While the long-term performance numbers from the US and Global sectors look pretty damning for active investors as a whole, there have been active success stories here, for instance Fundsmith and Baillie Gifford.

LIFE COULD GET TOUGHER FOR PASSIVE VEHICLES

It’s also worth bearing in mind that market performance in the last 10 years has been heavily influenced by ultra-loose monetary policy and the digitalisation of the global economy. Should one, or both, of these trends moderate or even go into reverse, life might not prove so breezy for the passive machines that simply invest money according to the size of companies in the market.

DISCLAIMER: Financial services company AJ Bell referenced in this article owns Shares magazine. Tom Sieber who edited this article owns shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG