Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFund managers: stocks that let us down in 2021

In the second part of a two-part series Shares talks to various fund managers about the stocks that didn’t work out as they expected in 2021. They explain what went wrong and why the market reacted in the way it did.

The first part of the series can be read here and reveals 12 fund managers’ top stock picks for 2022.

Neil Goddin, co-manager, Artemis Positive Future Fund (BMVH597)

Stock that disappointed in 2021: Coursera (COUR:NYSE)

Our education system is costly and arguably ineffective. Given healthcare advances, our children and grandchildren could live to well over 100 and be working way beyond their 60s, so why do we funnel them into an expensive degree system where they’re supposed to complete their education by 22? The sector is ripe for disruption.

Coursera joined the US stock market in 2021. The company develops online education programmes delivered through a smart learning platform. It has around 80 million registered learners and works with 200+ leading universities and industry partners, delivering courses up to degree level – some free, most charging.

The aim is to offer courses that are affordable, can be accessed from anywhere and are thus more inclusionary than traditional methods of education.

Coursera’s shares have been weak despite delivering results ahead of expectations. Fears around a drop in interest post the pandemic miss the longer-term opportunity for disruption of a very stale education sector.

Samantha Gleave, co-manager, Liontrust European Growth Fund (B4ZM1M7)

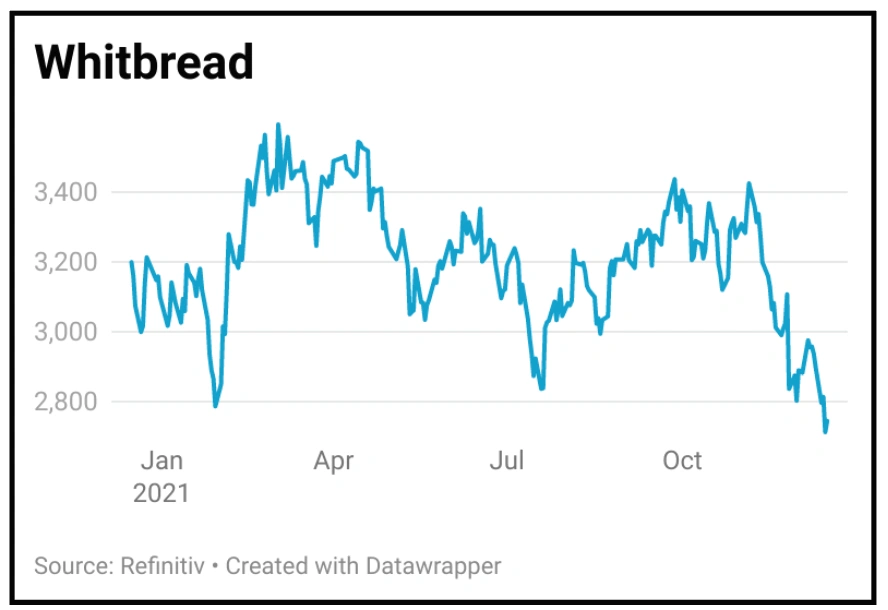

Stock that disappointed in 2021: Whitbread (WTB)

Prolonged Covid restrictions curtailed trading for even longer than expected for the beleaguered hospitality sector.

While leisure demand for Whitbread’s Premier Inn hotel rooms picked up over the year, particularly during the summer, demand from business customers in the UK and in its international sites remained depressed for most of 2021.

At the same time, the company has faced some negative short-term issues with labour shortages (and therefore subsequent high wage inflation), supply chain issues and more recently utility inflation risk in the UK. These factors adversely impacted Whitbread’s operating margin.

Kartik Kumar, co-manager, Artemis Alpha Trust (ATS)

Stock that disappointed in 2021: Just Eat Takeaway (JET)

Just Eat did very well through lockdown and its share price increased significantly. However, this year its share price has declined steadily, and the shares are trading materially below pre-Covid levels despite the pandemic lasting much longer than most expected.

Social restrictions helped to significantly expand the company’s user base of customers and restaurants with many habits proving sticky.

These enduring benefits have been overshadowed by concerns over greater competitive intensity and the imposition of delivery fee caps in the US.

The market has been ruthless over any missteps from companies earlier perceived to be pandemic beneficiaries, as seen by the broader decline in e-commerce market values.

We continue to feel that Just Eat is well placed to succeed with its uniquely profitable market positions and highly motivated management team. Despite a pull-forward of adoption during the pandemic, we believe the online food delivery industry is still in its early stages of evolution.

Simon Edelsten, co-manager, Mid Wynd Investment Trust (MWY) and Artemis Global Select Fund (B568S20)

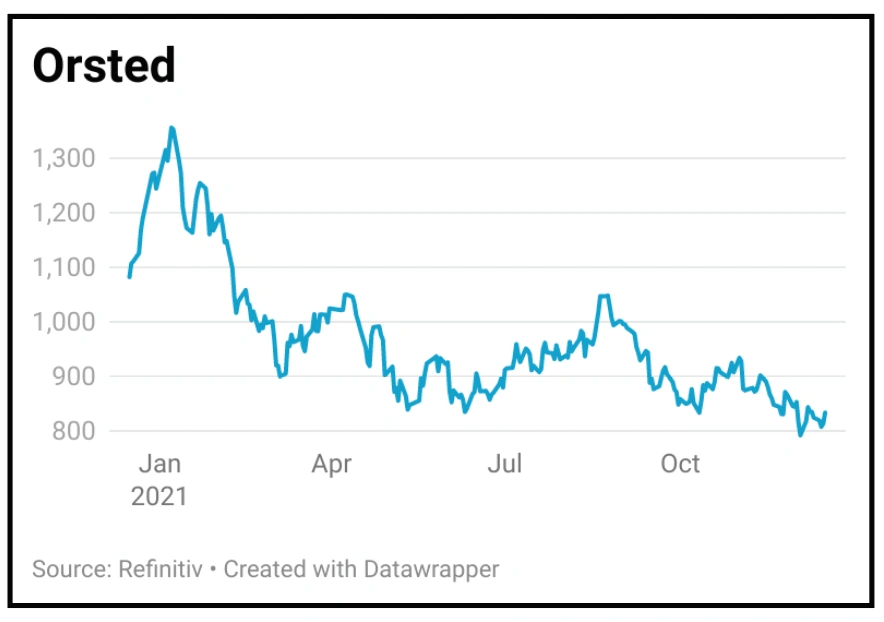

Stock that disappointed in 2021: Orsted (ORSTED:CPH)

From the beginning of 2018 to the beginning of 2021 Orsted shares travelled in a pretty steady upward direction – rising more than 250%.

We hoped that would continue, but fairly early on in 2021 realised things had changed. In this case I think the market had begun to get it too.

Orsted is the world’s leading builder of offshore wind farms. Unfortunately, as greater government attention has turned to accelerating renewable energy production, state loans have allowed many large less-experienced companies, such as the main oil producers, to enter this sector which has driven down returns. While Orsted will doubtless be busy over the next 10 years, its ability to make good profits out of future development activity seems hampered. Its shares are down 36% year to date.

Charles Luke, fund manager, Murray Income Trust (MUT)

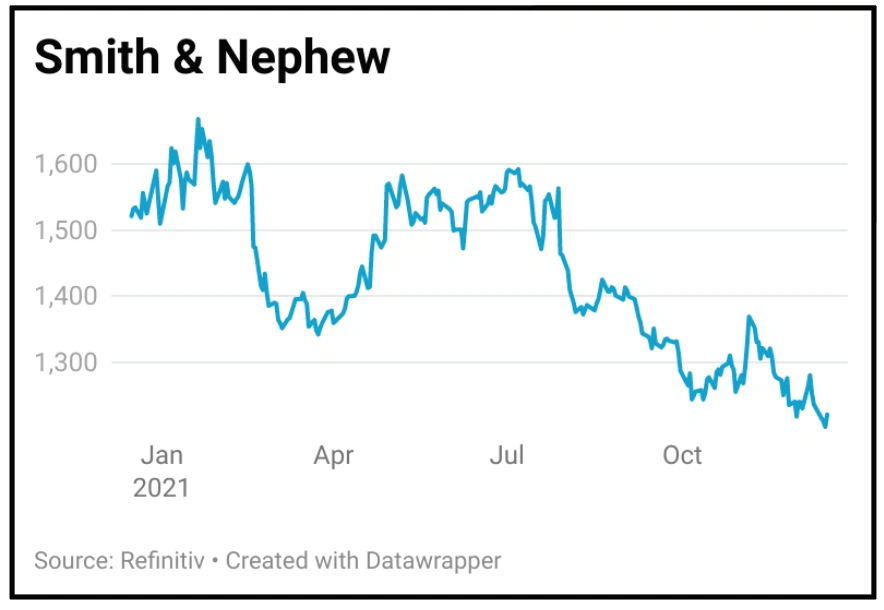

Stock that disappointed in 2021: Smith & Nephew

There are several reasons why the trade on Smith & Nephew hasn’t worked during 2021. First, the recovery in elective surgery has been fragmentary and certainly not helped by the emergence of the Delta variant and now Omicron as well.

Second, pricing in China has come under pressure from a move to volumebased pricing in that market.

Third, margin expectations have been downgraded for a variety of reasons, including foreign exchange, supply chain issues, higher freight costs, more R&D spend and the impact of dilutive acquisitions.

Looking forward the company should benefit from pent-up demand, margin pressures should mostly reverse or ameliorate, and the product portfolio is improving.

James Henderson, co-portfolio manager, Henderson Opportunities Trust (HOT)

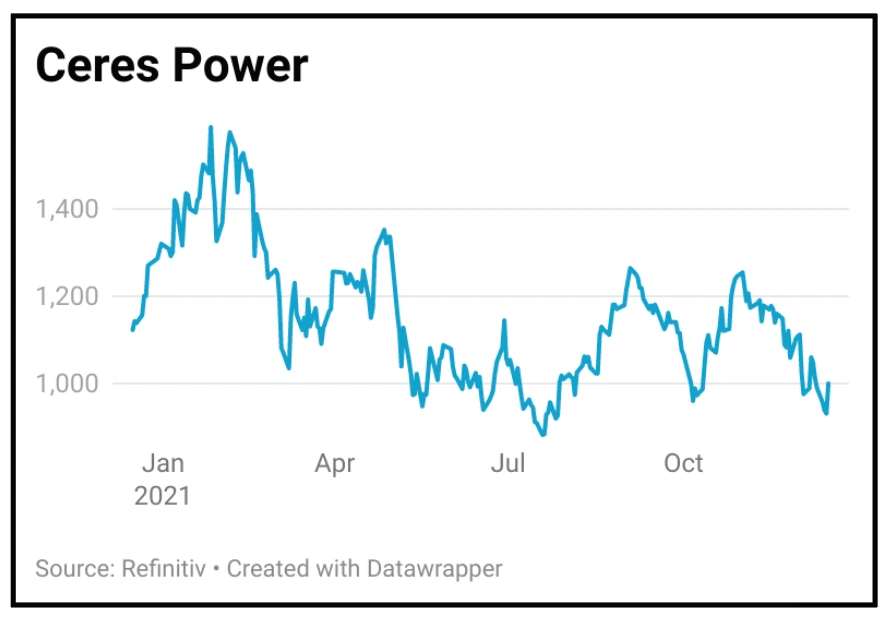

Stock that disappointed in 2021: Ceres Power (CWR:AIM)

Ceres Power is a fuel cell company which provides energy from smaller scale buses to, ultimately, large power stations.

The company has been in Henderson Opportunities Trust’s portfolio for seven years and for much of that time it did very little in terms of the share price because, while fuel cell technology is well known, the commercialisation of the fuel cell has been demanding and difficult.

Ceres Power has needed Bosch and the Chinese to help with the commercialisation of it, and their capital, too. Bosch became a large shareholder in Ceres, as did the Chinese.

Its share price in 2020 was very strong. It went up several times because the whole area became of great interest to investors, as belief in the need to move away from fossil fuels resulted in increased interest, as did the realisation that something had to happen.

Expectations probably got ahead of themselves and, therefore, this year it has drifted back. But it is making very good progress operationally.

Charles Montanaro, fund manager, Montanaro UK Smaller Companies (MTU)

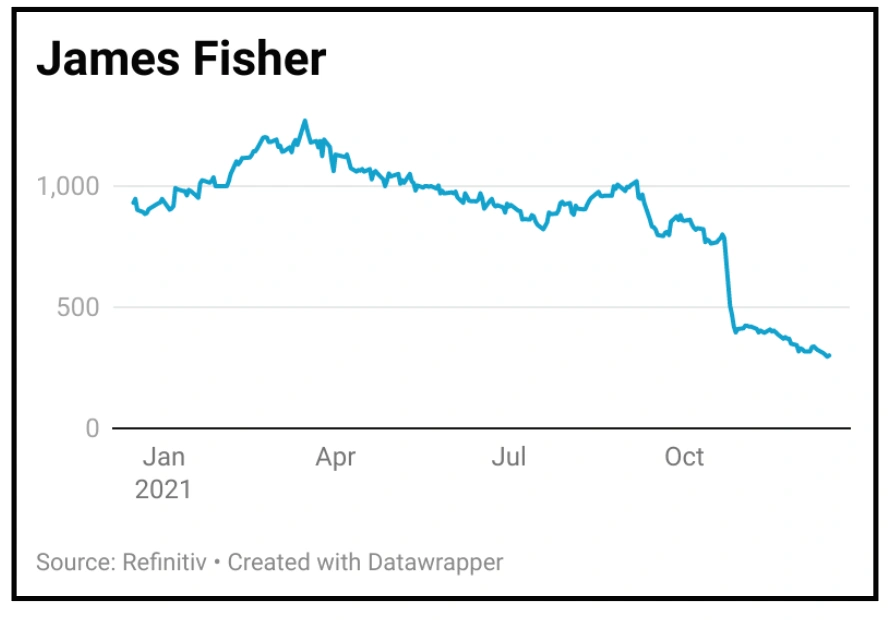

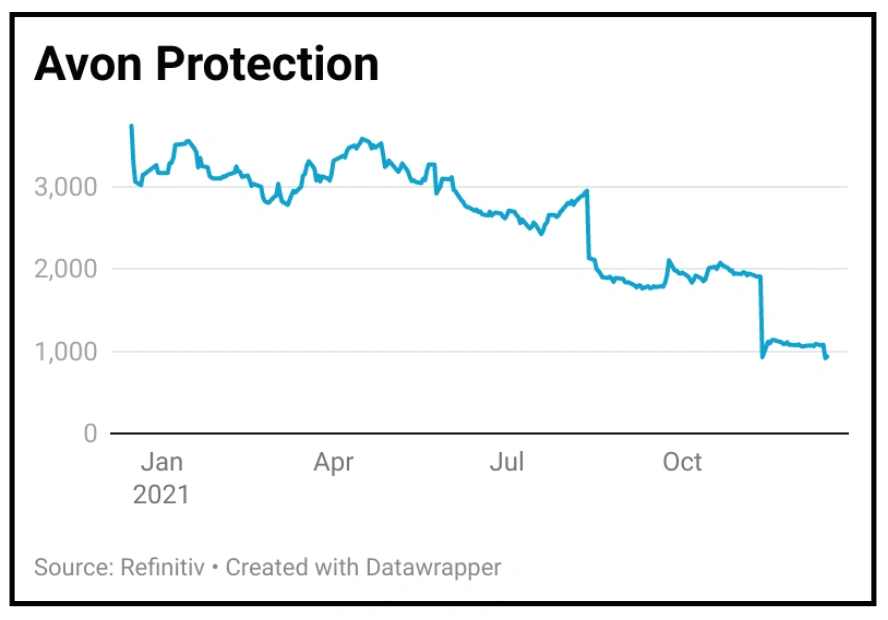

Stocks that disappointed in 2021: James Fisher and Avon Protection

James Fisher wins the wooden spoon: a mini conglomerate operating in the global marine, renewables, offshore oil, nuclear, defence and shipping industries.

Weakness in the marine support division, largely a result of buying two dive support vessels (Paladin and Swordfish) for oil and gas exploration in West Africa, led to losses. An ambitious restructuring plan is taking longer than expected.

This wooden spoon award is shared with Avon Protection which produces life critical products such as respirators, powered air systems, and filters alongside ballistic protection (helmets and body armour) to the military.

Having done everything right in 2020, the reverse has been the case in 2021. It committed the cardinal sin of raising expectations that a setback in the body armour division had been resolved when it was wasn’t.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG