Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine8.5% share price return from our 2021 stock picks

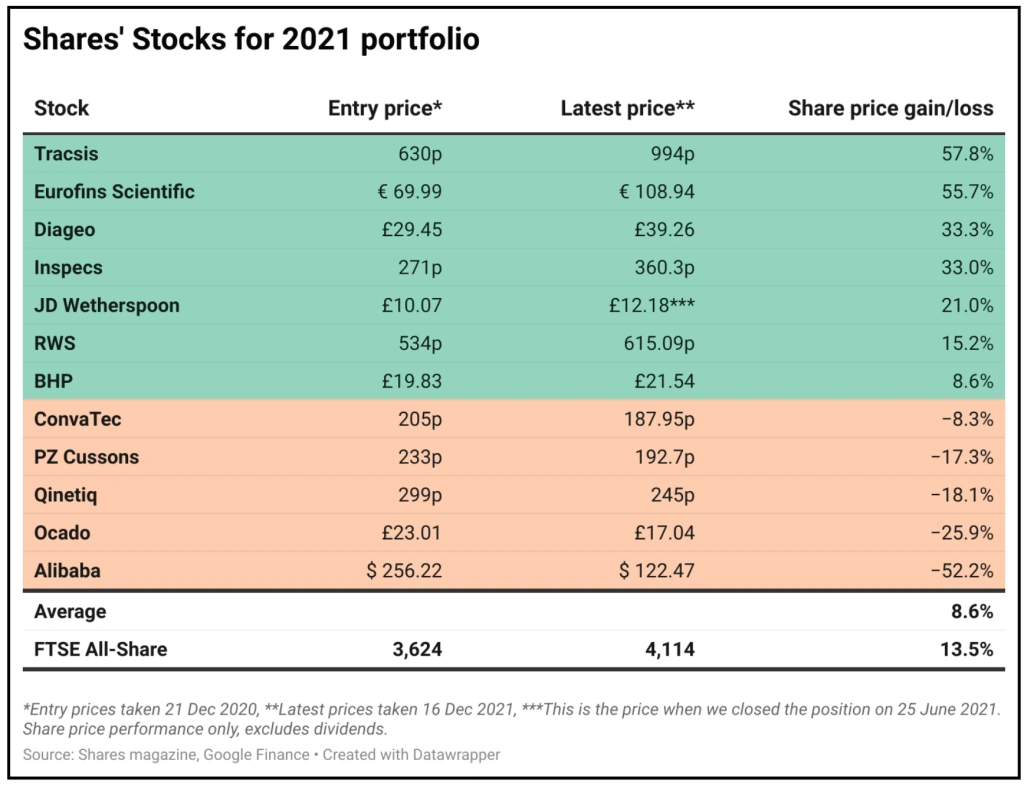

Constructed last December from shares in UK, European and US markets, Shares’ ‘Stock picks for 2021’ portfolio was based on high conviction in 12 companies for the year ahead. While more than half of them have subsequently done well, there were a handful of disappointments.

The net effect is a decent 8.6% return excluding dividends – that’s higher the historical average 6% to 7% from equities including dividends. However, it is below the 13.5% return in 2021 from the FTSE All-Share which is the benchmark for UK shares.

Our performance shows how difficult it is to be an active investor and consistently beat the market. However, our track record over a longer term remains good.

Shares’ annual stock portfolio has outperformed the market in seven out of the last 10 years, some of those periods by a considerable margin.

Three of those 10 years saw the markets deliver a negative performance and we outperformed in each of the years. In two of those years, we delivered a positive return and in the third our portfolio fell by considerably less than the market, showing we are good at preserving capital which is incredibly important for investors.

After all, legendary investor Warren Buffett says the first rule of investing is not to lose money.

ANALYSING 2021 PERFORMANCE

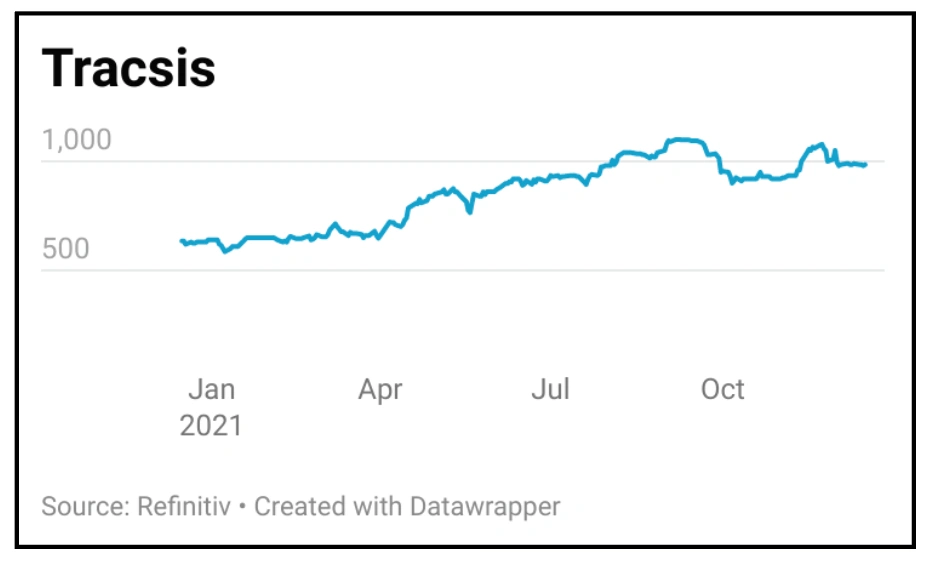

Six of our seven winners in the 2021 portfolio racked up double-digit gains, which is encouraging. The best among them was transport infrastructure and analytics firm Tracsis (TRCS:AIM), up 57.8% and which saw improving momentum in both its rail division and data business, leading to forecast-beating revenues and earnings.

Close behind was testing and certification group Eurofins Scientific (ERF:EPA) with a 55.7% gain. Its revenues surged more than 30% in the first nine months of the year and the company raised its full year guidance as Covid-related clinical testing supplemented strong underlying organic growth.

Eyeware company Inspecs (SPEC:AIM) was another hit with investors due to its strategy of consolidating its supply chain and pushing through synergies while continuing to drive sales particularly in the higher price bracket leading to analysts upgrading earnings forecasts.

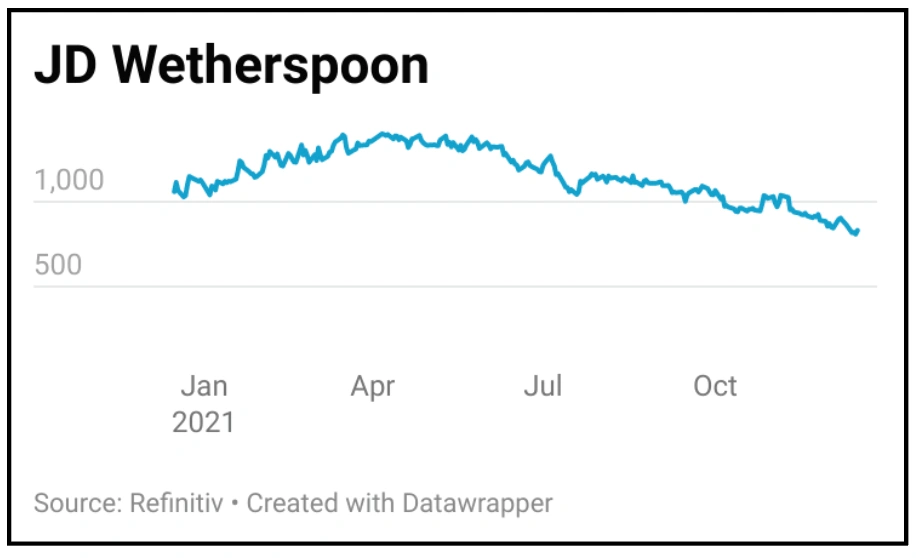

We also enjoyed a good run in two ‘reopening’ stocks, namely spirits maker Diageo (DGE) and pubs group JD Wetherspoon (JDW).

Diageo benefited from the continued trend towards premium drinks thanks to its roster of well-known brands such as Johnnie Walker, Smirnoff and Tanqueray on the back of a return to socialising.

Wetherspoons also performed well as loyal customers flooded back to its pubs. Given the strong rise in the shares by late June and the opposite trend in analysts’ estimates we took profits in the position at the half-year point, fearing a share price correction, which duly occurred.

Language services and technology group RWS (RWS:AIM) beat the market, although our sense is investors expected more than they got in terms of synergies from the SDL deal, even though the firm raised its margin guidance.

Also, the departure of chief executive Richard Thompson, who masterminded the group’s growth in the last few years, introduced a degree of uncertainty regarding future strategy.

Our final winner was mining giant BHP (BHP), which had a choppy year hitting highs of nearly £24 and plumbing lows close to £18. Despite landmark deals to merge its energy assets with Woodside and dispose of its majority interest in a coal joint venture with Mitsui, which will boost its green credentials significantly, the decision to unify its shares and move its primary stock listing to Sydney meant many funds were forced sellers which counted against it.

THE WEAKEST LINKS

Medical products group ConvaTec (CTEC) was on course to beat the market at the mid-year stage but after warning of higher raw material and freight costs in July the shares have kept falling, even though the firm has raised its organic sales growth forecast twice since.

It was a similar story at defence and security firm Qinetiq (QQ.), which was keeping pace until October when it warned that supply chain disruption had impacted a large customer programme and could result in a hefty downgrade to its full year outlook. The news took the shine off a strong first half performance which also included a 25% jump in order intake despite a tough prior-year comparison.

Consumer goods group PZ Cussons (PZC) was a victim of its own success, after sky-rocketing sales of its Carex hand sanitiser last year meant growth this year was going to be hard to match. The company warned in September it faced rampant cost inflation and its full year outlook depended on no further cost headwinds or supply chain or Covid-related disruptions, which the market read as downside risk to its forecasts, prompting a sell-off.

Our two biggest disappointments were also pandemic ‘winners’ which failed to shine, for different reasons. Online grocery delivery firm Ocado (OCDO), which could barely keep up with demand during the pandemic, found itself left on the shelf as many investors chased ‘value’ and reopening trades, while a lack of news flow on winning new clients for its technology platform turned others off.

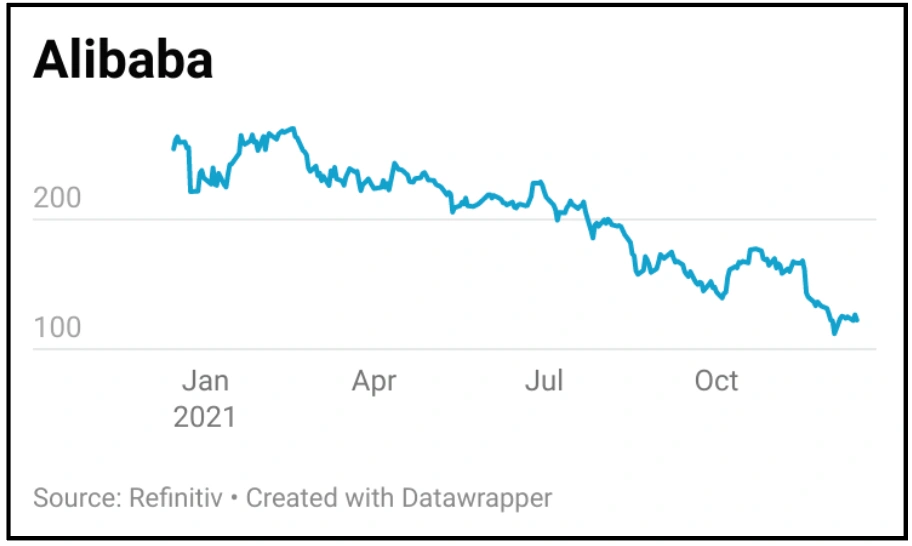

In retrospect, saying to buy shares in internet shopping giant Alibaba was risky as it was already on the Chinese regulator’s hit list last year, having had to shelve its Ant Group float. It was then slapped with a $2.8 billion anti-trust fine in April and in September the government said it wanted to break up its Alipay mobile payment system. Earnings forecasts continue to slide, so despite the share price fall the risk hasn’t gone away.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG