Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe smart way to play a rebound in the Chinese stock market

The MSCI China index is down by more than 20% over the past three months in response to regulatory clampdown in the country and a series of downgrades to Chinese growth forecasts. This has provided further ammunition to sceptics of the Chinese economic miracle, who argue that investing in the region is an increasingly risky proposition.

However, there is a compelling argument that we have reached an inflection point for Chinese equities.

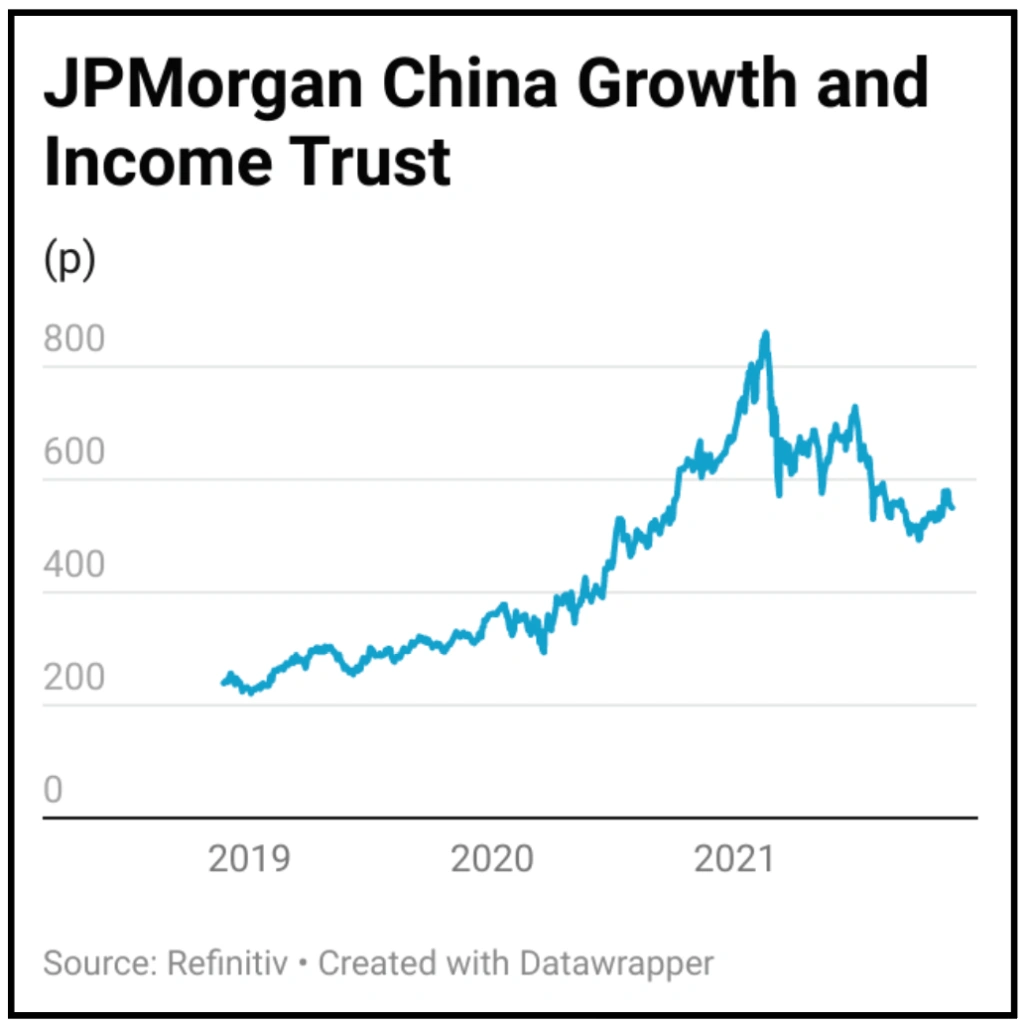

JPMorgan China Growth and Income Trust (JCGI) offers investors an interesting play on Chinese companies that are benefiting from the transition to a more consumer driven economy. It pays dividends every quarter.

The trust has an impressive track record of consistently outperforming its MSCI China benchmark by a significant margin on a three, five and 10-year basis. It currently offers a 4.1% yield, and trades on 3.7% discount to net asset value.

WHY THE RECENT SETBACK?

Investor sentiment in the region has been undermined by a wave of policy tightening and tougher regulation targeting sectors from property to technology. These fears have been compounded by concerns that Evergrande, the world’s most indebted property firm, will default and cause contagion in the Chinese banking sector.

JPMorgan strategist Tai Hui says there are two underlying motives behind the recent regulatory changes imposed by the Chinese government. First, common prosperity is designed to reduce the proliferation in income inequality. This is perceived as being a potential threat to social stability.

Second, several of the policy changes are intended to arrest the decline in the Chinese birth rate. The rising costs of education and housing are believed to have contributed to this trend.

According to Hui, while attempting to curb monopolistic activities, these initiatives are far from being inherently anti-business. He adds: ‘The government is highly cognisant that private enterprise has driven the rapid rise in living standards over recent decades.’

CHINA MARKET VOLATILITY IS NOT NEW

Hui highlights that over the last 10 years there have been four periods of heightened Chinese equity market volatility.

The first was between April and September 2011, when the market experienced a peak to trough correction of 30%, the second during May 2015 and February 2016 was particularly savage with a peak to trough correction of 40%. This was followed in January to October 2018 by a more modest market retracement of 30% (peak to trough).

Hui believes that the current pullback in the MSCI Chinese index which began in February and currently represents a 23% decline, is ‘comparable with previous market corrections, if not a little less aggressive’.

ENCOURAGING OUTLOOK

‘If you look at the performance, one, three and six months after the market trough, typically we get very respectable returns,’ says the JPMorgan strategist.

‘I expect economic data to pick up in the first quarter or at least the first half of next year, and that fits in quite nicely with the experience of the Chinese markets. When growth starts to improve you should be expecting a better performance from the Chinese market.’

KEY PORTFOLIO THEMES

JPMorgan China Growth and Income Trust fund manager Rebecca Jiang says her portfolio is geared to secular growth sectors including technology and healthcare.

She believes there are two key drivers that will benefit the technology sector. First, the Chinese manufacturing sector needs to become smarter and more digitised. This will facilitate its transition from being labour intensive and low value-added, into an industry creating higher value-added products and services. Second, rising labour costs are driving the adoption of automation to increase efficiency.

Carbon neutrality is another key investment theme for the trust, given China’s commitment to both peak CO2 emissions before 2030 and carbon neutrality by 2060.

Jiang emphasises that ‘Shanghai has an electric vehicle penetration rate of over 35%, which is significantly higher than Europe’. She adds: ‘China has the most comprehensive electric vehicle supply chains, it is very competitive on a global scale, and it is benefiting from increasing market share.’

The final theme is consumer-related businesses. Jiang suggests that as China consumers become more affluent, they demand better and healthier lives and products. Demand for innovative quality drugs and healthcare services will enable Chinese companies exposed to these areas to grow ahead of GDP.

RECENT PORTFOLIO ACTION

Jiang has taken advantage of recent market volatility to increase the trust’s weighting to technology conglomerate Tencent and video sharing website Bilibili.

Outside of technology Jiang has also added to her position in residential property management company Country Garden Services. Jiang likes the sticky nature of the business, and the ‘abundant scope for growth due to consolidation’. She also argues there is scope for the group to provide additional higher margin services to property owners.

This part of the world should be considered higher risk from an investment perspective and so the JPMorgan trust is only suitable for individuals who understand those risks and are patient.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

- DotDigital share slump means you can buy cheaper now

- Growth, profit and M&A to drive CentralNic higher

- Plenty of reasons to remain positive on Euromoney

- The smart way to play a rebound in the Chinese stock market

- All-weather trust Ruffer is selling new shares at a discount

- Investors overreact to Frontier Developments' downgrade