Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInflation-busting dividends: six stocks and funds providing a decent, growing income

UK inflation is at a 10-year high. Rising prices have been on the agenda for months but in October the impact of the energy crisis really bit as the CPI measure of inflation hit 4.2%.

This higher cost of living matters to all of us, not least because we now need a return of at least this level to avoid the so-called ‘real’ value of our savings being eroded.

While interest rates are poised to go up, the returns from cash in savings or current accounts fall well short of this 4.2% level. This makes a compelling case for investing your money instead.

In this article we have identified stocks and funds which are forecast to pay inflation-busting dividends which are also expected to grow faster than rising prices.

The list of names includes insurance firms Admiral (ADM) and Legal & General (LGEN), housebuilder and regeneration specialist Vistry (VTY), as well as a vehicle which invests

in music royalties and a real estate investment trust securing inflation-linked income from GP practices.

INFLATION-BUSTING INCOME

Investment bank Berenberg recently conducted a screening exercise of the market to identify companies with positive income characteristics. Analysts Edward Abbott and Jonathan Stubbs commented: ‘UK equities and real estate continue to offer some attractive yield opportunities.

‘This is relevant for investors looking to protect capital against rising inflation risk and could prove an important component of income portfolios over the coming quarters.’

Berenberg’s search criteria included dividend growth, whether companies are well positioned heading into an expected scenario of continued growth but rising inflation and bond yields; and the extent to which dividends are underpinned by earnings and cash flow, and supported by decent balance sheets. The table shows 12 names that tick the right boxes in its search.

We conducted our own screening exercise, looking for companies and trusts which pay a dividend yield of at least 4.2% with forecast growth of at least 4.2% in said dividend.

With many firms reducing dividend payments materially during Covid, some of the upcoming dividend growth looks artificially inflated, particularly given the impact of some planned special dividends.

To factor this in, we’ve restricted our search, at least in terms of individual company stocks, to those which have also delivered average annualised growth in the dividend of at least 4.2% over the past 10 years. We haven’t included this restriction for investment trusts, given that most of the high-yielding names on the list haven’t been on the market for a decade.

Miners dominate the list, but we think beyond the near-term there may be challenges in maintaining very generous dividends from here. This industry needs to invest in reducing emissions and in growth as it looks to capitalise on demand for metals to build assets like renewables and electric vehicle infrastructure.

From the list of 20 shares and funds we have selected six of the best ideas to help fight off the ravages of what is often called the cruellest tax.

GLOBAL INCOME FUNDS TO TACKLE INFLATION

It goes without saying that the increasingly globalised nature of today’s world means it has never been easier to gain income exposure from overseas equity and bond markets. This is a sensible option considering that recent data from Janus Henderson points to global dividends hitting pre-pandemic levels by the end of the year as third quarter figures surge.

This is particularly the case for companies in Europe, parts of Asia and emerging markets. Dividends jumped 22% year-on-year reaching $403.5 billion, an all-time high for third quarter figures, the study found.

There are several funds and investment trusts that will invest in income-paying equities anywhere in the world. This is a wide remit and can vary from fund to fund. Some funds will stick to companies in developed markets only, like Europe, the US and Japan, while others will also invest in emerging markets. There will also be variation in the size of companies that funds will invest in, which may tilt the risk balance.

Beating 4.2% UK inflation from the global dividend streams is a tough challenge. For example, JPMorgan Global Growth & Income (JGGI) aims to pay out around 4% of net assets each year through dividends paid quarterly, but its implied forward income yield of 3.2%, according to Trustnet data, falls short of most recent inflation figures.

The trust’s portfolio includes income payers like McDonald’s, ConocoPhilips and Wells Fargo as well as higher growth companies that pay lower levels of income, such as Microsoft and Mastercard. This plays to recent trends that have seen UK investors pull money out of dividend-paying British businesses into funds that invest in lower dividend payers around the world that have a greater potential for capital returns.

If these investors need income, they can take the money from their capital growth and dividends. Total share price and net asset returns have beaten the Investment Trust Global Equity Income benchmark over three and five years, but not all global income funds can say the same.

The Liontrust Global Equity (B9225P6) fund is ranked best in class over three and five years, according to data from researcher Yodaler. The fund’s own data shows it has posted returns of 70.1% and 95.1% respectively, versus the Investment Association’s Equity Income benchmark of 36.2% and 56.3%, yet investors would have done better buying an MSCI World ETF, the index having chalked up gains of 66.4% and 103.9% over the equivalent timeframes and cheaper than Liontrust’s 0.88% ongoing charge.

This illustrates that income seeking investors should take a close look at past performance relative to ETF options before backing an active fund with their cash.

INFLATION-BUSTING DIVIDEND PICKS

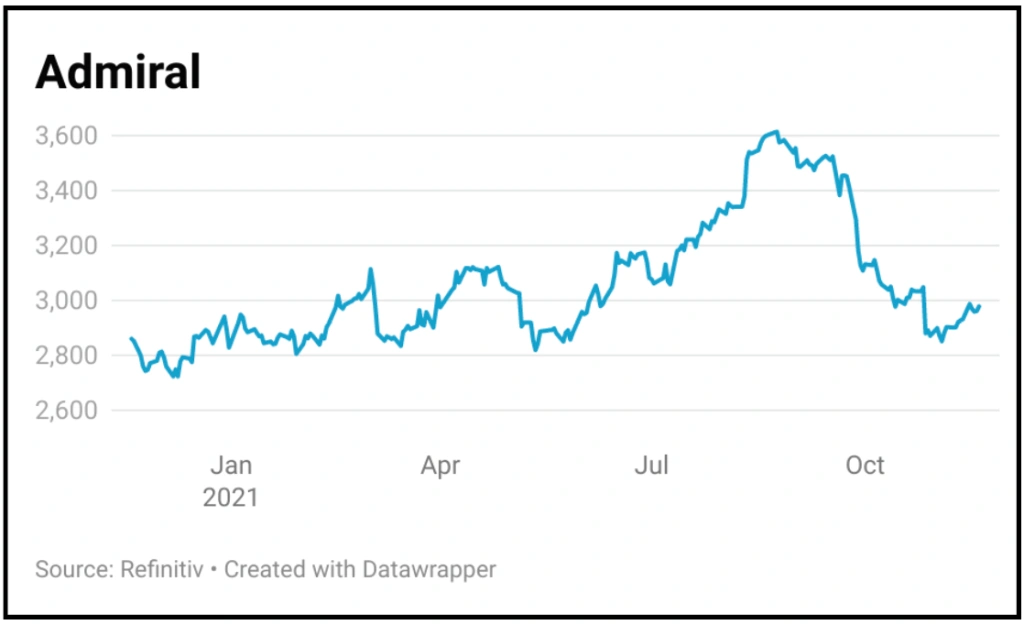

Admiral (ADM) £29.56

2021 yield 9.7%

Cardiff headquartered non-life insurer Admiral (ADM) offers income investors an inflation beating 9.7% yield for 2021, and a prospective 6.6% yield in 2022.

Two factors account for this inflation-busting yield. First, the 63% increase in the first-half dividend is a reflection of a strong uplift in earnings. Second, both the 2021 and 2022 figures are boosted by special dividend payments resulting from the disposal proceeds of its price comparison website Penguin Portals.

First half results to the end of June, reflected the strong underlying health of the business. Profit before tax increased by 76% to £482 million versus the first half 2020 of £274 million. Earnings per share rose by 67% to 132.9p compared to 79.7p in the corresponding period in 2020.

As Berenberg notes: ‘Admiral has a proven track record of outperformance in a very competitive environment. We expect it to continue to use its sophisticated pricing tools to price effectively and maintain underwriting profitability.’

On 30 April Admiral confirmed the sale of its price comparison website Penguin Portals for £460 million. The group is returning £400 million to shareholders, via three special dividend payments.

The 63% uplift in the 2021 interim dividend from 70.5p to 115p was in part due to the first of these special distributions of 27.1p. Two additional special dividend payments will be made with the payment of the final 2021 dividend, and at the 2022 interims. [MGar]

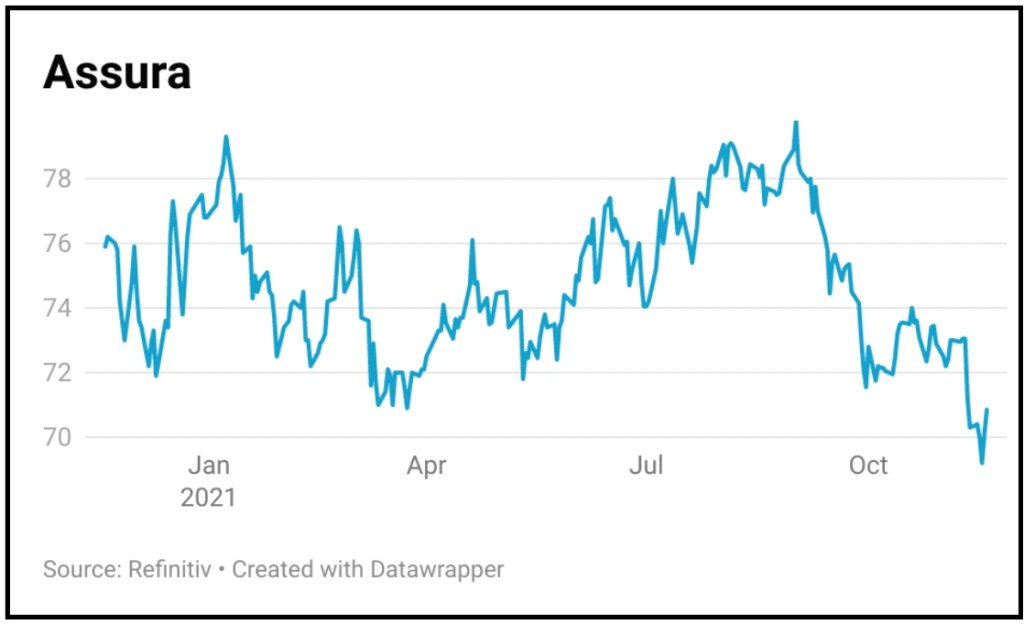

Assura (AGR) 70p

Dividend Yield: 4.2%

Real estate investment trust Assura (AGR) invests in healthcare premises and manages a portfolio of more than 600 GP surgeries, primary care, diagnostic and treatment centres around

the country.

It has a strong relationship with the NHS and delivers a wide range of services from general practice to physiotherapy, renal dialysis and even x-rays, while the pandemic clearly highlighted capacity constraints in hospitals and the need for better community healthcare.

Assura works with GPs and healthcare companies to design and develop new medical centres, tying in its tenants before its third-party construction partners start building.

Thanks to its secure covenants and long leases, which are subject to rent reviews linked to inflation, the company generates a secure and predictable income stream with an attractive and growing dividend.

In the six months to September it invested over £110 million in new and existing sites, and it recently raised £182 million to invest in its pipeline of almost £500 million of opportunities of over the next 18 months.

Analysts at Jefferies believe the firm can grow its dividend by more than the current rate of inflation for several years and rate the shares as attractive given the low-risk income profile and above-inflation dividend yield. [IC]

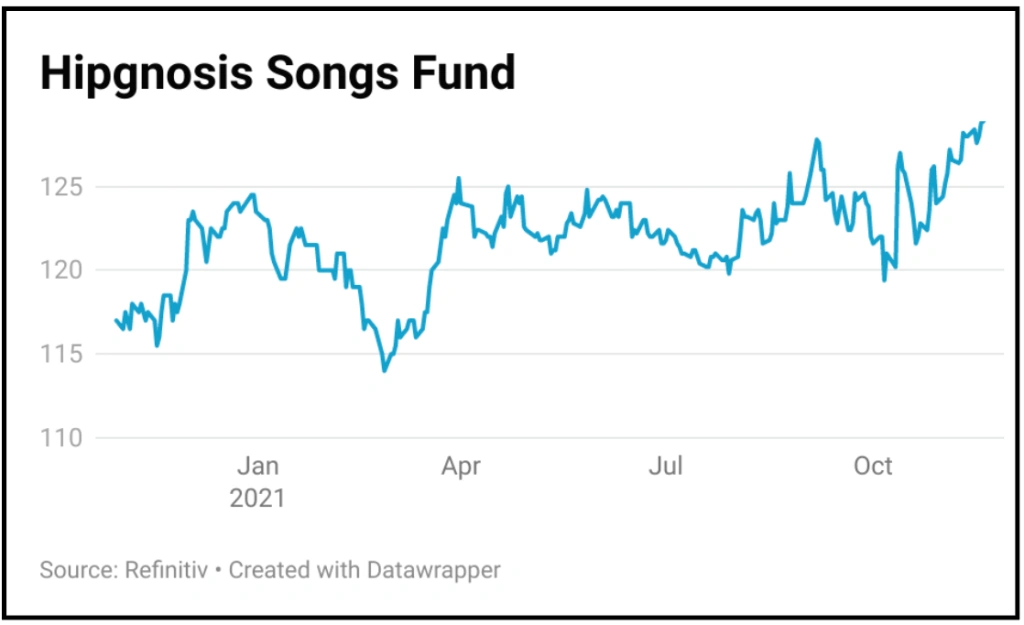

Hipgnosis Songs Fund (SONG) 127.9p

Dividend yield: 4.2%

Investment trust Hipgnosis Songs Fund (SONG) buys up collections of songs from which it can generate royalties, underpinning a growing stream of dividends. It listed in London 2018 and investment in the music royalty space has ramped up in the interim.

As Numis observes: ‘Universal Music paid more than $300 million for the song catalogue of Bob Dylan, and Warner Music just did a deal with Madonna. KKR formed a joint venture with BMG and acquired the catalogue of songwriter Ryan Tedder.’

Music streaming has grown rapidly during the pandemic, with Hipgnosis generating revenue from platforms like Apple Music and Spotify, as well as when songs are played in gyms, shops and restaurants, on stage or on the radio and increasingly when they are played on social media platforms, TV shows and video games too.

Hipgnosis owns the rights to works by the likes of Ed Sheeran, Barry Manilow, Beyonce and Stevie Wonder and it has a good track record of dividend growth since listing. The main drawback is the regular issue of new shares to fund catalogue acquisitions, which dilutes existing shareholders.

Hipgnosis’ investment adviser HSM recently created a joint venture with private equity firm Blackstone which will invest up to $1 billion in acquiring and managing music catalogues. The venture will also include co-investment with the investment trust on royalties. The ongoing charges are not cheap at 1.59%, reflecting the specialist nature of the fund’s remit. [TS]

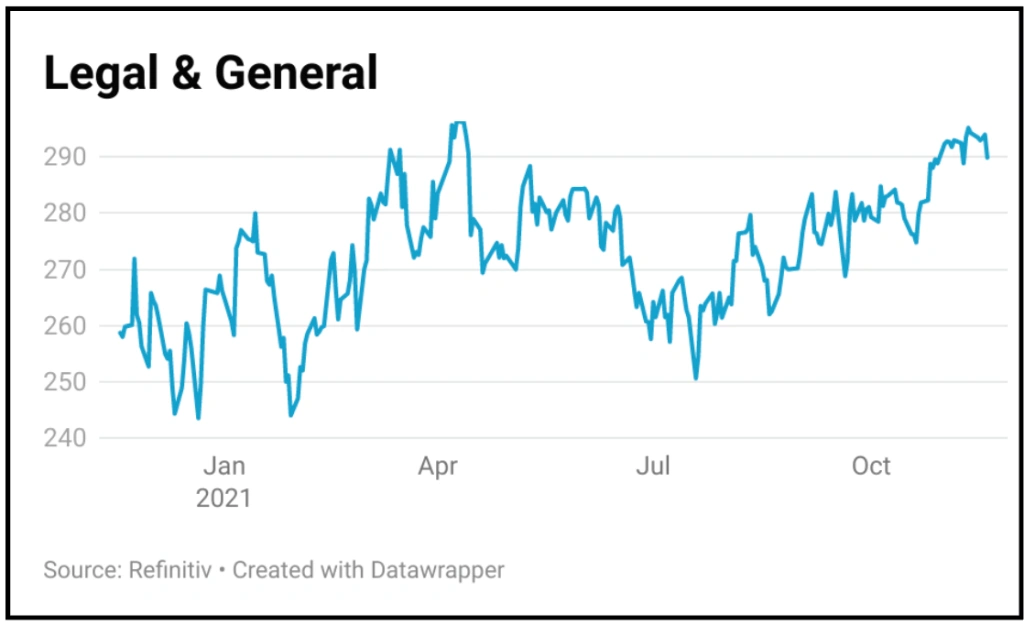

Legal & General

(LGEN) 292.8p – Dividend yield: 6.3%

The dividend performance record of UK life insurance company Legal & General (LGEN) is impressive. This looks set to continue as improving actuarial assumptions (people dying earlier as a result of Covid), coupled with good market returns and timely disposals, should enable the group to increase dividend payouts.

The dividend policy intends to ‘maintain progressive dividends, reflecting the group’s expected medium-term underlying business growth’.

The strength of the underlying business was reflected in the results for the six months to June, where pre-tax profits increased to £1.4 billion versus £342 million for the prior year. The 14% jump in operating profit to £1.1 billion was 8% ahead of market expectations. The company declared an interim dividend of 5.18p per share, an increase of 5% year-on-year.

Legal and General’s dividend track record is particularly impressive when viewed from a longer term perspective. The company has steadily grown the dividend following the lows in the immediate aftermath of the 2008 financial crisis.

Another appealing facet of the Legal & General dividend story is its relatively robust levels of dividend cover. At 1.34 times, the ratio

of earnings to dividends is ahead of many of its peer group. [MGar]

Polar Capital (POLR:AIM) 830p

Dividend Yield: 5%

Boutique fund manager Polar Capital (POLR:AIM) has a prospective dividend yield of 5% which is covered 1.5 times by forecast earnings per share. Over the last decade the company

has delivered a compound annual growth rate in its dividend per share of 18% a year.

We believe the quality of Polar Capital’s business and stable operating margins which has achieved an average return on equity of 35% over last five years provides comfort to investors that the dividend is safe.

And beyond that we think there are sustainable growth drivers supporting the business which should see the dividend grow faster than inflation over the coming years.

The two biggest factors shaping the fund management industry over the last decade have been the growth of low-cost exchange traded funds whose main advantage is scale and the growth of specialist truly active managers like Polar Capital.

Polar is an ‘investment focused’ firm whose goal is to deliver differentiated risk-adjusted returns across a diverse range of fundamentally driven products as well as a high level of customer service.

The company’s operating model and entrepreneurial culture attracts the best talent in the industry and creates a solid platform for future growth. [MGam]

Vistry (VTY) £11.10

Dividend yield: 5.7%

Housebuilder and regeneration play Vistry (VTY) posted first half revenues and earnings ‘significantly’ ahead of management expectations and raised its full year guidance after it was able to more than offset higher input prices with higher selling prices.

Turnover was up 91% on the first half of 2020 and was modestly above the first half of 2019, making Vistry one of the few housebuilders to show progress against pre-pandemic levels.

The firm is already fully sold out for 2021 and is ‘in great shape’ for 2022 according to chief executive Greg Fitzgerald, with higher margins and strong cash generation meaning it expects to end the year with a net cash position of

£225 million.

This positive outlook and the strength of its balance sheet have allowed the firm to accelerate its move to a sustainable two times dividend cover policy, with a promise that any further excess capital generated be handed back to shareholders through special dividends or buybacks.

Having cut its payout last year to preserve capital, the company is expected to pay an ordinary dividend of 63p this year out of earnings per share of 126p and 73p next year out of earnings of 146p, although we wouldn’t be surprised to see forecasts raised again. [IC]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

- DotDigital share slump means you can buy cheaper now

- Growth, profit and M&A to drive CentralNic higher

- Plenty of reasons to remain positive on Euromoney

- The smart way to play a rebound in the Chinese stock market

- All-weather trust Ruffer is selling new shares at a discount

- Investors overreact to Frontier Developments' downgrade