Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy it’s so tricky to run a bank

Is there a harder job in the corporate world than managing one of the UK’s big four banks? Barclays’ (BARC) current head of global markets CS Venkatakrishnan, or Venkat, for short is about to find out – subject to regulatory approval.

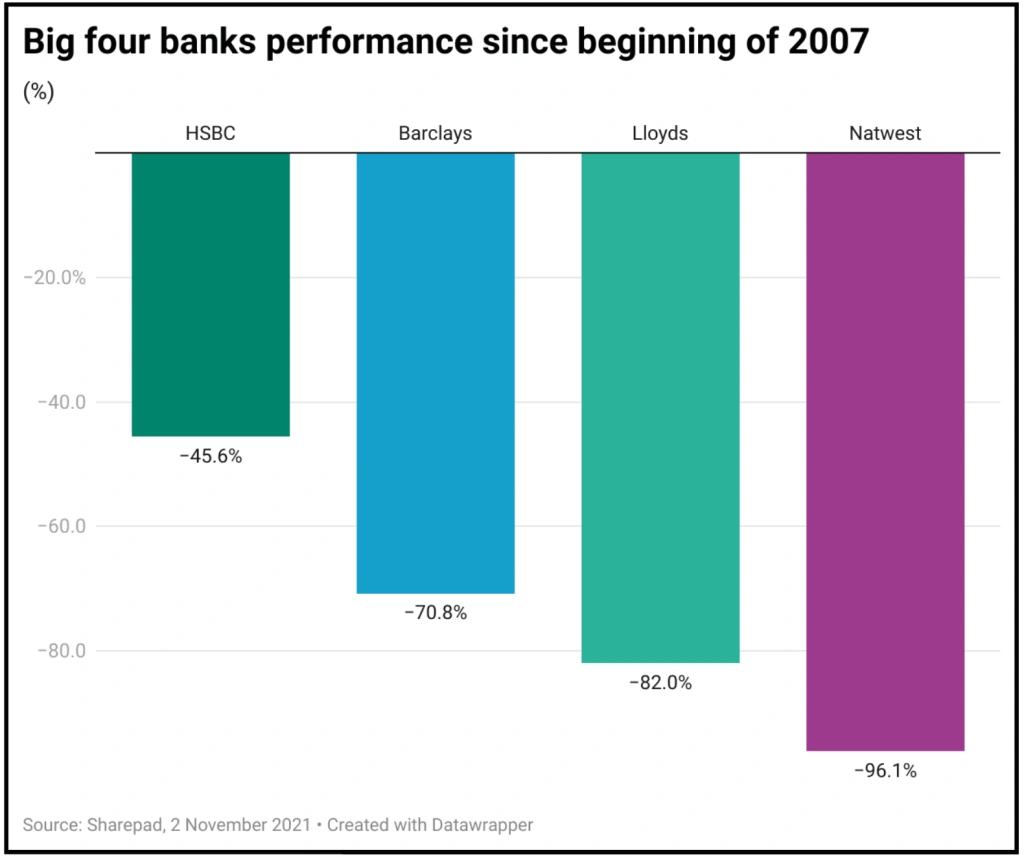

Those last four words sum up the situation the sector has found itself in ever since the financial crisis of 2007/8 – with the relevant authorities minded to keep them on a tight leash. See, for example, their inability to pay dividends during the pandemic in case Covid-19 put a material strain on their balance sheets.

That should not necessarily invite sympathy. The banks invited such a situation on themselves through their behaviour in the run up to the credit crunch which resulted in all of us, as taxpayers, having to come to their rescue.

Notably Lloyds (LLOY) and Natwest (NWG), the two recipients of state bailouts, have performed significantly worse than their counterparts Barclays and HSBC (HSBA) since the beginning of 2007.

While the predicament departing Barclays CEO Jes Staley found himself in, facing a FCA (Financial Conduct Authority) and PRA (Prudential Regulation Authority) probe into links with the disgraced financier Jeffrey Epstein, might have rendered his position untenable at any company, there is no doubt that being at a bank means the glare of publicity and the attention of regulators goes up a notch.

RATE RISE RISKS

In theory the backdrop for the banks looks likely to improve, with management teams able to look forward for the first time in a long time to higher interest rates. The Bank of England may even have raised rates today (4 Nov) but is certainly lining up a rate rise before the end of 2021.

This should enable the sector to increase the amount it charges for lending to businesses and consumers and thereby boost its returns.

However, those in charge at the banks have to balance the temptation to take advantage of this opportunity with several reputational, political and financial risks.

If the banks go too far and too fast with their lending rates, particularly on products like mortgages, the politicians may well exert pressure on the industry as they look to salve the concerns of homeowners already facing a cost of living crisis.

Perhaps even more pertinently, putting too much pressure on customers risks a wave of bad debts which would clearly have very negative implications for their profits and balance sheets. Or, in other words, life just doesn’t get any easier in the boardrooms of Britain’s banks.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.