Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat the bond market is telling investors

The most violent price reaction to last month’s Budget was seen in the usually calmer environment of the bond market.

The yield on the benchmark 10-year government bond, or gilt, plunged in one trading session from 1.11% to 0.985%.

That equated to a 1.3% one-day gain in the paper’s price (since bond yields move inversely to price, just as is the case with shares) as the Budget document itself revealed a big drop in the amount of gilts that the Bank of England intended to sell for fiscal 2021-22, in response to downward revisions to estimates for government borrowing.

But that was the first bit of good news holders of UK government debt had had for a while. As inflation has picked up pace, so bond yields have surged and prices tumbled. From its year low of 0.18% on 4 January, the benchmark ten-year gilt yield rose to a peak of 1.20% on 21 October.

That equated to an 8% drop in the price of the paper – so anyone who bought at the yield low (and price peak) lost the equivalent of 44.4 years’ worth of interest.

Safety first

This raises the issue of whether government bonds are ‘safe’ or not. The idea is that they are. The investor buys the bond at issue, receives the interest payments (or coupons) over the lifetime of the bond and then gets back their initial investment (or principal) upon maturity of the loan.

However, there are risks:

– Credit, issuer, or default risk. Western government defaults are rare (because they can just print more money to foot the bill) and such paper is therefore used as a benchmark, ‘risk-free’ rate. Any other bonds – corporate, emerging market and so on – of similar duration should offer a premium return to compensate the holder for the greater risk that the borrower gets into trouble and cannot make the interest payments or return principal.

– Inflation risk. If the rate of inflation exceeds the coupon or yield on the bond, then the investor is effectively locking in a guaranteed real-terms loss.

– Interest rate or market risk. If inflation becomes entrenched and interest rates rise then a further risk comes into play since bond prices could fall as holders sell existing positions to buy new positions in new issuance, which will have to come with higher coupons to compensate for advances in headline borrowing costs. Price declines could erase a chunk of the income accrued.

– Liquidity risk. It is important to make sure the bond's issue size will be large enough so it can be easily bought and sold in the secondary market. The less liquid the paper, the higher the coupon should be to compensate the holder.

The coupon is always fixed and is based upon the issue price of the paper (usually 100). The yield will change according to the price, just as it would for a share.

As coupons get lower, or yields become thinner, the buffer against any potential capital loss in the event interest rates rise gets progressively smaller. This is where duration comes into play.

Macaulay duration measures the average weighted time to maturity of all coupon and principal payments.

Modified duration quantifies interest rate risk and how much a bond or portfolio of bonds will move in price relative to a 1% shift in borrowing costs.

Note how that one percentage point rise in the UK 10-year gilt yield between January and October translated into an 8% price decline.

Risk and reward

The issue therefore is not whether government bonds are risky or not, but whether the rewards on offer, in the form of the coupon or the running yield, compensate the holder for the risks involved.

In inflation becomes entrenched and stays elevated, the answer may well be ‘no’. If an investor believes the storm will blow over and deflationary forces will reassert themselves, then the answer may be ‘yes,’ especially after the recent sell-off.

Investors can also build a portfolio of bonds to help manage the risks:

Longer-dated bonds have longer durations, as the returns are more back-end loaded, so they will be more volatile, or sensitive to interest rate movements. Perpetual bonds, with no maturity date, are the most volatile bonds of all.

Lower-coupon bonds also have longer durations, and therefore be more volatile, as again the returns are more back-end loaded. Zero-coupon bonds have a duration that is the same as their maturity.

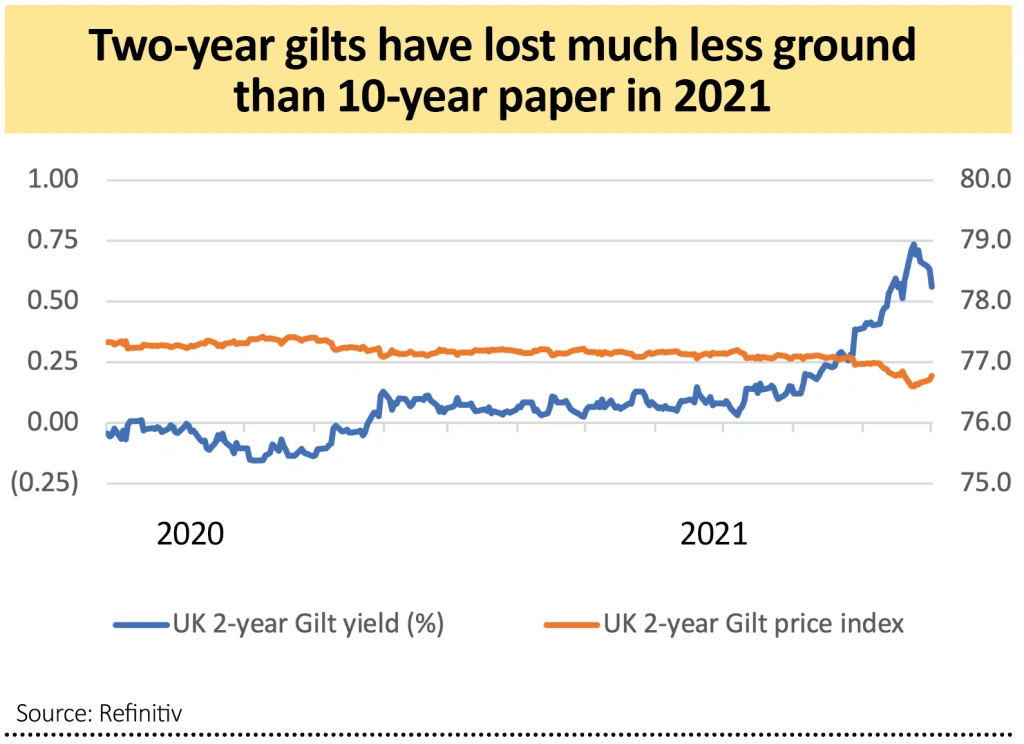

The opposite also applies: the shorter the life of the bond, or the higher the yield, the shorter the duration and the less the degree to which prices will move relative to interest rate changes. The UK two-year gilt lost just 1% in price while the 10-year lost 8% in that January-to-October market swoon.

Investors can also use bond funds to mitigate the dangers. They can own a range of them or pick a flexible bond funds that can put money to work across a wide range of fixed-income asset classes and not just one and therefore use its mandate to to tackle – and even benefit from – duration.

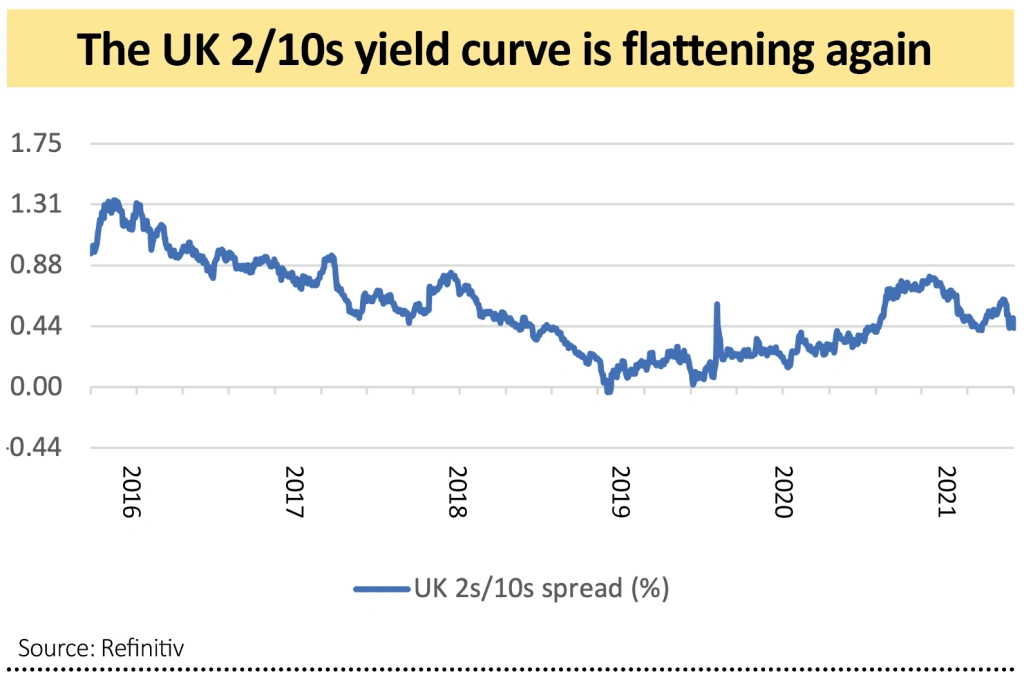

Mind the spread

One tool that investors can use to measure whether inflation or deflation is coming, is the spread between the two and 10-year gilt. If the market thinks a recovery and inflation is coming (and that central banks will actually raise interest rates), the spread may widen, and the yield curve steepen as rate rises are priced in. If it thinks a downturn or deflation are coming, then it may flatten as rate cuts are priced in.

Right now, the yield curve is flattening, even as inflation rises. Central bank manipulation of bond markets via quantitative easing could mean we are getting a false signal. But it could mean the gilt market is warning of the middle ground, the worst outcome of all – stagflation.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.