Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWater: the investment theme which is bubbling up nicely

The argument for investing in the water sector is simple. Water is critical for both human life and commercial activity. Economic and business growth is contingent upon a steady stream of clean water.

For these reasons water has been talked about as potentially the next big thing in terms of global investment trends for at least a decade.

However a combination of the growing prominence of investing with an ESG (environmental, governance, social) bias and a mounting awareness of the specific challenges associated with ensuring the world has sufficient clean water has helped move water firmly into the mainstream in the last 12 months and this has been reflected in the performance of assets in this space.

HOW TO INVEST

There are two main options for UK investors’ interested in gaining exposure to this theme. First, invest in one of three dedicated water funds.

Second, select a specialist water ETF (exchange-traded fund). There are two ETF’s with established track records, and a third relatively new entrant to the sector that has adopted a slightly different approach to its charges, in an attempt to outperform its rivals and scale its assets under management.

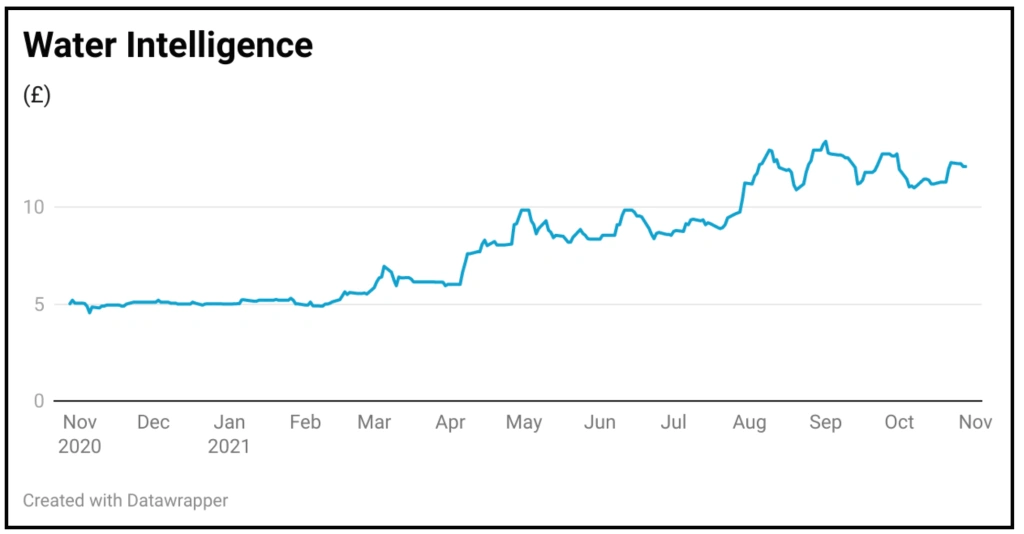

Small cap Water Intelligence (WATR:AIM) has enjoyed a stellar year with its shares more than doubling in the last 12 months to £12.

The business uses its technology to identify and fix water leaks and recently reported a 42% rise in pre-tax profit for the first nine months of 2021 to $5.9 million. However, for most investors diversified exposure to water is probably a more sensible approach.

WHY WATER MATTERS

Several factors have exacerbated the long-term scarcity of water supplies.

These include climate change, population growth, demographic shifts and increasing industrialisation. Large-scale investments are needed in both emerging and developed markets in order to improve efficient water use, increase water supplies, ensure water quality and mitigate scarcity within the agriculture sector.

Water is an essential component for biological, environmental, social and economic growth. Nonetheless, during the last century imprudent global water consumption has threatened water supplies and resulted in a water crisis.

This acute shortage is likely to become more pronounced given demographic shifts coupled with the impact of industrialisation.

Limited supply, coupled with ever increasing consumption and rising levels of pollution, highlight the need for more sustainable and long-term solutions. These will differ depending upon local market traits, like urban trends, existing infrastructure and topography.

WHICH SECTORS HAVE EXPOSURE?

From a practical perspective the utilities sector is a natural destination for investors seeking exposure to the water sector. These companies focus on the provision of water and wastewater to residential, commercial, and industrial sectors.

They operate large and small-scale water and wastewater networks as well as special use water facilities such as desalination plants near oceans and advanced filtration plants in urban areas. They generate revenue through customer fees as well as through the recovery of nutrients and energy from wastewater.

Investing in water infrastructure provides stable and enduring returns. Increasing demand in urban areas throughout the world, suggests that investments in utilities will continue to be a steady source of income in forthcoming decades.

In developed countries, utilities are investing in renewing existing infrastructure, and increasingly in green infrastructure (a network that provides the ingredients for solving urban and climactic challenges by building with nature).

Engineering and construction is another key beneficiary of the need to ensure a safe and reliable supply of water. In developed countries, investment is focused on replacing aging distribution networks. In major urban centres pipes and mains are outdated and in need of replacement.

The value of water lost before it reaches the customer, (losses due to main breaks and leaks), totaled $39 billion per year globally.

The United Nations sustainable development goal seeks to ensure availability and sustainable management of water and sanitation for all by 2030.

According to a research paper entitled Estimating the Value of Public Water written by Martin Doyle at Duke University to meet this target annual water investments must triple in the next decade to around $114 billon a year.

A key driver of growth is the upgrade and expansion of distribution networks to consumers in residential communities and commercial buildings. From plumbing, pipes, toilets and faucets to heating and cooling systems.

However green infrastructure is gaining importance. For example ‘smart’ urban planning policies can help reduce flood risks by providing spaces to collect and store floodwater within the built environment. The same flood run off can be used to recharge municipal groundwater reservoirs.

SPECIALIST WATER FUNDS

There are currently three dedicated water funds available to investors. These include RobecoSAM Sustainable Water Equities (BMF7CR0), Pictet Water (B516BZ3), and Fidelity Sustainable Water and Waste (BHR44F6).

From a performance perspective the RobecoSAM fund has the best track record, with a three-year annualised return of 21.3%. This compares with a comparable figure of 19.4% for Pictet’s Water fund.

The Fidelity Sustainable Water and Waste fund has a shorter track record than the other two funds. In 2020, the fund returned 7.1%, underperforming the benchmark that recorded a 13% return, and year to date returns indicate a similar pattern with the fund returning 18.3% versus a benchmark return of 24.8%.

This divergence in the performance of these funds is predominantly a consequence of their relative sector weightings. Robeco’s fund has a 43% weighting in industrials, a 15.3% weighting in in healthcare, 15.2% in utilities and 14.4% in the basic materials sector.

The consumer cyclical sector has the lowest weighting in the fund at 7.9%. Both the Fidelity and the Pictet fund have significantly greater weightings to the industrials sector at 50.7% and 54.4% respectively.

Another notable point of differentiation is Robeco fund’s larger exposure to the basic materials sector, at 14.4% compared to both the Fidelity and Pictet funds at 0.93% and 4% respectively.

With respect to the healthcare sector both the Robeco and Pictet offerings have substantial investments at 15.3% and 13.7%, this in marked contrast to Fidelity’s fund which has no healthcare exposure, but does have a 13.1% weighting in technology. The other two funds have no technology investments.

FACTORING IN COST

From a cost perspective the Pictet Water fund has the highest charges, it has an ongoing cost fee of 1.1% and an annual management charge of 1.2%. The comparable figures for the Fidelity and Robeco funds are 0.95% and 0.75%, and 0.96% and 0.85%

There are three different water ETF’s providing exposure to the sector. These are Lyxor World Water (WATL), iShares Global Water (IH20), and L&G Clean Water (GLGG). On a three year annualized basis the iShares ETF has the strongest performance, but only marginally, at 20.8%.

The Lyxor ETF almost mirrors this performance at 20.6%. The L&G ETF was formed in June 2019, so there is a paucity of comparable performance data. In 2020 the fund outperformed the benchmark by a significant margin, with a return of 19.3% against 13% for the benchmark.

All three ETF’s follow different indices, which helps to explain the difference in performance. The L&G ETF tracks the Solactive Clean Water Index. This comprises a basket of sixty-six companies involved in the provision of technological, digital, engineering and other water services.

Consequently it has more of a technology driven growth tilt than the other ETF’s. This accounts for its year to date return of 20.8% which is marginally ahead of the Lyxor ETF (20.5%), but lags the iShares ETF (23.5%).

As with the aforementioned specialist water funds, another factor influencing the divergent performance of these ETFs is their relative sector weightings. Lyxor fund has a greater weighting to the industrials sector (71%), compared to L&G (56%) and iShares (57%).

The iShares ETF also has a noticeably higher exposure to utilities sector (39.5%) than both the L&G ETF (26.2%), and the Lyxor ETF (25.9%).

The ongoing charges are almost identical for both the Lyxor and iShares ETF, at 0.6% and 0.65% respectively. As a relatively new entrant to the sector and with only $317 million of assets under management, the L&G team have strategically priced their offering at a discount, with a total expense ratio of 0.49%.

If we compare the returns (three-year annualised) for the best performing water fund (Robeco) versus the equivalent ETF, (iShares), the Robeco fund comes out ahead by a whisker, at 21.3%, versus a figure of 20.8% for the iShares ETF. However after accounting for fees, the return for the Robeco product comes in just behind the ETF.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.