Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSay yes to Scottish Investment Trust merger with JPMorgan

After more than 130 years, the board of the once-pioneering Scottish Investment Trust (SCIN) has decided it is to be subsumed into a rival global trust and will cease to be. The trust has suffered in recent years from poor performance and the board of directors has rightfully called for change.

Shares takes the view that shareholders should vote in favour of the merger with JPMorgan Global Growth & Income (JGGI) as this is a decent investment trust and one which could deliver superior returns.

The caveat is that the investment approach is slightly different. Scottish Investment Trust was a pure ‘value’ play, investing in unloved companies but whose merits it believed would eventually be recognised by the market. JPMorgan’s trust has a broader approach, building a portfolio of best ideas whether that’s value or growth in style.

THE TRUST’S HISTORY

Incorporated in Edinburgh in 1887, Scottish Investment Trust originally invested heavily in the Americas, at that time still a developing market.

As a result, it owned stakes in railroads in the US, Latin America and Cuba, as well as an Argentinian bank, a Brazilian telegraph company, Costa Rican bonds and a Uruguayan chemical company.

There were also investments in ‘the colonies’, such as companies managing rubber and tea plantations. Some of its early investments are still well known today, including HSBC (HSBA), P&O – now owned by Carnival (CCL) – Rio Tinto (RIO) and Standard Life, now part of Abrdn (ABDN).

The company’s first board members believed investment at home ‘seldom matched the prospects for economic expansion which existed overseas’, and by the turn of the 20th century, the Scottish Investment Trust had most of its investment overseas.

Except during the Second World War, when the Treasury requisitioned almost all overseas investments to help pay for the war effort, and its immediate aftermath, this remained the position. The company’s principal aim was to invest in ‘well-managed companies which were likely to achieve a good increase in earnings and dividends’.

CHANGING OF THE GUARD

In 2015, following the ousting of the former chief investment officer, the remaining managers abandoned the previous growth and income strategy and embarked on a ‘high conviction, global contrarian’ investment approach.

The board took the view that a period of at least five years was necessary to evaluate the company’s returns under this new mandate.

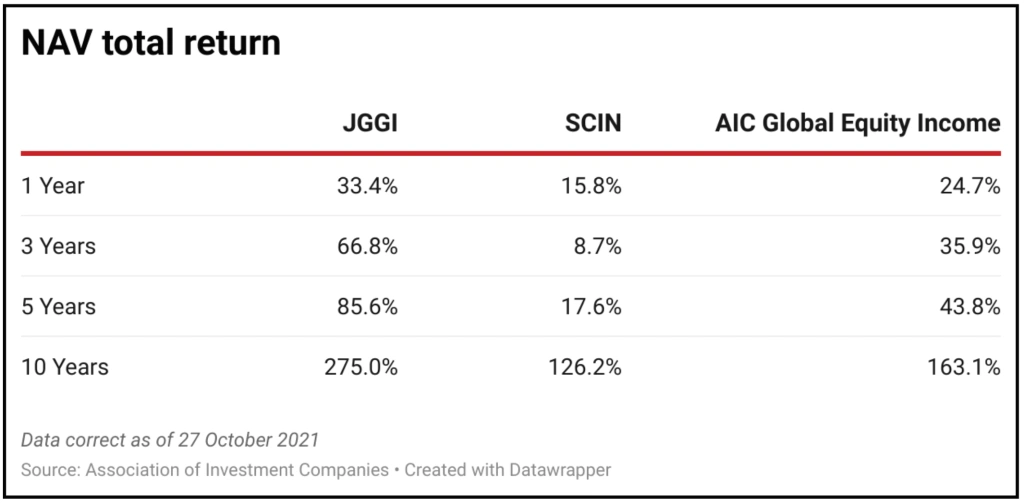

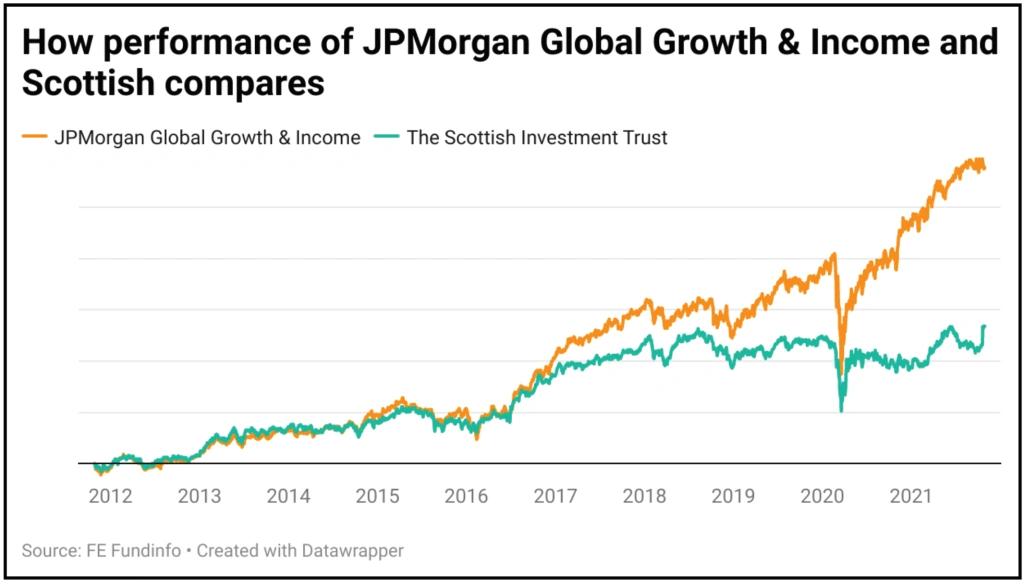

While it doesn’t have a formal benchmark, the company’s net asset value total return over the five years to the end of this April consistently underperformed the MSCI All Country World Index and the Association of Investment Companies’ Global sector index.

As a result, in early June 2021 the board appointed consultants to help it review the company’s investment management arrangements, inviting proposals from rival fund management groups.

The board especially wanted to hear from firms ‘with the experience of managing listed closed-ended funds, designed to deliver, over the longer term, above-index returns through a diversified global portfolio of attractively valued companies with good earnings prospects and sustainable dividend growth’.

END OF AN ERA

The board has now concluded ‘the most compelling outcome for shareholders’ would be to combine Scottish Investment Trust JPMorgan Global Growth & Income to form an enlarged investment trust with net assets in excess of £1.2 billion and a single, focused mandate. Essentially it would see JPMorgan in charge and the Scottish Investment Trust name disappear.

Assuming shareholders vote in favour of the deal, the JPMorgan management team will comprise Helge Skibeli, Rajesh Tanna and Tim Woodhouse, supported 80 in-house analysts located globally.

Among the attractions of merging with the JPMorgan trust are its strong NAV total return over the last five years (14% per year or 1.7% ahead of the MSCI ACWI in sterling), the depth of in-house resources JPMorgan brings, and its generous distribution policy which targets dividends of at least 4% of NAV at the end of the preceding year.

The enlarged investment trust would benefit from economies of scale and come with an average annual management charge set at 0.49% of assets and an ongoing charge of 0.57% for the next 12 months.

WHAT HAPPENS NEXT?

General meetings of both trusts will be convened to approve the change of manager and merger, with the new managers expected to be in place by mid-January next year and the transaction expected to complete during the first quarter. The dates for the shareholder votes have yet to be published.

Assuming a deal is approved, shareholders in Scottish Investment Trust will receive new shares in JPMorgan Global Growth & Income on a formula asset value basis, comparing the net asset values of each company adjusted for costs and declared but unpaid dividends.

In the case of Scottish Investment Trust, the formula will exclude the company’s offices at 6 Albyn Place in Edinburgh, its home since 1889, the pension scheme and its wholly owned subsidiary SIT savings. These will remain with the liquidator along with sufficient assets to meet the trust’s liabilities.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.