Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMarket impact of company updates more obvious than economic data

You don’t need a degree in finance to understand that both company earnings reports and major economic indicators and events both influence the investing landscape.

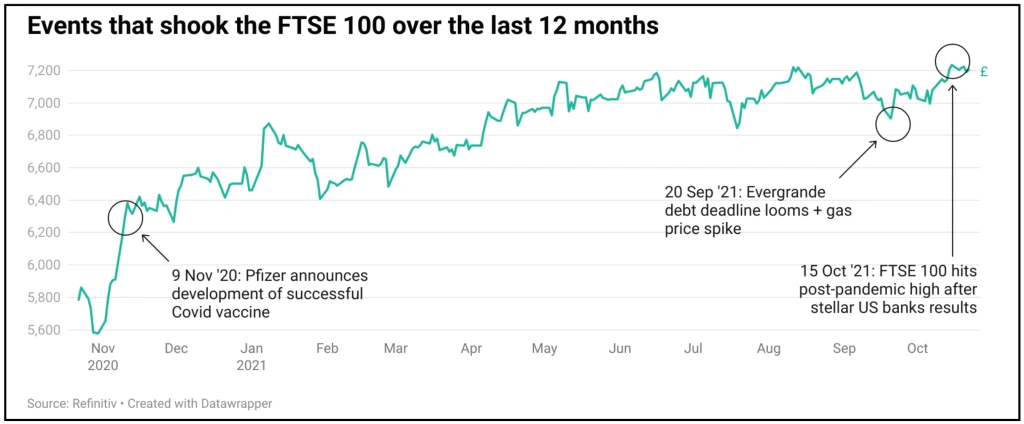

However, looking at how London markets have performed over the last, complicated, 12 months it’s interesting to dig into those peaks and troughs and explore trends. Just weeks ago, at the start of the latest round of company earnings, the FTSE 100 surged to a pandemic high despite ongoing concerns about supply snarl ups and rising prices.

US banks in particular exceeded expectations, but it wasn’t just banks and it wasn’t just US companies reporting forecast busting figures. It’s not surprising that stellar results whet investor appetites.

They’re straightforward and immediate. If profits and earnings are up there’s an instant catalyst to buy and vice versa when the numbers disappoint.

The X-factor is surprise. Investors are pretty good at picking up cues and pricing them in, so often its more about how a company does relative to expectations rather than how it makes out in absolute terms. Sometimes just meeting expectations will disappoint investors.

Updates from individual firms may have a significant impact on their own share price but a limited one on the wider market in isolation. However, in combination a results season can set the tone for the markets.

MARKETS DON’T LIKE SURPRISES

Economic data typically acts more like a drip, drip of incremental news which gradually shifts investor sentiment in different directions. Often individual releases like GDP figures don’t tend to make big ripples unless there’s a major upset.

For example, China’s latest growth numbers unsettled many people but that’s because any slowdown seems unusual, and they came off the back of events which have already impacted sentiment towards China, from the tech crackdown in May to the Evergrande debacle which came to a head in September.

Both of those events in singularity took time to permeate through to big market movements, primarily because it was hard to know immediately what the situations might mean, it can take days or even weeks for the ramifications to really permeate. It buys investors time, gives them breathing space to make adjustments in their portfolios and get comfortable with the winds of change.

It’s why the anticipated interest rate hike from the Bank of England which has received so many column inches has seemingly had a modest influence on markets so far.

Even when it comes it’s unlikely to merit much of a move, unless the MPC (Monetary Policy Committee) go bonkers and shoot for a whole 1% all in one go, but that’s about as likely as the UK experiencing a white Christmas in June.

The more UK-facing FTSE 250 index has endured a year of uncertainty. Covid hasn’t run in a smooth line, lockdowns have had to be re-implemented, ‘Freedom Days’ have had to be shifted and sometimes the expected benefits are undone by crises like the ‘pingdemic’ which saw many businesses scrabbling to find the staff they needed just to keep operations going.

When the economy has enjoyed a smooth run, when the recovery juggernaut ploughed through, the FTSE 250 soared; its domestic companies expected to benefit from a return to something like business as usual.

RISING PRICES NOT THE ONLY TROUBLE AHEAD

Gas prices on the other hand, they nestle between the two extremes. On the one hand rising prices and the impact they were having on energy providers could be clearly seen for some time. The energy cap was going up, small providers were dropping like flies.

But this impact was crystallised in a single day, a day of extremes, that made waves. After a 37% jump in 24 hours the gas price cooled as the Russian president stepped forward and seemed to imply more supply would be forthcoming to Europe.

Forget the next 12 months, the next six months is shaping up to bring more of those heart stopping, unexpected moments that markets hate to love and many more of those priced in economic set pieces.

And the next quarterly results, the judgement is still out on that one… even among companies which have beaten analysts’ estimates, there have been warnings that margins are set to be eroded, that supply issues and inflation will take their toll. Investors love certainty, but in the unexpected there are opportunities as well as potholes.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.