Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLessons one year on from the low

It was Warren Buffett’s mentor, Benjamin Graham, who once wrote: ‘The intelligent investor is a realist who sells to optimists and buys from pessimists.’ Such plain-speaking, common sense has yet again proved its worth over the past 12 months to offer a timely lesson to us all.

It is almost a year to the day (23 March 2020) since the FTSE 100 bottomed at 4,994 amid widespread fear over what the pandemic could do to global growth and corporate profits.

A year later and the picture is very different. Anyone brave enough to have started to take on more risk a year ago would have done remarkably well, as four data sets show. Investors now must decide whether these trends will continue, further changes in performance trends since ‘Pfizer Monday’ on 9 November will dictate or that a further shift in gear is imminent.

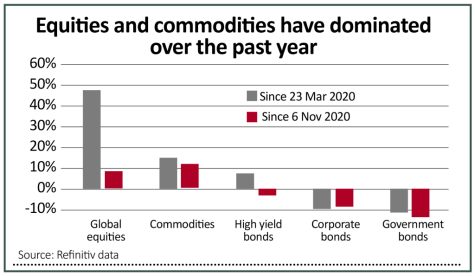

GLOBAL ASSET CLASSES

Fear may have dominated a year ago, but equities have been the best place to be over the past 12 months. As benchmarked by the MSCI All World index, global stocks have beaten commodities and bonds. Government bonds, in theory a port in a storm, have provided no shelter with capital losses more than offsetting any yield that they offered.

There have been subtle changes since November. Commodities have taken the lead from equities and high yield bonds have started to flag. Meanwhile, the rout still seems to be on when it comes to investment-grade corporate and government bonds.

STOCK MARKETS

Unlike bonds, where all major categories have fallen on a one-year view, all geographic equities options have gained. Asia and Japan have performed consistently well, perhaps thanks to the relatively low number of pandemic cases they have suffered and their rapid, robust approach to test, track and trace as well as containment.

America’s domination of early 2020 has faded and it is prior laggards who have come to the fore – emerging markets and even the unloved UK equity market has put on a spurt, finding itself outpaced by just Eastern Europe and the Africa/Middle East region since November. This may be down to the perception that the UK is ahead of the game when it comes to vaccination programmes, having previously struggled to contain the virus.

EQUITY SECTORS

Technology continues to grab the headlines, especially as a raft of new initial public offerings tempts investors’ wallets. But miners, industrials and consumer discretionary stocks have all beaten tech over the past 12 months and oil has been the best performer of the lot, to reaffirm the adage that the darkest hour is before the dawn.

Meanwhile, sectors that looked reliable going into a pandemic – utilities, consumer staples and even healthcare – have lagged, a trend that has become ever-more noticeable since the Pfizer-BioNTech announcement of last autumn.

UK STOCKS

These ‘big picture’ trends – a switch from defensives to turnaround plays, from ‘growth’ (and promises of long-term secular growth, or ‘jam tomorrow’, almost regardless of the economic backdrop) to ‘value’ (cyclicals that offer growth now, or ‘jam today,’ in the event of a recovery), from pandemic winners to bounce-back candidates can be seen on a bottom-up basis in how individual UK-quoted stocks have performed

That said, it has been hard to lose money since last year’s panic. Just nine of the FTSE 350’s current membership have lost ground over the last 12 months.

These trends have become even stronger since Pfizer Monday. Beneficiaries of an economic reopening dominate the leaderboard, notably travel and leisure stocks. The laggards include online delivery plays, precious metal miners, pharmaceutical plays and previously dependable names where investors may have paid too high a valuation, and thus mistaken reliability of earnings for safety of share price. Pay the wrong valuation and nothing is safe.

CONCLUSION

No-one will time a market bottom or top perfectly and trying is a mug’s game. But the trends of the past year show how investors can calibrate risk and earn rewards over time by going against the crowd, focusing on valuation and not getting carried away.

The best approach now could be to heed the words of another investment legend, Sir John Templeton: ‘Bull markets are born on pessimism, grow on scepticism, mature on optimism and die on euphoria.’ It is perhaps time to once more research those areas of which investors are frightened and tread carefully where fear of missing out predominates.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

- Now is a good time to take a stake in Tesla

- Hacking attacks could see surge in cyber insurance claims

- Trying to double your money using a £50,000 inheritance

- Vodafone-backed Vantage Towers: it’s all about the income

- Three IPOs to buy and the names coming soon

- Why supermarkets won’t be shaking over Amazon Fresh

- How to get involved in IPOs

- 3 stocks to play the exciting hydrogen theme