Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe bumper returns Gym Group could generate

After more than 12 months and nearly 50 separate entries our education series aimed at giving new investors a comprehensive introduction to the markets is nearing its conclusion.

We have gradually increased the complexity as we have moved through the series and this week we complete the analysis of The Gym Group (GYM:AIM) by examining its balance sheet, looking at who owns the company, discussing analyst earnings estimates and potential shareholder returns.

Next week we will have a recap of and links to the whole series in its entirety so you can find exactly what you are looking for.

First though we turn back to Gym, a business we believe could be an excellent investment for the long term. You can find part one of the analysis here.

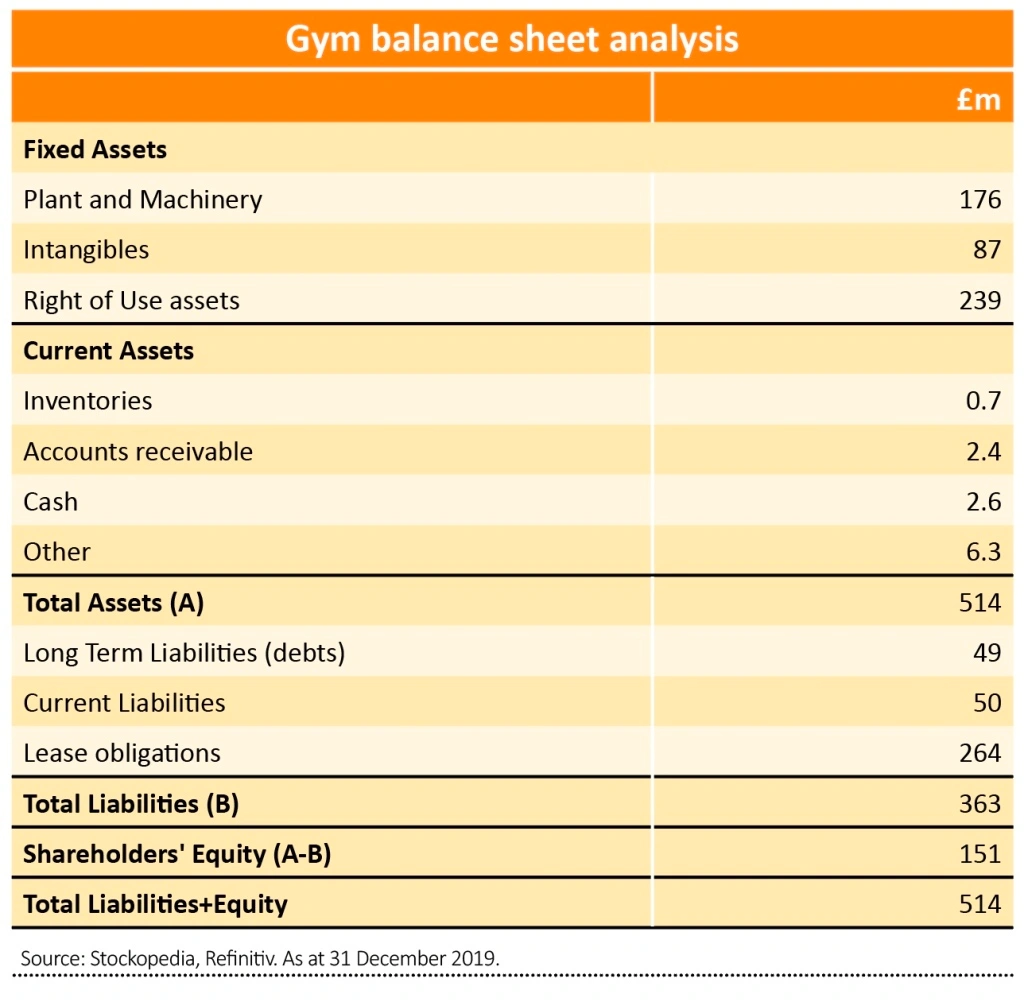

IS GYM SENSIBLY FINANCED?

The company has £49 million of long-term interest-bearing debt which compares with equity which is roughly three-times as big at £151 million, resulting in a gearing ratio of 32%. This is comfortable and not worrying from a solvency point of view.

The accounts have been prepared under the new IFRS-16 lease accounting rules. This means that a new asset (right-of-use) and liability (lease liabilities) have been created to reflect rental leases. This effectively increased total assets by £239 million to £514 million.

Taking a conservative approach to the balance sheet, we adjust debt to include lease obligations. This increases the debt to assets ratio to 61%, still not particularly concerning.

Another way of examining financial strength is to look at interest cover. In 2019 operating profit was £21.5 million which covered annual interest payments of £2.2 million by a comfortable 9.8 times.

The net debt to EBITDA (earnings before interest, taxes, depreciation and amortisation), ratio fell below one to 0.98 times in 2020, before the pandemic, representing low leverage.

In summary, Gym appears to be sensibly financed and up until the pandemic was close to the point of self-financing its growth.

At the pre-close trading update (15 January) the company said it had significant liquidity under a £100 million banking facility. While gyms are closed the group is burning though £5 million a month.

This means that under current government plans to allow gyms to open from the 12 April, Gym is more than adequately positioned to continue its growth strategy.

WHO OWNS IT?

We include a section on ownership because it can reveal what type of investor is attracted to a business. Having long-term backers is important because they provide stability and if needed, inject fresh capital.

Gym is owned by shareholders with a long-term investment horizon who appear to support the management’s strategy.

Liontrust is the largest shareholder, representing 9.3% of the shares, Legal and General own 7.4% and Janus Henderson owns around 5%. The top 10 institutional shareholders own approximately 61% of Gym.

Directors own just over 3% of the company’s shares in aggregate, although the lion’s share of this is founder John Treharne who represents around 2.5% of this with chief executive Richard Darwin owning 0.7%.

It’s always worth checking if senior management have a stake in the business they run, showing they have aligned their interests with shareholders.

ANALYST ESTIMATES

It is worth keeping abreast of analysts’ earnings forecasts where you can. Numis and Peel Hunt are joint-lead brokers appointed by the company. While you might not necessarily be able to get hold of investment research from stockbrokers directly, you can get snippets in media articles about stocks and data on consensus forecasts for free from websites such as Shares own site as well as Sharecast and Reuters.

There are six broker estimates. The company reported 2020 revenue down 47% to £80.5 million in a trading update (15 January), and will provide its preliminary results on 15 March when investors find out how much the company lost last year due to the closure of gyms.

We know that 2021 will result in at least four months of lost trading and perhaps more depending how quickly clients return.

That means that 2022 will probably be the first full year of trading since the last one in 2019. It isn’t clear why analysts think 2022 profits will be below 2019, but let’s assume it reflects an overly conservative assumption about how quickly gyms will get back to normal.

It is tempting to get lost in the minutiae when considering specific forecasts, but as we have mentioned before it’s best to step back and consider what the business might look like in the next few years. Better to be roughly right than precisely wrong.

In the three years prior to 2020 Gym grew revenues at a compound annual growth rate (CAGR) of 27% a year and operating cash flow at 18% a year. We will assume the group continues to open between 18 and 20 new sites a year.

This represents growth of 10% from the starting base of 184 gyms (19/184) with each successive year’s growth slowing by 1% a year as the base estate gets larger. To be conservative we ignore any price effects despite Gym successfully increasing revenue per customer through initiatives like multi-site access in the past.

We also are assuming that the profitability of mature sites remains in the same ballpark as the historical return on capital of 30%.

This line of reasoning leads us to a CAGR of 9% a year over the next five years. We are also assuming no acquisitions which would add sites to the estate. In summary it looks like Gym can grow revenue and profit faster than the market.

THE SOURCE OF SHAREHOLDER RETURNS

In Gym’s case all potential shareholder returns are going to be derived from capital gains as the shares track an increase in profit because the company doesn’t pay dividends.

However, how can we be sure that the share rating is reasonable and reduce the risk of a future de-rating?

The historical price-to-earnings ratio isn’t much help because of the wide range it has traded over the last few years, from 11 times to over 50 times. In part, this reflects the nature of fast-growing businesses which investors find difficult to value.

We can’t use the forecast PE because it doesn’t reflect the business operating fully open.

OWNER EARNINGS

An alternative measure of value is the concept of owner earnings which is popular with value managers and originated by Berkshire Hathaway chairman and famed investor Warren Buffett.

Owner earnings represent profit attributable to shareholders before any capital allocation decision is made to pay out dividends or reinvest in the business.

Because Gym has been heavily reinvesting cash back into the business, net profit includes all the depreciation associated with growth spending. It needs to be adjusted to reflect ‘steady state’ profit.

The method is to start with the net profit line and add back depreciation and amortisation. We then take off maintenance capital expenditures and working capital that are needed to keep the business in business.

The result is owner earnings which are divided by the market capitalisation to provide a yield. The higher the yield the more attractive the investment.

We know from the accounts that Gym’s 2019 adjusted EBITDA was £48.5 million and operating cash flow was £40.8 million. The company explicitly states that the difference between the two numbers is maintenance expenditures. (£7.7 million).

Gym has an attractive owner earnings yield of 9.7%. Imagine for a second that you could purchase the whole company for the current £420 million market cap.

If as the owner, you decided not to grow the business but just run it for cash, within 10 years you would recoup your initial investment and in another 10 years you would double your money.

In other words, the current valuation of Gym implies no growth which looks too conservative.

SHARES SAYS: While Gym faces big challenges in the near term our analysis suggests it is worth buying for the long term at 254p.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Buy Dotdigital, among the UK’s few, true software growth businesses

- Panoply seeds growth opportunity with biggest ever acquisition

- Buy Lindsell Train UK Equity for strong short and long-term returns

- Supermarket Income REIT appeals as a steady investment purely for dividends

- Eurofins beats forecasts and raises guidance again