Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFunds, investment trusts and ETFs that pay dividends every month

Having worked hard for decades and squirrelled away money for later life, once in retirement individuals need to find a way of generating an income to replace the money that used to come from pay packets.

The state pension is a useful source of income but for many it isn’t enough to pay the bills. That puts a lot of emphasis on investments being a key source of cash to cover the cost of heating, electricity, council tax and so on.

Traditionally funds, stocks and bonds pay dividends or coupon payments once every three or six months. However, funds are increasingly speeding up their payment frequency to meet demand from retired individuals who want a monthly inflow of cash to help fund their monthly outgoings.

60 FUNDS ON OFFER

According to data from FE Analytics, there are currently around 60 funds available to UK retail investors which pay, or at least in the year before the pandemic paid, a monthly dividend.

Most of the highest yielding funds are what’s called ‘enhanced income’ funds. These funds normally pay a slightly higher yield than a standard income fund because they sell options on some of their holdings. This gives the purchaser the right, but not an obligation, to buy a stock from the fund at a pre-determined ‘strike’ price on a specific future date.

For this service, the fund receives a premium regardless

of whether the option is exercised or not. If the stock’s price does not hit the strike price by the time the contract expires the fund keeps the premium, which is distributed to investors as part of the overall dividend which also includes some or all of the natural income from the portfolio.

If the strike price is reached the fund keeps the premium, but it must pay any additional increase in the stock’s value over and above the strike price to the purchaser. That means the fund’s upside is limited – hence the investor is giving up potential gains in exchange for a higher dividend.

Other than that, monthly dividend-paying funds mostly feature in three main categories – bonds, property and multi-asset funds.

INCOME FINDER SERVICE

To help people find some of the best dividend-payers out there and organise payments into a smooth monthly schedule, investment trust organization the Association of Investment Companies (AIC) has developed something called the Income Finder.

It enables investors to create a virtual portfolio of income-paying investment trusts, also known as investment companies, track their dividend dates and see how much income they could receive over a year.

This allows investors to customise their investment trust portfolio to smooth monthly income over the year, ensuring there are no periods without dividend payments, or shape income to meet their needs.

For more information on this, head to theaic.co.uk/income-finder.

For this article, we’re going to focus on funds that pay a decent 3% yield or above. We take a look at monthly dividend paying funds, investment trusts and exchange-traded funds (ETFs) in each asset class and discuss the things you need to know, plus we suggest some funds to buy.

BONDS

Most bond funds that offer a monthly dividend tend to be ones that invest in high yield bonds, which are bonds rated below investment grade (bonds that are considered to have a lower risk of default), though there are some like Baillie Gifford Strategic Bond (0594774) which invest in both investment grade and high yield.

A non-investment grade rating is important as it suggests there is a greater chance of an issuer’s default, when the company does not pay the coupon/interest due on a bond or the principal amount due at maturity in a timely manner.

Consequently, non-investment grade debt issuers must pay a higher interest rate – and in some cases they must make investor-friendly structural features to the bond agreement – to compensate for bondholder risk, and to attract the interest of institutional investors.

High yield corporate bonds are invariably risker than others like UK government bonds, also known as gilts, for example, but in the bond market it’s the classic case of the higher the risk, the higher the reward.

Plus, most of the bonds in the majority of respectable high yield bonds funds come from large, well-known companies with strong balance sheets, so while there is higher risk, it’s not exactly like dabbling in cryptocurrencies.

Take monthly dividend payer Threadneedle High Yield Bond Fund (B7SGDT8) as an example. The top five bonds it holds come from Japanese tech investment giant Softbank, carmaker Fiat Chrysler, French telecoms company Altice (the second biggest in France behind Orange), Netflix and energy supplier EDF. Altice is the smallest company among that list, yet still has a market value of over £7 billion.

SHARES’ TOP PICKS

BAILLIE GIFFORD STRATEGIC BOND (0594774)

The Baillie Gifford Strategic Bond fund stands out as a top pick for someone looking for monthly income from a bond fund.

It has a good track record of paying decent dividends with historic yields ranging between 3% and 3.5% over the past five years, while it also offers potential for good capital growth ahead of inflation with a five-year annualised return of 6.95%. It is also a lot cheaper than many other bond funds with an ongoing charge of 0.52% a year.

The fund’s stated aim is to produce monthly income, though opportunities for capital growth are also sought subject to prevailing market conditions. Top holdings include bonds from Netflix, National Grid (NG.), Virgin Media and Time Warner Cable.

It’s worth noting that yields are currently very low across the bond market and there is no guarantee that you’ll get 3% yield in the near-term.

VANGUARD USD CORPORATE BOND ETF (VUCP)

There aren’t many ETFs that pay a monthly dividend, but one which does in the bond space is Vanguard USD Corporate Bond ETF (VUCP). ETFs track the performance of a basket of assets, so in this case a basket of bonds. They are typically lower cost than an actively managed fund.

The Vanguard ETF tracks the performance of 5,690 bonds, yielded just over 3% in 2020, and offers the potential for capital growth as evident by its three-year annualised total return of 7.13%. It charges

0.09% a year.

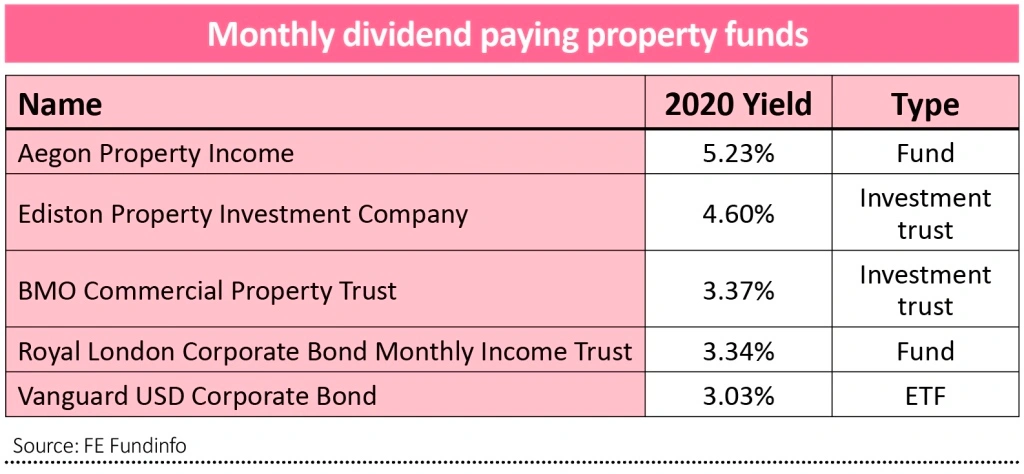

PROPERTY

Funds and investment trusts can give investors access to a wide range of properties across different sectors and potentially geographies.

In theory they should be able to rely on rental income from these properties and potentially benefit from any capital appreciation, which should translate into solid investment returns.

It’s important to be aware however that many open-ended property funds have suspended dealing in times of difficulty in the past, meaning investors have been unable to withdraw their money.

This happened most notably straight after the Brexit vote and then more recently during the market sell-off in March as the UK went into lockdown, with funds unable to accurately value their underlying properties in fast-moving markets.

Investment trusts are often seen as a better vehicle for less liquid assets like property, which are harder to buy and sell in short order, because they are listed on the stock market and the fund managers don’t have to factor in redemptions to how they invest. However, they will typically trade at a discount to net asset value at times of stress.

A lot of property funds, particularly ones paying monthly dividends, have big exposure to commercial property. There is a debate whether investing in commercial property is still a viable option and whether it can be relied upon for income in the same way as before, given the shift to online shopping and working from home.

PROS AND CONS

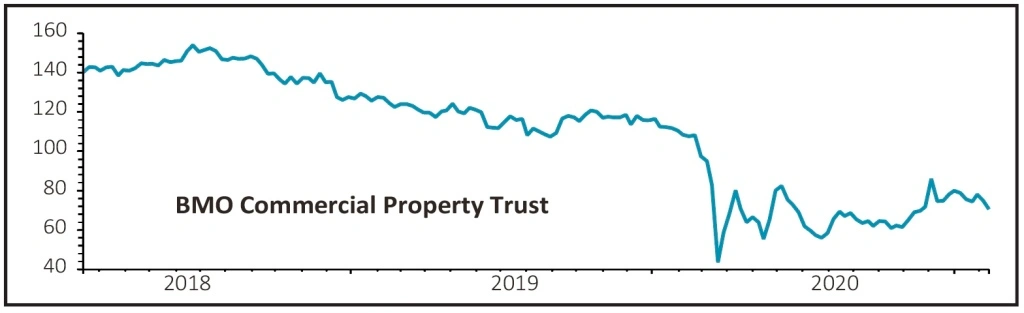

A good example is FTSE 250 investment trust BMO Commercial Property Trust (BCPT) which for a long time paid 0.5p per share dividend every month but had to stop payments for a period amid the height of the pandemic.

Dividends restarted in August at the lower rate of 0.25p per month and they’ve been paid every month since. Importantly, dividends are now starting to go up – rising 40% in December to 0.35p. On an annualised basis that equates to a 5.9% yield based on a share price of 70.7p.

Although uncertainty remains regarding the impact of continued lockdown restrictions on the trust’s portfolio and tenants, it expects to continue paying dividends at this rate for the foreseeable future.

‘BMO Commercial Property’s 0.5% increase in net asset for the three months to December is a positive step for the fund, following NAV declines in each of the first three quarters of 2020,’ says the investment trust team at Numis.

‘The modest capital increase in portfolio value masks the continued divergence in performance of underlying sub-sectors in the portfolio with industrial and logistics assets performing strongly in sharp contrast to the retail assets as well as alternative assets exposed to the leisure sector.’

Investors need to weigh up whether a 5.9% yield is a good enough reward for risks around rent collection, particularly as the backdrop for some of its tenants remains unfavourable.

This is very important – if you’re relying on your pension or ISA to provide income in retirement, you must think very carefully about the risks you are taking.

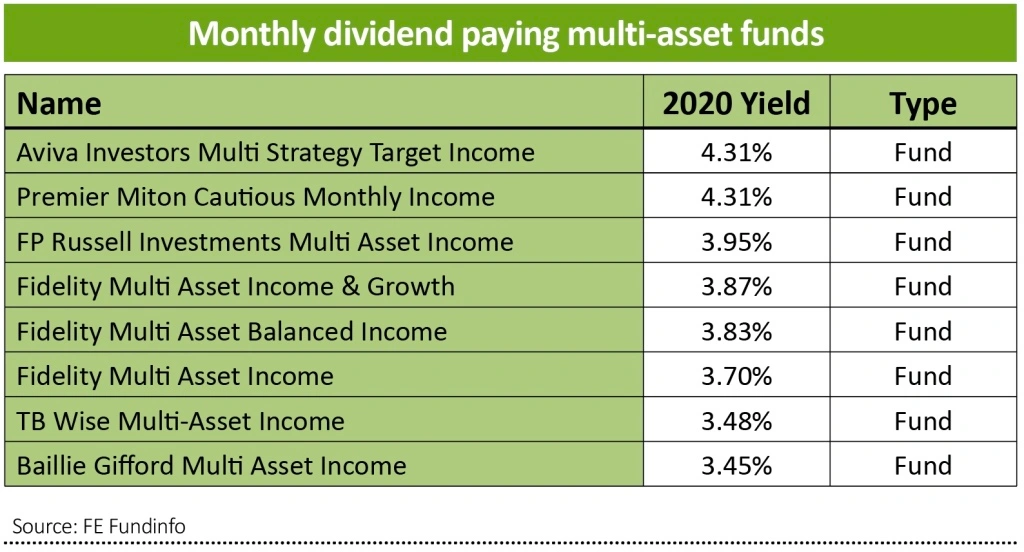

MULTI-ASSET FUNDS

If the property space currently seems like too much of a headache, more comfort could be found in multi-asset investments.

Multi-asset funds and trusts are those that invest in a range

of different things, most commonly stocks, bonds and other assets like property or commodities like gold.

They have been growing in popularity for a while as investors seek a one-stop shop for their money, with the funds having the freedom to invest wherever they see fit to meet their objectives.

A lot of funds in this sector have generally held up well following the March sell-off, though the diversification they provide while helping limit the downside, also means returns aren’t as strong when markets are rising.

SHARES’ TOP PICK

PREMIER MITON CAUTIOUS MONTHLY INCOME (B79QBF9)

Premier Miton Cautious Monthly Income invests across the major asset classes including company shares, government bonds, corporate bonds and gold, together with a very small amount in cash and property. It has a decent track record of dividend payments and capital growth.

It has a historic yield of 4.3% based on payments from 2020 and has delivered a five-year annualised return of 6.83%. It has a reasonable ongoing cost of 0.81% a year.

The fund distributes income on a monthly basis with 11 equal payments and whatever’s left in the pot at the end of the year.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.