Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCreating a plan to invest cash saved during lockdown

This is the first part in a regular series in which we will provide an investment clinic based on hypothetical scenarios. By doing so we aim to provide some insights which can help different types of investor from beginners all the way up to experienced market participants.

The 43-year-old already has shares in the banking firm for whom he works through a SAYE (save as you earn) scheme and has additional exposure to the markets through a defined contribution pension, with money going into a mix of UK, US and emerging market stocks and bonds.

He has paid off a significant portion of his mortgage, accumulated a rainy-day savings pot worth three months’ salary in an easy-access Cash ISA, and has no significant credit card or bank debt.

Shaheen wants to build up a nest egg which could potentially help him towards a targeted retirement age in his late 50s. Being stuck at home in lockdown means he is spending £400 a month less on commuting, gym membership and meals out. He has put aside 10 months’ worth of these savings since the first lockdown restrictions began in mid-March 2020, adding up to £4,000.

He wants to use that money to invest now and find a way to keep squirreling away £250 a month into stocks or funds (on top of his pension contributions) once lockdown ends. Shaheen is confident of having this spare cash every month as he intends to cycle to work which not only saves money on train fares but also keeps him fit, meaning he can cancel his gym membership.

He has some knowledge of the markets but wouldn’t describe himself as an expert. Shaheen’s goal is to achieve an annual return of at least 6%.

IS THAT A REALISTIC GOAL?

The first thing to note is that Shaheen is in a good place to start investing more. He’s already putting money into his pension every month with his employer also making contributions. He has a decent level of emergency savings and, even in his best-case scenario, he is still more than 10 years away from retiring which provides some time to absorb any short-term market volatility.

With interest rates so low, there is a good case for investing spare cash so that the money can work a bit harder.

A 6% return feels realistic, particularly once you factor in dividends. On a total return basis (encompassing capital gains and reinvested income) the FTSE All-World index has delivered an annualised 6.8% over the last 10 years.

To shelter these returns from capital gains and income tax it is worth considering a Stocks & Shares ISA. Even having used some of the current year’s ISA allowance in cash, Shaheen still has plenty of headroom to the generous £20,000 annual limit across the different types of ISA. It’s worth noting that he is too old to qualify for a Lifetime ISA.

In terms of getting started it might make sense to put his £4,000 lump sum into a Stocks & Shares ISA and to spread it across a variety of investments. Going forward and assuming £250 monthly deposits into his ISA, he might want to invest £500 in a single asset every other month.

Dealing fees are often charged at a flat rate so, in percentage terms, the more you are putting in the lower your costs. A typical £10 charge to buy shares in a company, investment trust or exchange-traded fund would equate to 2% of a £500 investment – but a less appealing 4% if investing £250 once a month.

Setting up a direct debit to fund the ISA is also a good idea as it will take the hassle out of remembering to transfer funds.

INVESTMENT OPTIONS TO CONSIDER

Given his pension includes a diversified mix of global stocks and bonds, Shaheen already has a solid ‘core’ to his investment portfolio. He could therefore consider adding some ‘satellite’ holdings to an ISA which are higher risk in nature.

One option is for Shaheen to buy shares in individual companies, with an argument for looking outside the banking sector given he already has exposure through owning shares in his financial services industry employer.

To begin with, it might make sense for Shaheen to look at businesses where he is familiar with their products or services as it is important to invest in things you understand. In this situation, it would be worth him taking the time to read some annual reports to get a clear idea of a company’s performance and prospects before buying their shares.

He likes to play games on his Nintendo Switch at home, so Shaheen might want to look at the computer games sector as he should know which games are popular and the companies that make them. One that might appeal is Sumo (SUMO:AIM) which started life as a ‘work for hire’ games developer and has since gone on to develop its own intellectual property.

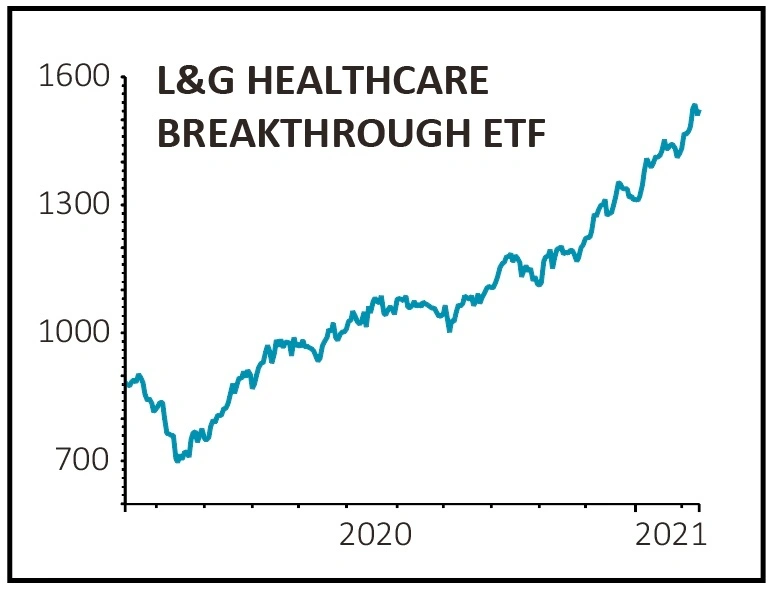

Another option for Shaheen is to buy a thematic exchange-traded fund that plays into a specific investment theme. For example, L&G Healthcare Breakthrough ETF (DOCG) would provide Shaheen with exposure to innovation within healthcare, across both developed and emerging markets. It has an in-built charge of 0.5% a year to cover the costs of running the product.

Shaheen would have to pay additional charges on top to his investment provider, such as the cost of buying shares in the ETF and potentially ongoing custody fees. The same would apply when making other investments, such as buying shares in individual companies, funds and bonds.

A third option for Shaheen is to buy a fund or investment trust which invests globally in smaller companies. While small caps typically come with higher risks there can be more room for growth than with larger, more mature firms.

FINANCIAL BENEFITS OF LOCKDOWN

LOCKDOWN SAVINGS: Shaheen has saved £400 a month since March 2020 as he hasn’t had to incur costs associated with commuting, gym membership or eating out. He wants to invest that saved money.

GOAL ONCE LOCKDOWN ENDS: Save £250 a month by cycling to work and not returning to the gym – and invest that money.

There are five investment trusts in the Association of Investment Companies’ Global Smaller Companies sector. The only one to have a consistent top quartile position for performance over one, three, five and 10 years is Baillie Gifford-run Edinburgh Worldwide (EWI), according to FE Fundinfo data which shows it has generated 607% total return over 10 years.

While strong performance over a long timeframe would suggest the people running Edinburgh Worldwide know what they’re doing, it is important to consider that what’s done well in the past isn’t guaranteed to do well in the future.

The investment trust invests in companies which it believes to offer long-term growth potential. The companies are typically valued at less than $5 billion at time of initial investment, but Edinburgh Worldwide will often hang on to them as they become a lot bigger. That explains why you have some very large companies like Tesla in the portfolio as well as smaller ones like engineer Ricardo (RCDO).

DISCLAIMER. This article is based on a fictional situation to provide an example of how someone might approach investing. It is not a personal recommendation. It is important to do your research and understand the risks before investing.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.