Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWorld index hits new all-time high on US stimulus hopes

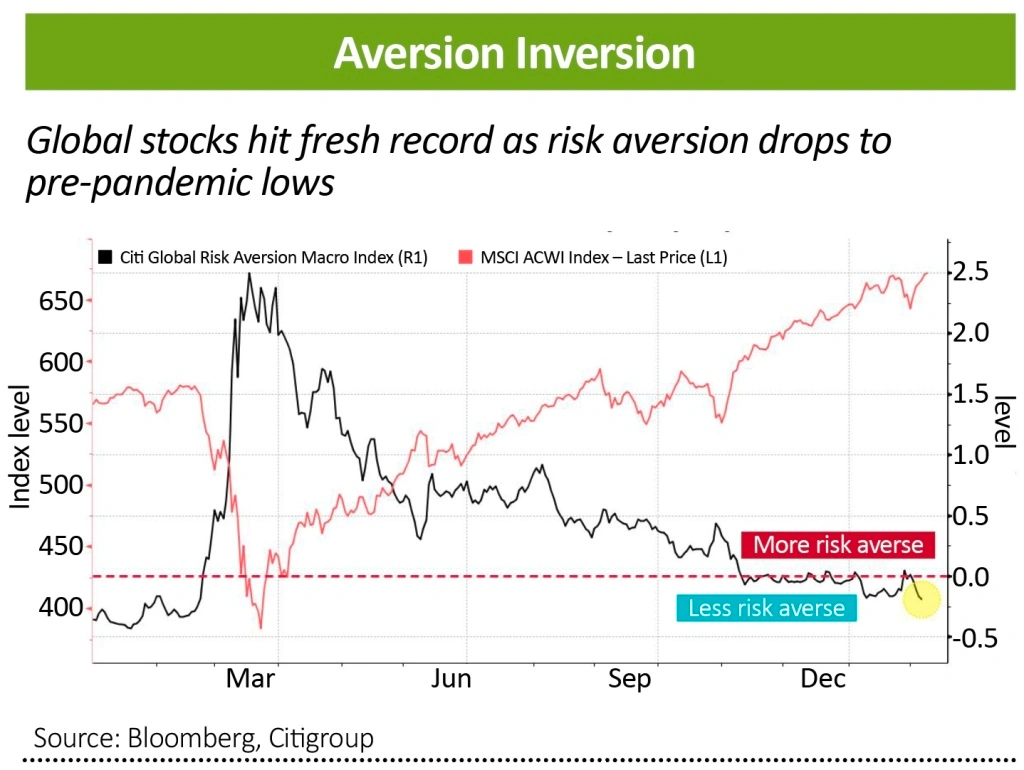

With markets approaching the one-year anniversary of their pre-Covid-highs, it might seem surprising that the MSCI All Countries World index, the benchmark most used by global funds, is hitting new all-time highs.

Thanks to unprecedented monetary and fiscal stimulus by the world’s central banks, markets have recovered sharply from last year’s depths of despair even though earnings for a large part of the economy have been wiped out.

Investors who were already bullish are even more bullish. Howard Ward, director of growth products at Gabelli Funds, says stocks are ’the only game in town’.

Bond investors meanwhile have to scrape the barrel and buy BB- or junk-rated bonds just to generate a positive real yield.

We’re at the stage in markets where risk appetite is so high – or to put it another way, risk aversion is so low – that what would normally be seen as bad news has become good news.

The latest US non-farm payroll data, which showed a big downward revision to the November figure suggesting far fewer jobs were created than at first sight, actually saw the Nasdaq and S&P indices make new highs following the news.

The argument is that, under Secretary Janet Yellen, the Treasury will move quickly to deploy its stimulus in order to create more jobs, rather than wait for evidence that the economy actually needs it.

Even rising Treasury yields – the US 10-year government bond is heading towards 1.25% again for the first time since 2017 – are no longer seen as a negative. Although debt levels are high, the bulls argue that the fact the market can tolerate higher interest rates and higher inflation is another reason to own certain types of stocks.

Many analysts believe that by targeting an average inflation rate of 2%, the Fed will let prices overshoot in order not to rush into tightening, so market interest rates (yields) will continue to rise.

Also worth noting is the sudden fall in the Vix volatility or ‘fear’ index. In the week to 5 February it lost 44%, the second sharpest fall on record. This might normally be a cause for concern, yet a look at the historical returns 12 months after similar falls in the Vix is encouraging for stocks.

On the five previous occasions when the gauge fell by 40% or more in a week, 12-month returns were uniformly positive, ranging from 5% to as much as 30% with an average of 20%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- New-look Bango is a great way to play online payments boom

- Reasons why Texas Instruments shares are still worth buying

- GlaxoSmithKline remains attractive despite delay to recovery

- The retail giant with a chance of beating Amazon

- Ocado delivers on growth at the expense of short-term earnings

- Credit-scoring firm should repay the patient investor