Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy the inflation debate is more than just hot air

There is a general rule that the most vituperative arguments are those that take place between academics, because the stakes (and the implications for the real world) are so small.

Usually, such debates can be watched with detached amusement, but there is one current spat which does command attention, especially from an investment perspective.

Larry Summers – former US Treasury secretary under president Bill Clinton and former economic adviser to Barack Obama – is involved in a fierce set-to with current Treasury secretary and former US Federal Reserve chair Janet Yellen. To add spice to proceedings, Summers was reportedly an unsuccessful candidate when Yellen got the post at the US central bank in 2013.

Yellen is actively endorsing the Biden administration’s fiscal stimulus plans, arguing that spending too little could do more harm than spending too much.

Judging by his columns in The Washington Post, Summers seems to disagree, in the view that too much stimulus could unleash inflation.

Yellen, perhaps conveniently ignoring how her four years as Fed chair employing ultra-loose policies employed by both her predecessor, Ben Bernanke, and her successor, Jay Powell, cannot point to any sustained progress in stoking inflation. She asserts that any such threat is being monitored and can be swiftly contained.

Cue much eye-rolling from Summers, whose antipathy to the quantitative easing (QE) policies used as ‘temporary’ measures by the Fed since 2008 is also well known.

If Yellen is right, then investment portfolios can stay slanted toward momentum and growth strategies and long-duration assets such as government bonds with a decade or more to maturity and technology and biotechnology stocks – in other words, what has a great track record over the last decade will keep delivering, if history is any guide.

But if Summers is right, then the whole game changes. If inflation pops higher and stays that way, then history suggests investors need to be exposed to short-duration assets such as ‘value’ equities (cyclical growth and recovery stocks), emerging markets and ‘real’ assets such as commodities and precious metals.

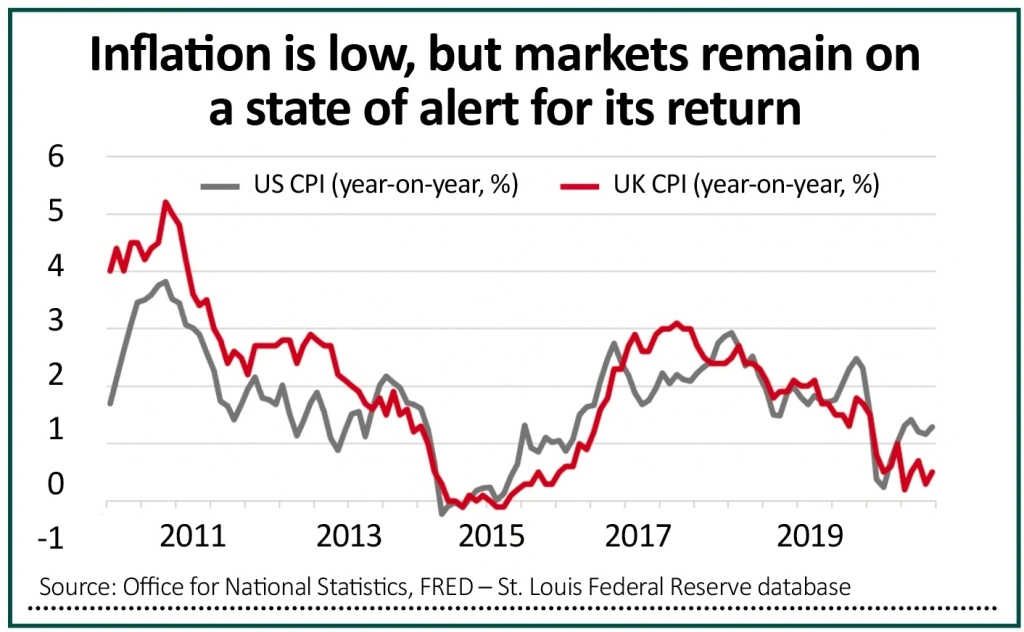

BASE EFFECT OR BOUNCE?

Again, the headline inflation numbers are benign. There will be a base effect for the rest of 2021, as the pandemic-induced recession comes up as a comparator.

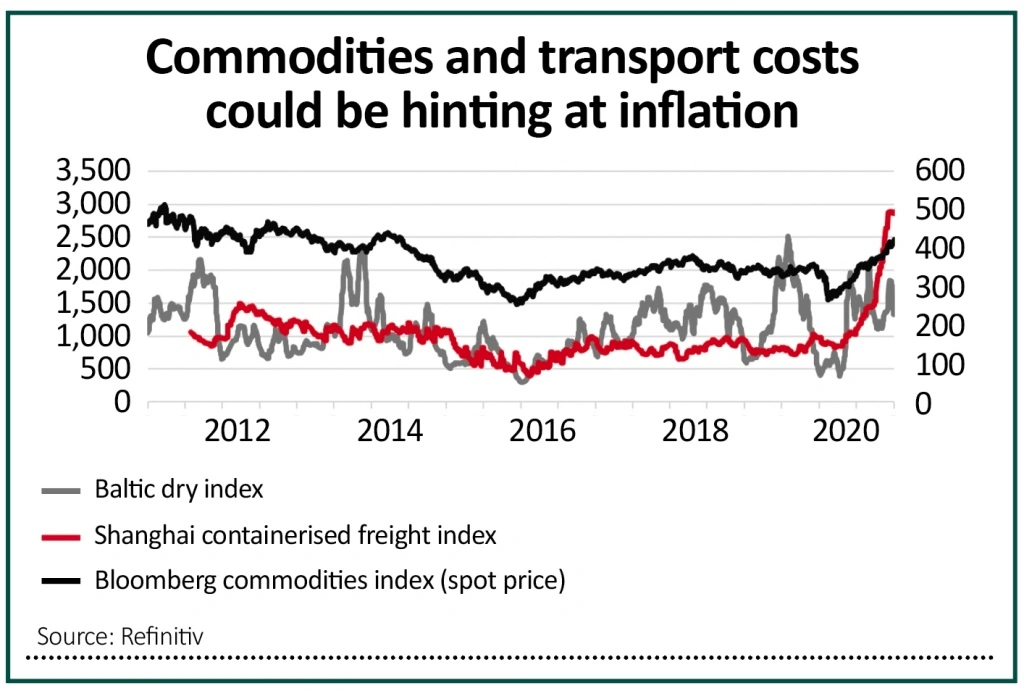

Doubtless central banks will dismiss that as transitory rather than signs of a fundamental cost pressures, even if the price of vital raw materials from oil to metals and crops is on the march if the Bloomberg Commodity index and shipping’s Baltic Dry benchmark are any guide.

If there is any good news here is might be that the Shanghai Containerised Freight index is maybe topping out after a stunning run, but all these trends are indicators of cost pressures building in the pipeline.

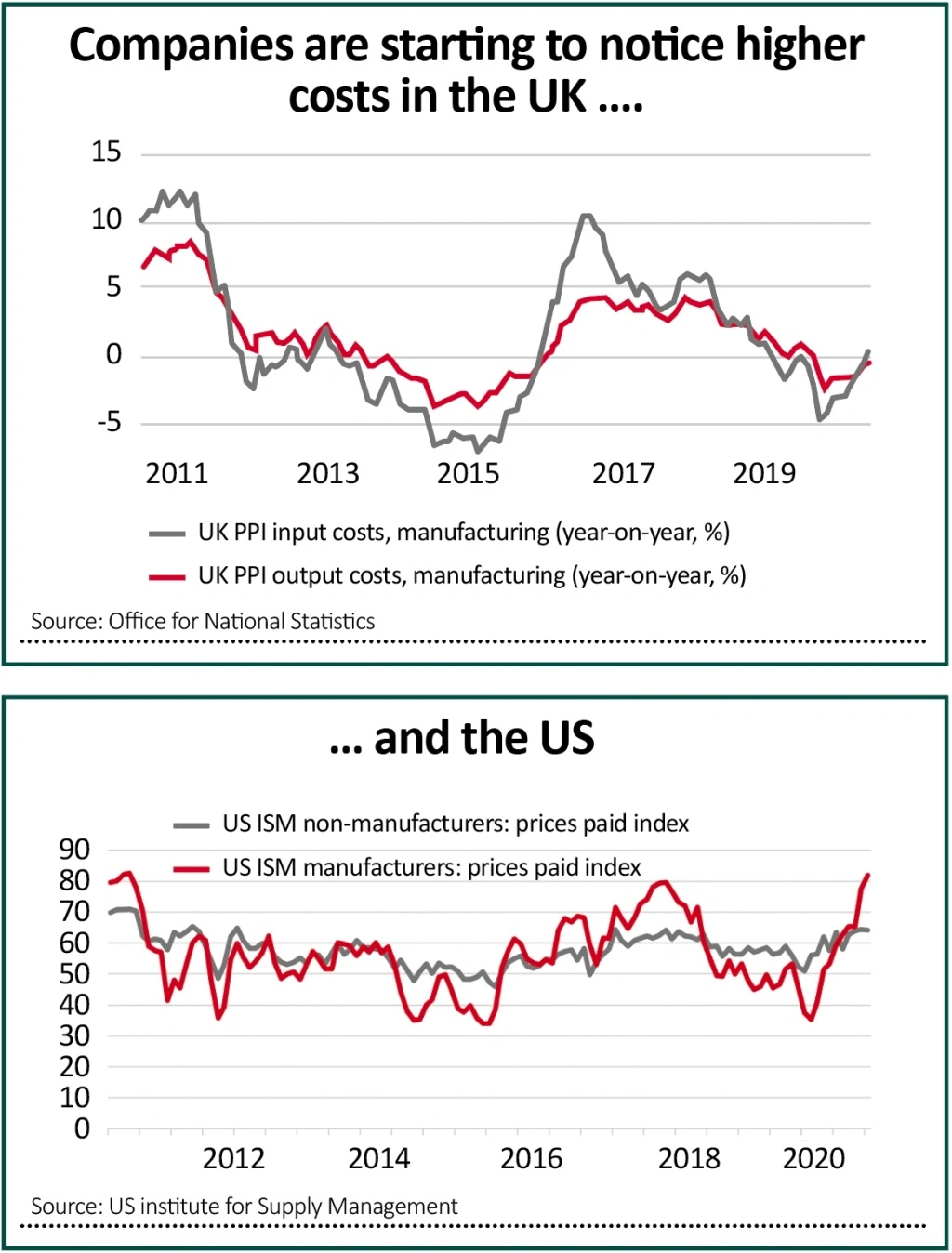

Companies are already paying attention – because they must. Input costs and output prices are showing some momentum in the UK, while American firms are flagging a sharp increase in their costs in the latest purchasing managers’ indices.

Muted demand, owing to the pandemic, lockdowns and increased unemployment, could keep a lid on this trend but a strong bounce back at a time when supply is crimped by company closures and supply chain disruption remains a possibility, too.

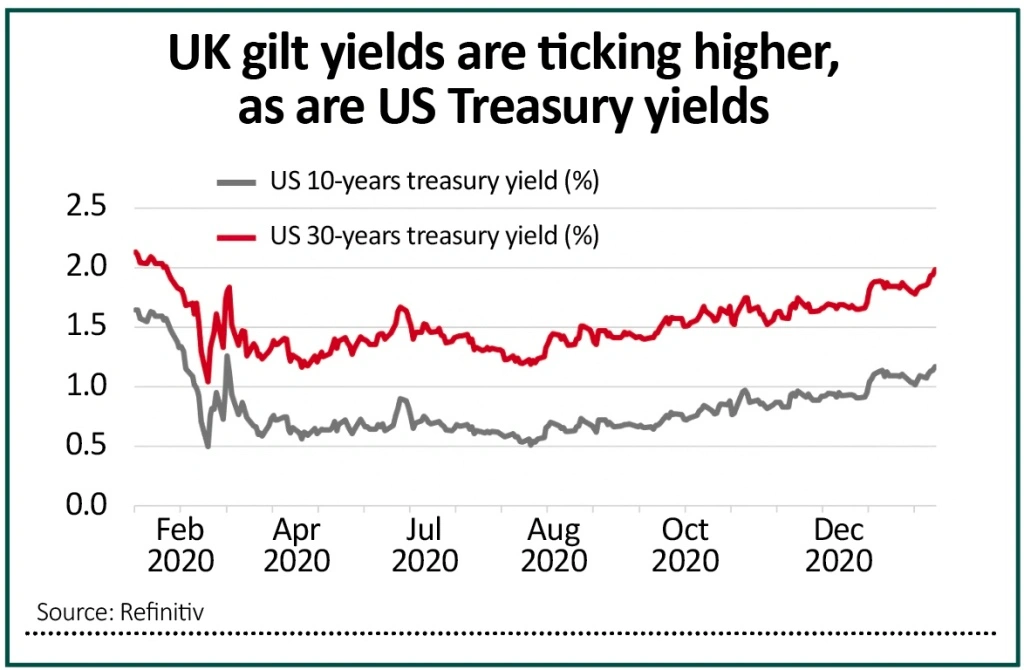

FRETFUL FIXED INCOME

Fixed-income investors are paying attention because government bond yields are rising. They still stand at what are historically low levels, so it would be wrong to say bond investors are in a tizzy.

They still seem to believe the Yellen narrative that inflation can be managed and that central banks can just keep throwing money at fixed-income markets via QE to put a lid on bond yields. That would keep bond prices high but gilts’ and treasuries’ skinny yields would offer holders little or no protection if the inflation genie finally pops out of the bottle.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- New-look Bango is a great way to play online payments boom

- Reasons why Texas Instruments shares are still worth buying

- GlaxoSmithKline remains attractive despite delay to recovery

- The retail giant with a chance of beating Amazon

- Ocado delivers on growth at the expense of short-term earnings

- Credit-scoring firm should repay the patient investor