Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUnderstanding your new ‘Investment Pathways’

Hundreds of thousands of people who choose to keep their retirement pot invested while taking an income through drawdown will from 1 February be offered ‘Investment Pathways’. The same is true of those who transfer a drawdown plan to a new drawdown provider.

This change, instigated by the Financial Conduct Authority (FCA), is significant and it is vital savers understand the new options available to them.

One of the central aims of these reforms is to reduce the number of people holding cash or cash-like investments for the long term and seeing the value of their money whittled away by inflation.

The FCA also wants more people to think about their investments when going into drawdown so they remain appropriate to their needs.

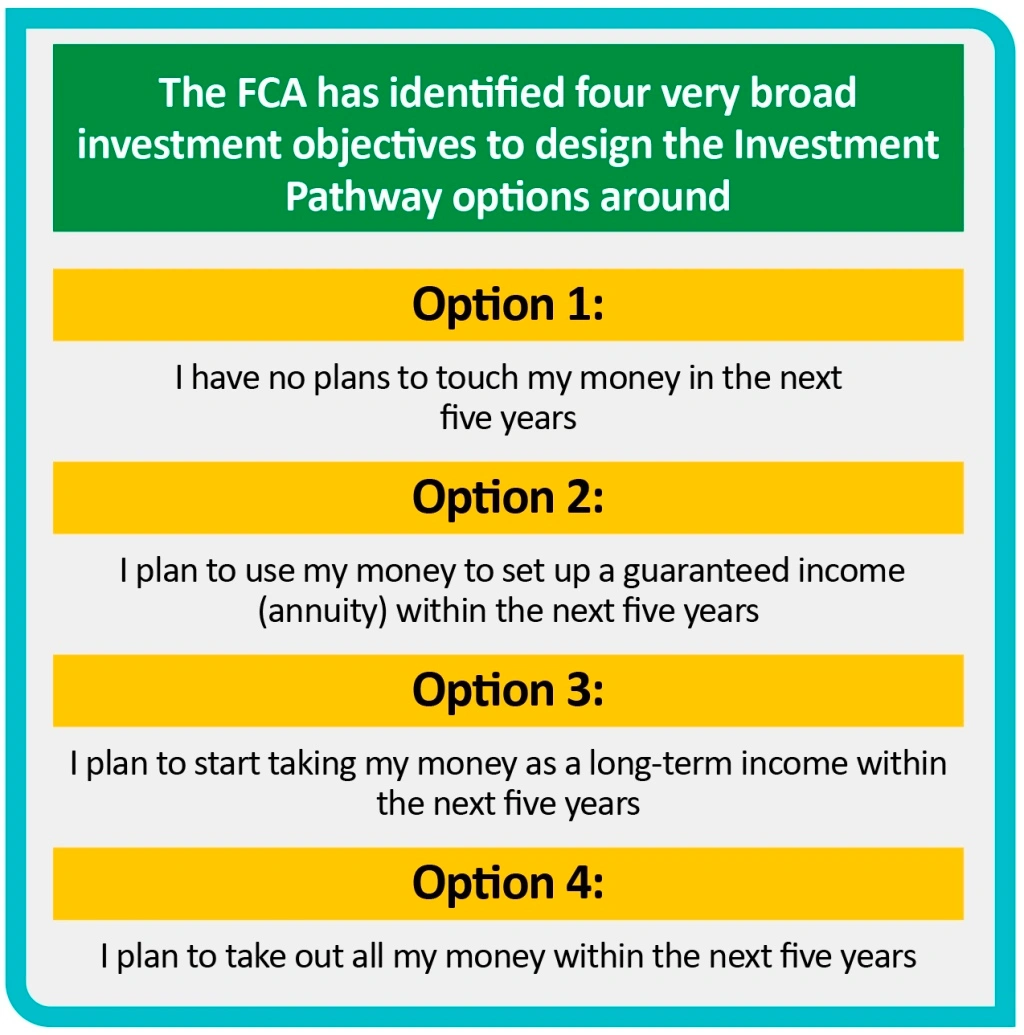

There are a few fundamental things you need to know about these Pathways options. Firstly, they aren’t being presented to you based on your personal circumstances but rather offer very broad investment options based on four basic outcomes.

Secondly, they do not take into account your appetite for risk or withdrawal strategy in any detail and must therefore not be seen by as a replacement for engagement or seeking regulated financial advice.

Finally, responsibility for investment decisions continues to rest with you.

If you chose a Pathways fund you still need to check the risk level and objective of the fund is aligned with your needs and that you are comfortable with the charges you are paying in return for the service being offered.

If you enter drawdown - whether invested in Pathways or having chosen your own investments – you need to regularly review your investments to ensure they are delivering against your objectives and remain appropriate for your evolving personal circumstances.

WHY ARE INVESTMENT PATHWAYS BEING INTRODUCED?

The reforms are designed to help savers make better decisions on how to invest their drawdown fund and ensure they do not end up holding large portions of their pension in cash or cash-like investments over the long-term.

This is because the FCA is worried people who hold too much cash in their pension risk missing out on valuable investment returns and having the real value of their pension eaten away over time by inflation.

There will be no obligation on people to invest in Pathways, however, and many will prefer to choose their own investments to better meet their attitude to risk, retirement plans and long-term goals.

WHO WILL BE AFFECTED?

The new rules will impact people who do not take financial advice and choose to keep their money invested while taking an income in retirement (‘drawdown’).

This includes people who move all or part of their pension savings into drawdown, or people who transfer funds already in drawdown to a new provider.

WHAT WILL PEOPLE ENTERING DRAWDOWN OR TRANSFERRING TO DRAWDOWN EXPERIENCE?

If you enter drawdown or transfer to a drawdown account, from 1 February you will initially be given the option of:

– Choosing an Investment Pathway;

– choosing their own investments; or

– sticking with the investments they already have

If you choose your own investments or stick with the investments you already have, your ‘Pathway’ journey will come to an end.

If you choose the Investment Pathway route, pension companies will be required to offer you four Investment Pathway options. These will not be tailored based on your personal circumstances, but rather designed around four very broad retirement income objectives.

Pension companies will then offer an Investment Pathway fund depending on which option you have chosen.

WHAT HAPPENS IF I DECIDE I WANT TO BUY AN INVESTMENT PATHWAY FUND?

This will depend on the approach taken by your provider. If an AJ Bell customer indicates they want to buy an Investment Pathway fund, they will then go through the normal process of being placed into drawdown.

Once in drawdown, you retain responsibility for purchasing your investments – including Investment Pathways funds.

Where an AJ Bell customer said they wanted to buy an Investment Pathway investment then doesn’t – either keeping their money in cash or choosing different investments – they will be sent a reminder of their original choices.

However, as is always the case with do-it-yourself investments, it will be up to the individual investor to complete any transaction.

HOW MUCH WILL PATHWAYS INVESTMENTS COST?

Again, this will vary from provider-to-provider. AJ Bell Youinvest customers will be offered the following Pathways funds:

Option 1:

I have no plans to touch my money in the next five years

Fund: VT AJ Bell Balanced Fund (BYW8RX1)

Objective: To achieve long-term capital growth with a balanced approach between defensive assets such as cash, fixed interest securities, money-market funds and collective investment schemes following alternative strategies such as property and commodities, and higher risk assets such as equities.

Fund OCF: 0.34% plus platform charge of a maximum 0.25%

Option 2:

I plan to use my money to set up a guaranteed income (annuity) within the next five years

Fund: VT AJ Bell Cautious Fund (BYW8RV9)

Objective: To achieve long-term capital growth with a high level of exposure (often indirect) to defensive assets such as cash, fixed interest securities, money market funds and collective investment schemes following alternative strategies such as property and commodities and a low level of exposure to higher risk assets such as equities.

Fund OCF: 0.35% plus platform charge of a maximum 0.25%

Option 3:

I plan to start taking my money as a long-term income within the next five years

Fund: VT AJ Bell Income Fund (BH3W744)

Objective: To generate an income, whilst maintaining capital value over a typical investment cycle. It has a target average yield of 3-5% per annum (over a trailing three year period), which is not guaranteed. This is consistent with a goal of capital preservation and drawdown of an income.

Fund OCF: 0.74% plus platform charge of a maximum 0.25%

Option 4:

I plan to take out all my money within the next five years

Fund: VT AJ Bell Cautious Fund (see previous)

AJ Bell Youinvest’s annual platform charge for funds is:

– 0.25% on the first £250,000 funds invested;

– 0.10% on the fund value between £250,000 and £1 million;

– 0.05% on the fund value between £1 million and £2 million;

– No charge on the fund value over £2 million.

WHAT HAPPENS IF I CHOOSE TO INVEST MY DRAWDOWN FUND IN CASH OR CASH-LIKE INVESTMENTS?

If you invest 50% or more of your new drawdown fund in cash or cash-like investments then your provider will check to make sure your have made an active decision to do that.

Your provider will also warn you that the fund is in danger of being eroded by inflation.

WHERE CAN I GO FOR FURTHER INFORMATION?

Pension Wise offers free and impartial Government guidance to people over 50 who have a personal or workplace pension and will cover Investment Pathways. The Money and Pensions Service will also be offering an Investment Pathways comparison tool.

If you want more bespoke help tailored to your individual needs you should seek regulated financial advice.

DISCLAIMER: The value of investments can go down as well as up and you may get back less than you originally invested. Target yields are not guaranteed and can fluctuate.

Shares magazine is owned and published by AJ Bell. The author (Tom Selby) owns shares in AJ Bell. Shares’ Deputy Editor Tom Sieber who edited this article also owns shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- New-look Bango is a great way to play online payments boom

- Reasons why Texas Instruments shares are still worth buying

- GlaxoSmithKline remains attractive despite delay to recovery

- The retail giant with a chance of beating Amazon

- Ocado delivers on growth at the expense of short-term earnings

- Credit-scoring firm should repay the patient investor