Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

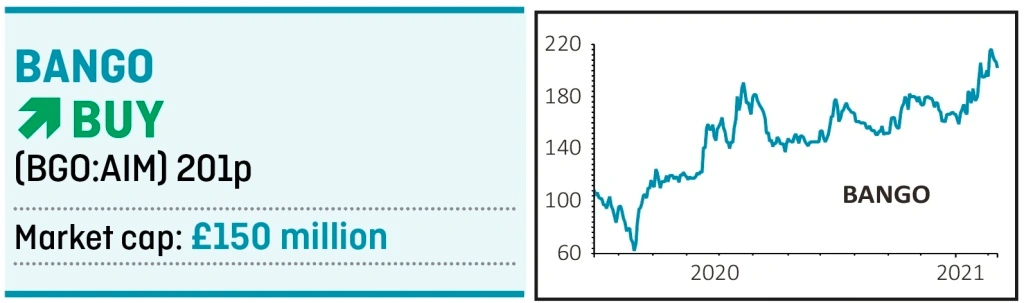

magazineNew-look Bango is a great way to play online payments boom

The digital payments space is booming and not just because of lockdown. We are all buying more stuff online, and that requires safe and easy ways to pay.

A forecast-thumping fourth quarter for industry leader Paypal earlier this month saw its stock jump to new all-time highs.

Cambridge-based Bango (BGO:AIM) is much smaller but well worth a look.

It runs a direct carrier billing (DCB) payments platform. This is a ‘one-click’ solution that allows online shoppers to buy goods and services by adding the internet shopping charges to their mobile phone bill, once they have set up an account.

That’s great for many consumers uncomfortable submitting debit or credit card details online. It also provides data insights that help improve the user experience and can help to acquire more paying customers.

Bango makes its money by getting a tiny percentage per transaction, about 0.6% in 2020. This produced £12.2 million revenue last year on £1.9 billion end user spend (EUS), the latter doubling for the fifth consecutive year.

Crucially, this will mean adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) of more than £4 million, finally making the profits breakthrough after nearly two decades of trying.

But $1.9 billion EUS is a drop in the ocean compared to the $4.9 trillion of digital payments estimated globally last year. According to Statista data, the space is set for annual compound growth of 13.4% between now and 2024, putting the digital payments market at $8.17 trillion by 2024.

Bango already connects online app stores and merchants to over 3 billion users across the globe and on many of the world’s biggest online platforms.

Merchants including Amazon, Google, Microsoft and Samsung, mobile network operators such as O2, Vodafone and T-Mobile, and pay TV, cable and fixed-line operators use Bango payment technology to provide new ways to pay that are fast, simple and secure. BT (BT.A) came aboard in November to help power bundled subscription services like Britbox.

FinnCap believes that Bango’s DCB platform is becoming ‘cornerstone technology’ in the rapidly growing global market for subscription-based entertainment, and is expanding into areas like virtual gym memberships and food clubs, as well as video, music and game-streaming subscriptions.

Bundling multiple services is becoming an increasingly powerful tool, helping to win new customers for platforms and to retain existing ones.

Bango has showed promise before only to disappoint so the stock remains higher risk. That said, revenue could grow at more than 20% for several years, and with a largely fixed cost base, we anticipate rapid profit expansion which could light a fire under the stock. Forecasts will be updated following 2020 results on 16 March which could act as a near-term catalyst for the stock.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- New-look Bango is a great way to play online payments boom

- Reasons why Texas Instruments shares are still worth buying

- GlaxoSmithKline remains attractive despite delay to recovery

- The retail giant with a chance of beating Amazon

- Ocado delivers on growth at the expense of short-term earnings

- Credit-scoring firm should repay the patient investor