Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBest buying opportunity for Unilever shares in 11 months

The Marmite effect seems to have put FTSE 100 stock Unilever (ULVR) in the ‘hate it’ rather than ‘love it’ camp with many investors. The shares have been out of favour since the market started to prefer value stocks last November, with Unilever seen as an ‘expensive defensive’ and not offering the level of growth that can be found among cheaper-priced stocks.

A strategic update alongside full-year results (4 Feb) triggered another decline, with the shares at £39.80 now having fallen almost to the £37.26 low seen at the worst of the global market sell-off in March 2020. Investors were disappointed at news of shrinking margins and guidance for heavy restructuring costs over the next two years.

Unilever is targeting 3% to 5% sales growth over the longer term. The consensus analyst forecast is 2.6% growth in 2021, 3.3% in 2022 and 1.6% in 2023 so the consumer goods giant will need to work harder to meet growth targets.

In an environment where investors have been obsessed with fast growth, it is understandable why many people wouldn’t be interested in Unilever. However, there is considerable merit in owning the shares for the long term.

According to SharePad, over the past 10 years Unilever has achieved 1.4% annualised sales growth, roughly on a par with Imperial Brands (IMB) and Tesco (TSCO). While this may look dull, Unilever as an investment has been far from boring.

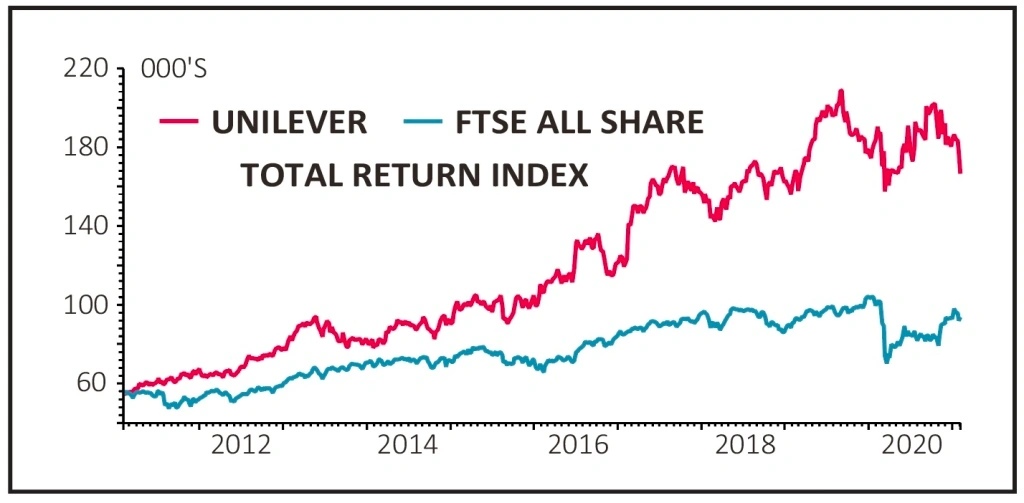

Over the past 10 years it has delivered a 204% total return which encompasses share price gains and dividends reinvested, based on Refinitiv data. This is nearly triple the total return from the FTSE All-Share index (71%) over the same period.

Its products are in demand in both good and bad economic conditions, hence why people call it a ‘defensive’ stock.

Importantly, it is one of the few companies delivering on positive environmental, social and governance factors rather than just declaring an intention.

Ten years ago, it declared an ambition to become the world’s most sustainable business and its achievements to date have been commendable such as sourcing all of its agricultural raw materials sustainably. It is now driving equality in the supply chain.

Cash generated from operations is reinvested in the business which gives it an advantage in marketing and product innovation, and it funds a growing stream of dividends.

Unilever is not perfect by any means. Some of its brands have limited growth potential, so they are likely to be sold. There is talk of the company wanting to make big acquisitions and with that comes the risk of over-estimating cost synergies or overpaying, just as Reckitt Benckiser (RB.) did with its purchase of Mead Johnson.

The group has lagged some of the consumer goods peers during the pandemic because of its smaller exposure to cleaning products. It may also be looking with envy at Nestle which is streets ahead in pet care.

However, we’re confident that Unilever can move with the times and just because the shares are unloved today doesn’t mean they will stay that way permanently. A diversified portfolio needs a reliable name like Unilever and its moment in the sun will come again (and again) in the future.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- New-look Bango is a great way to play online payments boom

- Reasons why Texas Instruments shares are still worth buying

- GlaxoSmithKline remains attractive despite delay to recovery

- The retail giant with a chance of beating Amazon

- Ocado delivers on growth at the expense of short-term earnings

- Credit-scoring firm should repay the patient investor