Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineYour checklist for the end of the tax year

It is that time of the year when many of us will be logging onto the HMRC website and filling in our self-assessment tax returns to meet the 31 January deadline.

It’s a pretty soul-destroying process. It requires quite a lot of work, and at the end of it, the reward for your efforts is usually a tax bill to pay. There’s not a great deal you can do to make it better this time around, because you’re paying for the last tax year (2019/2020).

But there are some things you can do to save tax in this financial year, before it ends on 5 April. Most of them will make next January a little easier on the wallet.

ISAS AND PENSIONS

ISAs and pensions are a great way to save for the future because your investment returns are free from income tax and capital gains tax.

All adults can save a maximum of £20,000 each year in ISAs, whether that be a cash ISA, Stocks and Shares ISA or a Lifetime ISA.

Importantly, if you don’t use all of the allowance, it can’t be carried forward, so you lose it for good. Investors with unused ISA allowance for this year should consider using it if they can before the 5 April deadline.

The pension annual allowance for adults is 100% of earnings, up to a maximum of £40,000. People with no earnings can still save up to £3,600 a year in a pension.

The pension annual allowance can be carried forward for up to three years but it will be lost eventually, so investors should consider whether they have made as much use of their pension annual allowance ahead of the end of the tax year.

If you don’t want to commit fresh money to the market, or you don’t have any spare cash at the moment, you can do a Bed and ISA, or a Bed and SIPP, which involves funding an ISA or SIPP contribution using investments you already hold outside a tax shelter.

GOVERNMENT TOP-UPS

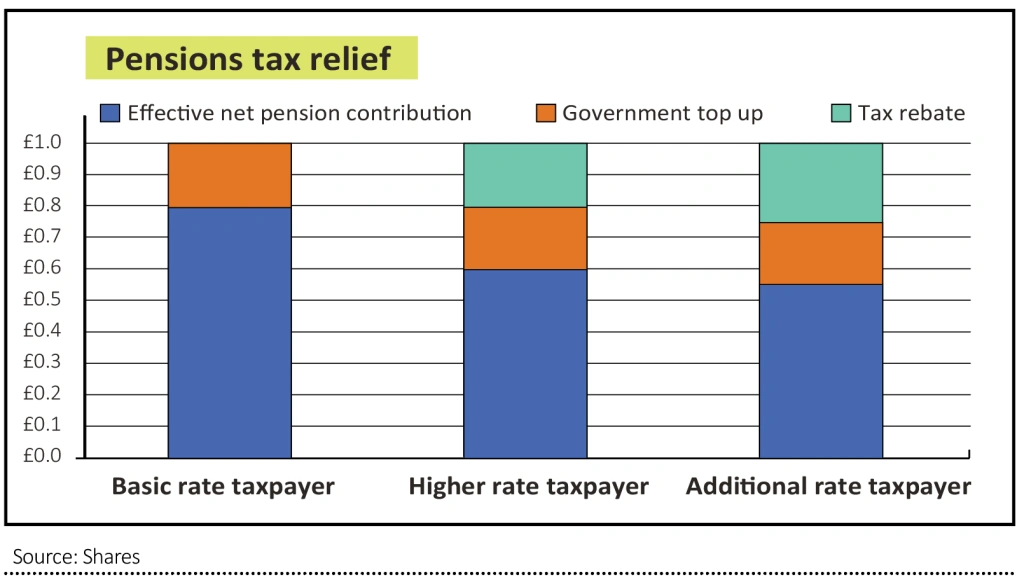

A significant benefit of pensions and Lifetime ISAs is that any money paid into them will benefit from a top up from the government. This is most generous in pensions, where personal contributions are automatically topped up by 20% in the form of pension tax relief.

That means that every 80p you pay into your pension is automatically topped up to £1. Higher rate and additional rate taxpayers can reclaim an additional 20% or 25% tax relief respectively via their tax return. So, for a higher rate taxpayer, every £1 that ends up in their pension only costs them 60p.

With the Lifetime ISA, you can get up to £1,000 a year in the form of a Government bonus, up until the age of 50. If you opened a Lifetime ISA at age 18, that is a maximum Government bonus of £32,000 (or £33,000 if you’re lucky enough to have your 18th birthday before 6th April).

Lifetime ISAS are more restrictive than other ISAs. You can only open one if you’re between 18 and 40, and you can save up to £4,000 each year. You can withdraw the Lifetime ISA money once you’ve reached age 60, or to buy your first property. But be warned that if you take the money for any other reason you’ll pay an exit penalty which is currently 20% but will increase to 25% on 5 April.

USE YOUR CGT ALLOWANCE

For investments held outside an ISA or pension, the annual capital gains tax (CGT) allowance is very valuable. Investors can make investment gains of up to £12,300 a year without paying any tax.

Gains over that amount are added to income and if they fall in the basic rate tax band are taxed at 10% and if they fall in the higher rate tax band are taxed at 20%. An additional 8% is added if the gains are from a second property.

The annual CGT allowance cannot be carried forward into future years so if you don’t use it, you lose it. If you have investments with gains outside of an ISA or pension therefore, you might consider taking some profits before the end the tax year to make the most of the tax free allowance. You can also transfer investments to your spouse or civil partner, in order to use their annual CGT allowance too.

CONSIDER LIFETIME GIFTS

Gifting money in your lifetime needs careful consideration to avoid any surprise tax bills. Lifetime cash gifts are known as PETs, or potentially exempt transfers, and can create an inheritance tax charge if you, as the donor, pass away within seven years of the date of the gift.

However, you also have an annual gift allowance of £3,000, and any unused allowance can be carried forward, but only for one year. Gifts of up to £250 made to an individual are also exempt each tax year. You can also make regular gifts of any size out of surplus income without paying tax, provided your lifestyle is not affected.

START SAVING FOR YOUR KIDS

Like adults, children also have tax allowances that can be utilised each year. The Junior ISA allowance is now a very generous £9,000 a year, which enables you to start building a very healthy fund to help them transition into their adult lives. They won’t be able to access the money until they are 18, at which point it automatically turns into a normal ISA and transfers into their name, giving them full access.

If you’d prefer something longer term, you can pay up to £2,880 into a Junior SIPP each year, with Government tax relief automatically boosting that to £3,600. They won’t be able to access the money until they are at least age 57, maybe later if the Government increases the minimum retirement age.

This ensures there is plenty of time for them to benefit from compound investment returns. Either a Junior SIPP of a Junior ISA is a great way to encourage children into the savings habit, and using tax-efficient shelters, from an early age.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Act fast with Brunner to secure very cheap access to good stocks

- Stick with Yamana Gold despite falling share price

- Don't be tempted to take profit on Treatt following recent share price spike

- Good strategic process is helping to drive up shares in PZ Cussons

- Ford shares electrified and there could be more to come

- There is so much to like about ASOS as an investment

Investment Trusts

Money Matters

News

- Surge in amateur day traders suggests final stages of market bubble

- Terry Smith denies overexposure to highly valued tech firms

- Market excitement is building over electric vehicle growth

- Rolls-Royce under pressure after new setback

- Asian stock markets have raced ahead so far in 2021

- Companies may tap investors again for cash to survive the crisis