Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUS stocks as expensive as before the 1929 and dot-com crashes

We all know that financial markets are discounting mechanisms that look to ‘price in’ future events (and therefore trade off their perception of events rather than necessarily the reality of them).

However, it did look more than a little odd that the US stock market hit new all-time highs just as protestors were storming Capitol Hill to challenge the presidential election result, data highlighted how America was still piling up twin fiscal and trade deficits and the number of Covid cases continued to tick up inexorably.

This leaves investors to decide whether US equities are now overbought, overvalued and primed for a fall (or least some underperformance relative to other options) or capable of adding to a glittering run that dates back to end of the financial crisis in 2009.

BULL CASE

The bull case for US equities has three main planks. The roll-out of the vaccination programme will accelerate and further boost an official recovery rate of 97% among those Americans unlucky enough to catch Covid-19.

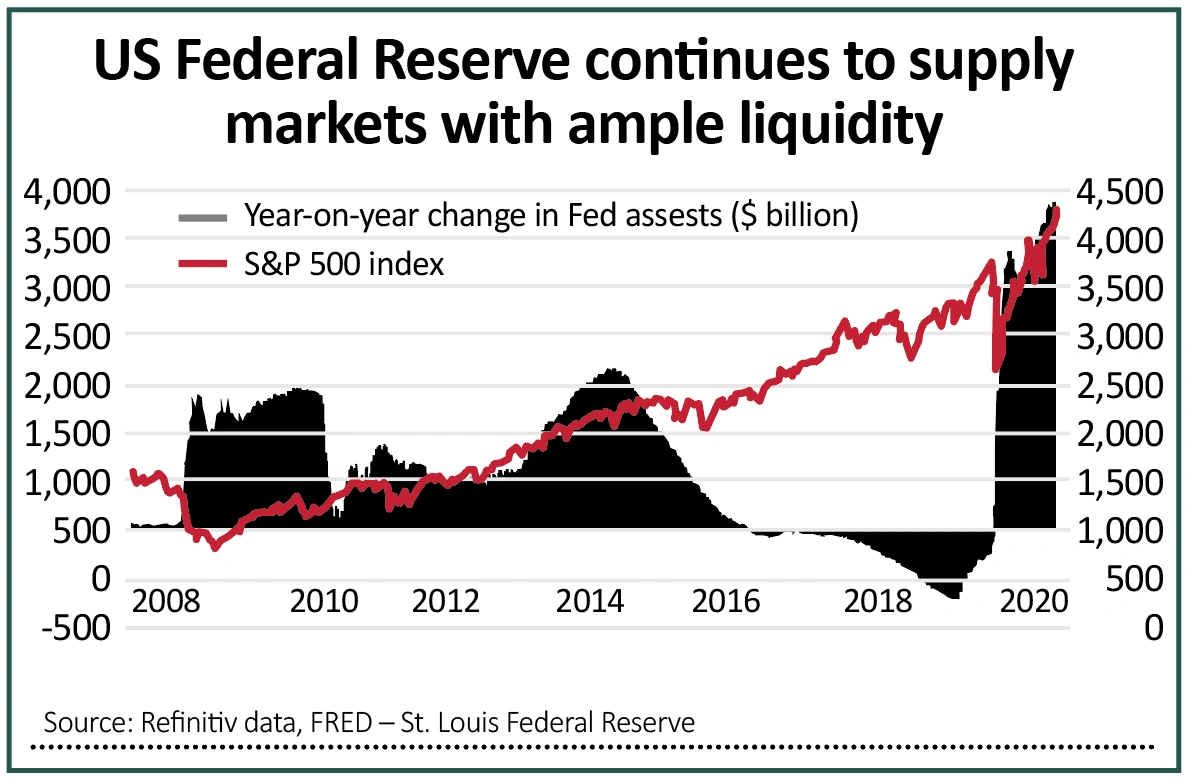

That will help in turn to unleash pent-up demand from consumers and corporations, stoking a strong economic upturn, especially as Government and the US Federal Reserve continue to offer strong fiscal and monetary stimulus.

The Fed is in no rush to raise rates until 2023 or even 2024, if you apply its requirement for a return to full employment and 2% trend inflation. The US central bank is still adding nearly $1.5 trillion a year to its quantitative easing (QE) scheme, too, and the financial asset prices do seem to be benefiting from this tidal wave of liquidity.

This is a good environment for equities, as corporate earnings, dividends and buyback activity will recover, and potentially a bad one for cash and bonds, especially as the Fed seems willing to let inflation run over and above its 2% target, at least for a while.

BEAR CASE

The counter arguments go as follows. There remains a risk that new strains challenge the vaccination programme and delay the recovery in both the US economy and corporate profits, which could also be affected by ongoing global trade tensions and tariffs.

Even if the economy and company earnings bounce back as hoped or expected, current analysts’ estimates factor a lot of that in already, especially as consensus forecasts already assume the earnings per share (EPS) for the S&P 500 index will exceed 2019’s pre-pandemic peak in 2021.

Even if analysts are right with EPS forecasts for the S&P 500 of $169.6 and $196.7 for 2021 and 2022 respectively, that still leaves US equities on 22.6 times and 19.5 times those forecasts, multiples which are lofty by historic standards.

The valuation implications of professor Robert Shiller’s cyclically adjusted cape earnings (CAPE) ratio are even more challenging.

Shiller’s work, which irons out the vagaries (and habitual optimism) of near-term analysts’ forecasts, puts US equities on a CAPE multiple of 33.7 times. The S&P 500 has only twice before traded at such elevated levels and they were 1929 and 2000, episodes which did not end well for investors.

THE RIDDLE(R)

Bulls of US equities will rebut the Shiller methodology on the grounds that the past is no guarantee for the future and that the CAPE ratio has been a poor timer of markets. Both arguments are valid.

But even if CAPE does not mean a crash is certain, the compound average returns over the following decade from past peaks have been undeniably poor.

The truth is that no-one knows what will derail US equities or when it will do so. All you can say is that it will happen eventually, whether the cause is an unexpected recession and earnings disappointment, inflation that forces interest rates higher and blocks the monetary spigot currently provides asset prices with a rising tide or (more likely) something that no-one is yet considering.

In terms of timing, some investors are already wondering whether American equities’ decade of dominance is coming to an end. As this column noted last week, emerging markets have outperformed US equities since autumn. Moreover, the key driver of US returns, tech and the FAANG stocks, have lagged their local market over the same time frame.

The mood music may therefore be changing, very subtly. As John Maynard Keynes said, markets can remain irrational for a lot longer than investors can stay liquid but once traditional valuation measures are cast aside then trouble generally lurks somewhere ahead, if only because multiples of earnings or cash flow provide insufficient downside protection.

As stock market historian Edward Chancellor wrote in his study of stock market bubbles Devil Take the Hindmost: ‘The most striking similarity between the 1920s and the 1990s bull markets is the notion that traditional measures of stock valuation had become obsolete.’

The same could be said of markets now. Those investors who wilfully ignore the CAPE crusaders must therefore do so in the clear knowledge that they are taking a sizeable risk to do so and be equally certain that future rewards will be sufficient compensation for their actions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Act fast with Brunner to secure very cheap access to good stocks

- Stick with Yamana Gold despite falling share price

- Don't be tempted to take profit on Treatt following recent share price spike

- Good strategic process is helping to drive up shares in PZ Cussons

- Ford shares electrified and there could be more to come

- There is so much to like about ASOS as an investment

Investment Trusts

Money Matters

News

- Surge in amateur day traders suggests final stages of market bubble

- Terry Smith denies overexposure to highly valued tech firms

- Market excitement is building over electric vehicle growth

- Rolls-Royce under pressure after new setback

- Asian stock markets have raced ahead so far in 2021

- Companies may tap investors again for cash to survive the crisis