Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStick with Yamana Gold despite falling share price

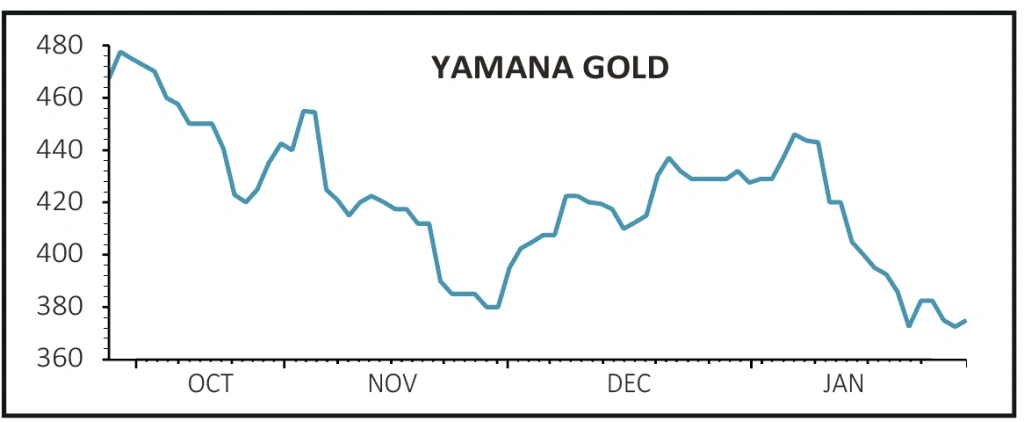

Yamana Gold (AUY) 374.9p

Loss to date: 18.5%

Original entry point: Buy at 460p, 22 October 2020

Gold miner Yamana Gold (AUY) has fallen 19% since we said to buy in October but we think it’s worth sticking with a company described by analysts as a ‘stable operator with plenty of upside’.

Gold miners can be leveraged plays on the gold price, and the firm’s falling share price reflects the 5% drop in the value of gold over the past few months as investor nervousness makes way for vaccine-induced optimism.

The company has proven itself to be a reliable operator and investor sentiment should change as it continues to demonstrate its strength. We also believe investor interest will return to gold miners as inflation expectations are rising. Gold is a natural hedge against inflation.

It produced 779,810 ounces of gold in 2020 and generated strong cash flows which has helped to significantly reduce net debt.

Yamana also has the long-term in mind, illustrated by its plan to increase output to 1 million ounces of gold a year through to 2030, underpinned by ‘continued operational success’ at its existing mines, which have consistently replaced mineral reserves above depletion.

The Canadian mining giant said it is ‘well-positioned to fund all exploration, expansions, projects and opportunities’ identified in its guidance and decade-long outlook using available cash and cash flow from operations.

SHARES SAYS: Yamana is a reliable operator with a strong plan for growth. Use the dip as a buying opportunity.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Act fast with Brunner to secure very cheap access to good stocks

- Stick with Yamana Gold despite falling share price

- Don't be tempted to take profit on Treatt following recent share price spike

- Good strategic process is helping to drive up shares in PZ Cussons

- Ford shares electrified and there could be more to come

- There is so much to like about ASOS as an investment

Investment Trusts

Money Matters

News

- Surge in amateur day traders suggests final stages of market bubble

- Terry Smith denies overexposure to highly valued tech firms

- Market excitement is building over electric vehicle growth

- Rolls-Royce under pressure after new setback

- Asian stock markets have raced ahead so far in 2021

- Companies may tap investors again for cash to survive the crisis