Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

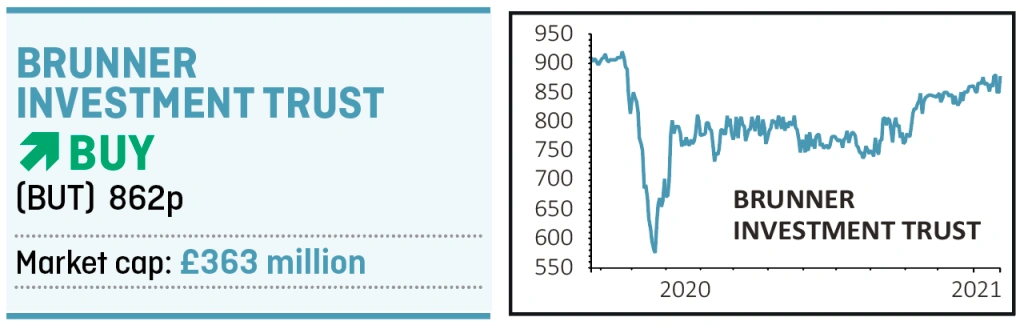

magazineAct fast with Brunner to secure very cheap access to good stocks

There is a lot to like about Brunner Investment Trust, not least the discount to net asset value (NAV) which has blown out to 16.3% from 9.4% in October 2020, according to Winterflood data.

Part of the reason is down to the actions of one of its largest shareholders, Aviva Global Investors. Data from Refinitiv shows that Aviva has been busy selling, nearly halving its position since November 2020. It still owns 9.9% but the discount has the potential to narrow once the overhang has run its course.

While Aviva’s selling has put pressure on Brunner’s share price, it does offer investors the chance to get heavily discounted exposure to some of the best quality companies in the world and a 2.4% dividend yield compared with 1.8% average for the peer group.

Managed by Matthew Tillett and Marcus Morris-Eyton, Brunner takes a more balanced view when searching for global opportunities rather than sticking to a pure value or growth style. Tillett focuses on finding reliable income while Morris-Eyton focuses on faster growth opportunities.

The portfolio isn’t skewed to either investment style, and it has faster growing companies trading on higher PE multiples as well as lower growth firms on cheaper multiples.

The common theme running through stock selection is quality with both managers looking to hold high quality companies with strong balance sheets and good cash generation.

The trust seeks out the best global opportunities for capital growth and reliable dividends, and gauges performance against a weighted benchmark composed of 70% of the FTSE World ex-UK index and 30% of the FTSE All-Share.

Over the last five years the net asset value and share price have gained 83% compared with 73% for the benchmark according to Refinitiv.

The trust is 46% exposed to the US, with Continental Europe comprising 28% and the UK at 18%. Asian companies comprise the rest of the portfolio.

The healthcare and industrial sectors account for around 20% each, with financials at 17% and technology at 13%, giving the portfolio decent exposure to ‘reflation’ prospects.

The largest holding is US software group Microsoft worth around 4.3% of the fund, followed by healthcare company UnitedHealth (3.8%), semiconductor company Taiwan Semiconductor (3.3%) and Swiss pharma group Roche (3%).

The trust has a very competitive 0.45% annual management charge and ongoing 0.66% charge which includes operational expenses.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Act fast with Brunner to secure very cheap access to good stocks

- Stick with Yamana Gold despite falling share price

- Don't be tempted to take profit on Treatt following recent share price spike

- Good strategic process is helping to drive up shares in PZ Cussons

- Ford shares electrified and there could be more to come

- There is so much to like about ASOS as an investment

Investment Trusts

Money Matters

News

- Surge in amateur day traders suggests final stages of market bubble

- Terry Smith denies overexposure to highly valued tech firms

- Market excitement is building over electric vehicle growth

- Rolls-Royce under pressure after new setback

- Asian stock markets have raced ahead so far in 2021

- Companies may tap investors again for cash to survive the crisis