Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMajor breakthrough for Netflix as it aims to be self-sustaining

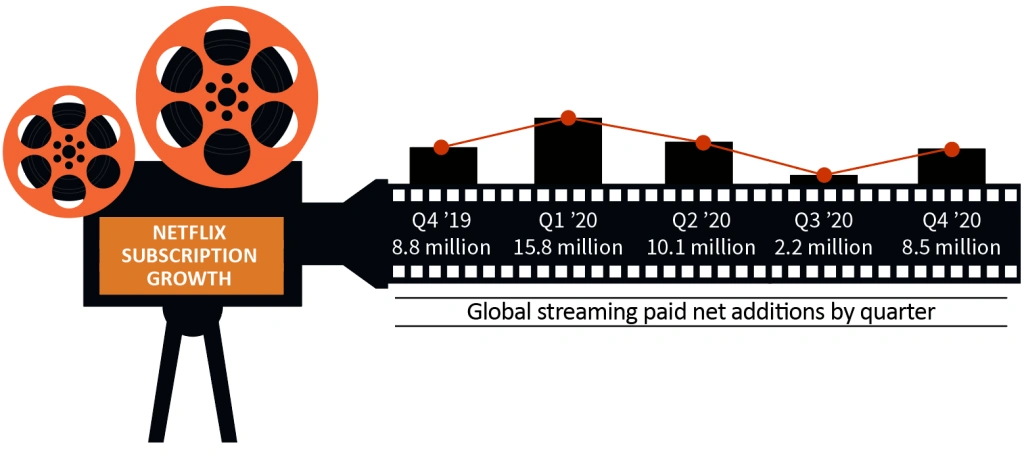

The short-term picture for Netflix is looking encouraging after it beat expectations with its fourth quarter subscriber numbers and signalled an end to its reliance on heavy borrowing. However, question marks remain over its longer-term prospects in a highly competitive streaming space.

The company passed the 200 million subscriber milestone as it added a better-than-forecast 8.5 million new paid subscriptions. Previously, third quarter subscriber numbers had disappointed, with the company suffering a lull after securing tens of millions of new users as the pandemic hit.

Like other streaming services, Netflix has been a beneficiary of people being stuck at home while cinemas and other entertainment venues have been closed.

This highlights a challenge for Netflix and its peer group, which is how to profit not just from adding subscriptions but also from viewers making more use of the platform.

Despite this challenge, management remain committed to the current model, rather than looking at areas such as premium content for which you pay extra. They also outlined their belief they can continue to grow the subscriber base despite already being 60% penetrated in North America.

Notably the fourth quarter announcement included guidance that the company will soon become free cash flow positive and Netflix even tentatively outlined plans to buy back shares. The former factor would reduce its reliance on external debt financing to sustain its heavy investment in new productions.

Helpfully many recently released productions appear to have hit the mark with viewers – notably the likes of The Crown, Bridgerton and The Queen’s Gambit.

However, rivals are also stepping up their spend on new content, in particular Disney which also has decades worth of its own creations to fall back on.

Independent media analyst Ian Whittaker commented: ‘While it stated it would be aggressive seeking out growth opportunities Netflix is essentially an operationally geared model (fixed cost of programming and the more subscribers you get, the higher the margins) and there is a natural limit on this.

‘It’s clear that Netflix does not intend to sit back and its comments about matching Disney at some point in family animation shows a willingness to take the fight to the enemy.

‘The key question is whether consumers keep multiple streaming services at a time when they are facing increasing economic pressure and strains on the household budget.’ [TS]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

- Experian reports reassuring growth

- Semiconductor cycle is turning to Micron’s advantage

- Polar Capital shares remain cheap despite high quality status

- Genus shares hit new record high after upgrading guidance again

- Knockout performance from Baillie Gifford US Growth

- Buy into Disney’s long-term dominance of the entertainment sector

Money Matters

News

- Major breakthrough for Netflix as it aims to be self-sustaining

- Three small cap new issues are currently flying high

- Investors buying IAG shares will have to pay new Spanish tax

- Shares in McDonald’s stall as challenges mount

- Shares in cruise operators start to rise as potential early vaccine beneficiaries

- High hopes for Bahamas Petroleum exploration well