Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe trends that will shape a continuing ESG boom in 2021

It feels as though 2020 was the year when ESG investing finally came of age. Expect more of the same in 2021, only more so.

Throughout the pandemic, whatever happened to share or bond prices, sustainable investing continued to grow as institutions and individuals allocated more and more funds to the sector.

A new cohort of younger, more eco-aware investors has emerged, demanding change, while companies are having to become more accountable and funds are no longer passive bystanders. Responsible and ‘positive change’ investing are the new normal.

Climate change and carbon reduction still dominate the agenda, but companies are now having to consider governance issues ranging from executive pay to diversity. New investment products are being launched every week, and existing products are being ‘greened’ in response to customer demand.

CLIMATE CONCERNS FIRST

Not unreasonably, given the more frequent occurrence of extreme weather events, the ‘E’ in ESG or, in other words, tackling emissions and climate change, is still the priority for investors and companies.

In 2016, global carbon emissions totalled 41 billion metric tons (gigatons). If left unchecked, at their current rate they could reach 60 gigatons by 2050 and cumulative CO2 emissions could reach more than 1,700 gigatons, putting us on a path to a five-degree increase in temperatures compared with pre-industrial levels.

Ongoing efficiency improvement and the growth of renewables could help lower emissions to 35 gigatons per year, according to McKinsey. That would still leave us with 1,300 gigatons of CO2 emissions by 2050 and the potential for global temperatures to rise three degrees versus pre-industrial levels.

Both trajectories are a long way from the 1.5 degree pathway which is needed to stave off ‘climate feedbacks’ such as the loss of arctic sea ice, loss of alpine glaciers, a collapse of the Greenland ice sheet, a collapse of the West Antarctic ice sheet, the dieback’ of tropical and boreal forests, and the collapse of ocean circulation patterns including El Niño, which in turn would create runaway global warming.

Tackling the problem needs every sector to decarbonize extensively and rapidly, from agriculture to industry, power generation to transport

A CHANGING INVESTOR BASE

According to funds network Calastone, the news in November 2020 of several vaccine breakthroughs prompted the biggest flow into active UK equity funds in five years and the second-biggest total inflow on record.

Out of a total of £2.3 billion, £1.6 billion of cash flowed into active funds and roughly £700 million into passive funds, the same level as the previous year. The £820 million of new capital investors added to the ESG category was more in a single month than in the entire five years to January 2020, and was more than double the monthly average of the year to date.

Meanwhile, research from Barclays suggests women and ‘Generation Z’ are the new stock market players investing with savings made in lockdown. Both groups put ESG towards the top of their investing criteria.

The encouraging performance of ESG funds during this period of extreme market volatility ‘may mark its turning point for overwhelming adoption across investors’ says Barclays.

Clearly there are positive market tailwinds for specialist asset managers such as Impax Asset Management (IPX:AIM) and Gresham House (GHE:AIM).

PRESSURE ON FIRMS RISING

Pressure is growing on firms, not just from outside investors but also from the inside, to incorporate ESG criteria into their internal processes as well as to become ‘greener’.

A survey of global firms by consultancy Willis Towers Watson found four out of five believe ESG is ‘a key contributor to stronger financial performance’ and are even planning to incorporate ESG into their executive incentive plans.

‘With investor and shareholder interest in ESG and sustainable investing increasing, companies are accelerating their focus on ESG initiatives’, says Shai Ganu, global head of executive compensation at Willis Towers Watson.

The decision by Germany’s Deutsche Bank to link senior executive pay to sustainability targets from next year sends a powerful message in this regard.

However, half the firms surveyed admitted they struggled with setting targets and measuring their ESG performance. This is a clear area of opportunity for firms such as MJ Hudson (MJH:AIM) and Inspired Energy (INSE:AIM).

The rise of the green bonds

According to credit research firm Moody’s sustainable bond issuance increased 65% between April and June compared with the first quarter.

Social and sustainability bond issuance has been increasing rapidly this year and Moody’s says this is because the pandemic has increased investors and companies’ sensitivity to ESG issues.

The global market for green, sustainability and socially responsible bonds is worth more than $1.5 trillion.

Fund manager Tom Chinery who manages Aviva Investors’ stewardship funds told Shares that engagement from credit managers with company executives had increased and was part of them fulfilling their stewardship responsibilities.

Chinery prefers to focus on sustainability bonds which are linked to specific projects and KPI’s (key performance indicators) which outline projects designed to reduce environmental impact.

One example is logistics property company Tritax Big Box (BBOX) which issued the first UK real estate investment trust (REIT) green bond in November.

What attracted Chinery to the bond is that it is linked to specific projects aimed at constructing net zero carbon buildings with third-party observers tasked with monitoring the progress against pre-determined targets and making sure the company adheres to meeting them.

Another example is Italian utility company ENEL which has issued sustainability bonds which will fund investments designed to treble renewable capacity and reduce carbon emissions.

Interestingly Chinery benchmarks himself against traditional indices because he believes that ethical investing will outperform over the long term.

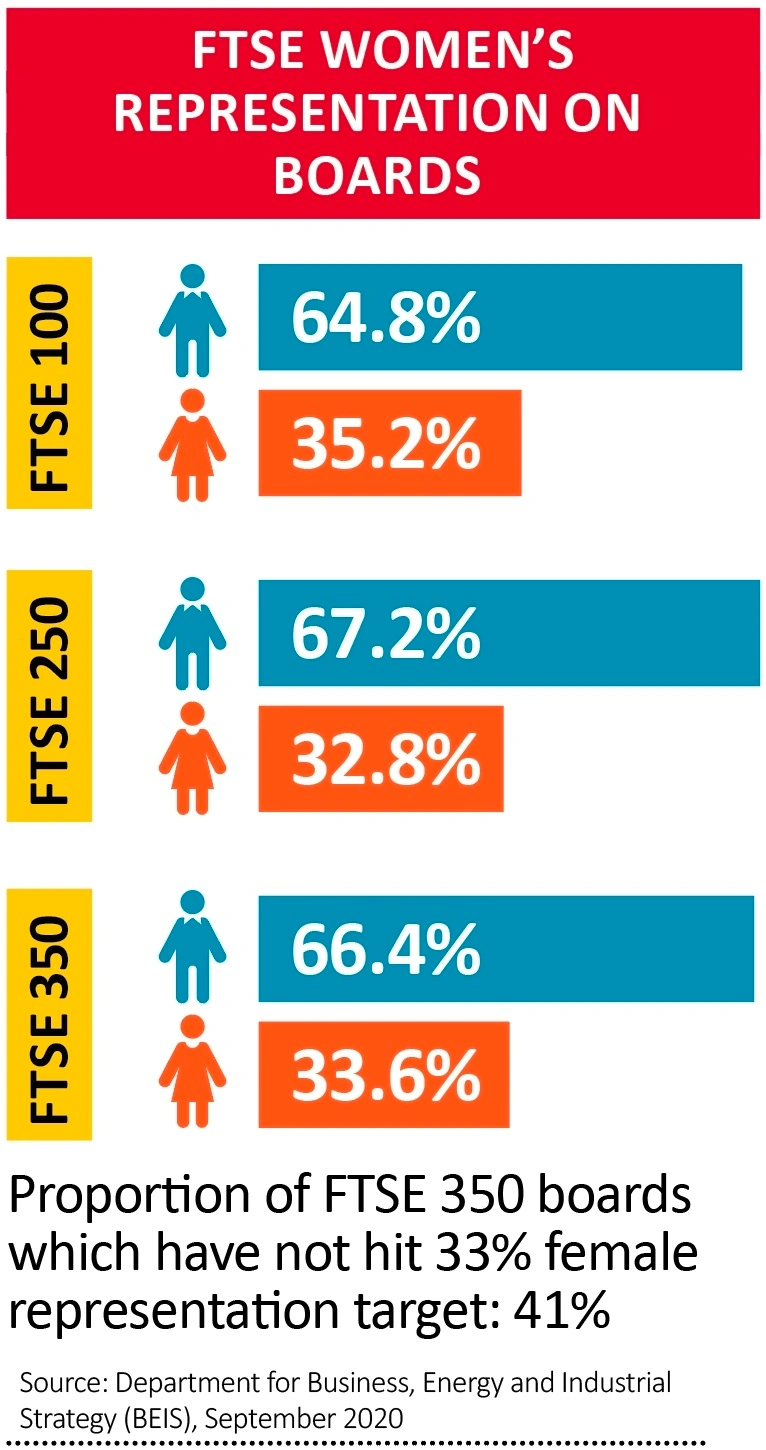

DIVERSITY MATTERS

If anything, ESG criteria are getting tougher, with large asset managers making increasing demands of companies. Investment bank Federated Hermes’ ‘stewardship’ team has promised to get tough on firms with little to no ethnic diversity on their board of directors.

The firm wrote to FTSE 100 companies saying it would recommend clients vote against the chair of a board that ‘does not have at least one director from an ethnic minority background and has no credible plan to rapidly achieve this’, in line with the Parker review.

It also said it could recommend clients vote against the chairs of FTSE 350 companies which failed to fulfil the 33% level of female board representation suggested by the Hampton-Alexander review.

GREEN ‘RE-BRANDS’

After its latest ‘pulse’ survey found 90% of respondents thought pension schemes should offer more ESG investments, US fund behemoth BlackRock has re-jigged the strategy of its flagship £6 billion ‘LifePath’ defined contribution product to ramp up exposure to ESG instruments to more than 50% ‘as a core driver of long-term sustainable returns’.

In a similar vein, US fund house State Street has added an ESG screen to some £21bn of assets in UK-domiciled equity and debt index funds in response to growing demand from investors.

The screen is ‘exclusionary’ and will avoid companies in violation of the UN Global Compact principles, meaning holdings such as weapons manufacturers will be eliminated.

Maria Nazarova-Doyle, head of pension investments at partner firm Scottish Widows, commented: ‘We believe divestment could be a powerful ESG risk mitigation tool for passive strategies. Investing responsibly will help to build a better future for everyone.’

ADDRESSING INEQUALITY

Finally, the social aspect of ESG investing has typically been the hardest to pin down, but the coronavirus pandemic has highlighted huge inequalities in global wealth and social injustice.

Analysts at ratings firm MSCI say many companies have responded to this conversation by addressing the race, gender and social divides in their workforces. However, ‘similar to greenwashing, the idea of ‘social washing’ needs to be watched closely’ they point out.

We can expect more companies to launch ‘social bonds’ and directly finance social impact programmes in 2021 as a way of staking a claim to being ESG champions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Stock pick for 2021: Alibaba

- Stock pick for 2021: Tracsis

- Stock pick for 2021: Eurofins Scientific

- Stock pick for 2021: JD Wetherspoon

- Stock pick for 2021: BHP

- Stock pick for 2021: Inspecs

- Stock pick for 2021: Convatec

- Stock pick for 2021: RWS

- Stock pick for 2021: PZ Cussons

- Stock pick for 2021: Diageo

- Stock pick for 2021: Qinetiq

- Stock pick for 2021: Ocado