Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTop stocks for 2021

Alibaba

China offers huge growth potential in 2021 and beyond and Alibaba (BABA:NYSE) is arguably the best way to play this theme.

The country’s answer to Amazon, Alibaba owns the largest online marketplaces in China while Alibaba Cloud is the region’s leading cloud platform. The company went public six years ago, and its share price has since risen nearly 300%.

Ambitious plans, which include doubling the active users of its digital ecosystem to 2 billion by 2036, are being driven by savvy digital vertical investments into areas like smart logistics, payment services, cloud computing, online marketing services, travel booking, music and video streaming.

Where Amazon subsidises its online marketplace with its very profitable cloud business AWS, the opposite is true of Alibaba. Its top Chinese marketplaces, Taobao and Tmall, do not take on any inventories. Instead, they act as paid listing platforms that link buyers to sellers, with its logistics unit Cainiao fulfilling orders.

This less capital-intensive approach keeps Alibaba’s core commerce business very profitable and allows it to fund its currently unprofitable cloud, digital media, and entertainment and innovation initiatives units.

Competition in China’s cloud computing space is tough, but Alibaba already has an estimated 50% market share, which should make its journey to similar profit margins to Amazon’s 30%-odd a big lever for future growth.

In short, Alibaba is valued at less than half of Amazon despite producing substantially wider margins, greater profitability on a group basis, and having a more extensive sales growth outlook for the next couple of years.

In the six months to 30 September 2020, Alibaba’s revenue grew 32% year-on-year and its adjusted earnings rose 28%. Analysts expect Alibaba’s revenue and earnings to increase 38% and 32% this year respectively as its growth is forecast to improve in the second-half period.

It is important to note that Alibaba faces growing online competition in China from the likes of JD.com and Pinduoduo.

Alibaba’s shares recently wobbled when the stock market listing of its part-owned Ant Group was temporarily halted by Chinese regulators as they looked to implement tougher rules on fintech firms.

There are also US threats to delist Chinese firms from Wall Street as part of a compliance clampdown, however these look largely political.

Investors need to be comfortable with these risks to buy the shares.

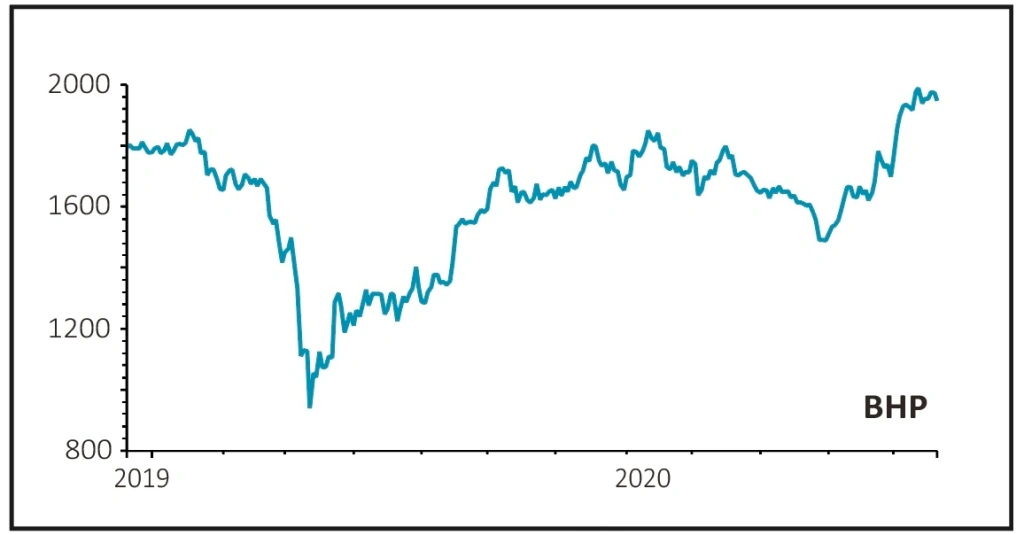

BHP

If 2021 is the year of global economic recovery, then one of the best placed stocks to capture that upside could be FTSE 100 miner BHP (BHP).

The £98 billion market cap company is one of the world’s biggest producers of iron ore and copper, two metals considered to be economic bellwethers.

Iron ore prices surged in December and reached their highest level in seven years as demand soars from China, a big market for BHP, and the benefits of which should start to be felt when the firm reports its half-year results to 31 December in February 2021.

BHP can dig iron ore out of the ground for less than $15 per tonne and is able to sell it for a whole lot more given prices in the past month have gone as high as $161 per tonne, and are forecast to remain at an elevated $123 per tonne well into the first half of 2021.

Bumper profits could also see BHP pay a decent dividend, particularly given the firm’s history of returning cash to shareholders, with the company forecast to increase its total shareholder payout to $1.49 per share in 2022 according to Refinitiv, equivalent to a 5.7% yield.

Longer term BHP is well-placed to benefit from the structural growth of electric vehicles (EVs) due to its exposure to copper and nickel, two metals key for EV components.

Nickel is expected to have a breakout year in 2021, and nickel futures are already starting to trade higher in anticipation of stronger demand.

BHP’s much-hyped Nickel West processing plant has been beset by delays having meant to be fully up and running this year and has therefore been loss-making for the firm. It is expected to start producing by the second half of next year.

This underscores some of the risks with miners, as operational problems can affect their production and impact earnings, while it’s also important to note none have pricing power as all of their income depends on the market prices for the commodities they are digging out of the ground.

The likes of Anglo American (AAL), Glencore (GLEN) and Rio Tinto (RIO) also have exposure to similar areas to BHP, but they either have a poorer commodity mix – with lower exposure to either iron ore, copper or nickel – or worse ESG credentials, something which looks more likely to weigh on share prices going forward, particularly in sectors which have big impacts on their environments like mining.

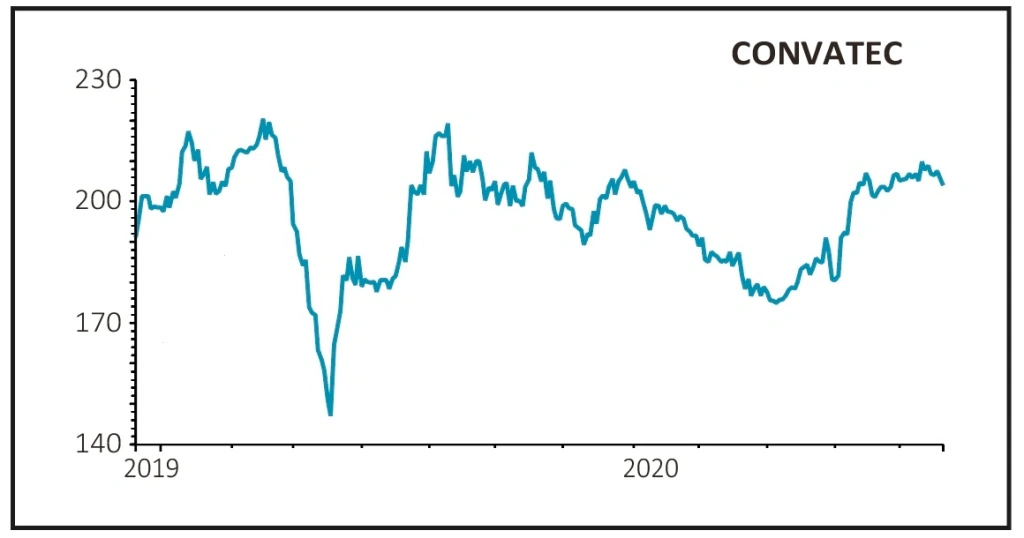

Convatec

After recently upgrading (28 October) full-year revenue growth to the top of its 2% to 3.5% target range, medical products company ConvaTec (CTEC) looks well placed going into 2021 as several tailwinds form.

A faster than anticipated recovery in US elective surgeries is providing a boost for its wound care business and new product launches position the company for renewed growth.

While Covid-19 still presents a challenge especially in the US where caseloads are still rising, the stars appear to be aligning for stronger than anticipated revenue growth translating into higher profit growth.

Before the pandemic management was confident 2020 would mark the trough year for margins. A temporary improvement this year from lower travel and other operating expenses, and a deferral of some investment in the ‘transformation programme’ has muddied the picture.

However, there remains the tantalising prospect that ConvaTec is on the cusp of entering a new phase of profitable growth, allowing the shares to claw back some of their sector valuation discount.

ConvaTec operates in attractive markets with structural growth drivers related to ageing populations. Its products serve patients with chronic and progressive diseases where there are few cures.

Of the four niches in which ConvaTec operates the insulin pump market for diabetes sufferers is expected to have the fastest growth potential at around 9% a year to 2023.

The company has market-leading solutions including a ‘smart glycaemic control’ which provides continuous monitoring of blood sugar levels of patients, a key advantage. In the third quarter the infusion segment saw particularly strong revenue growth of 27%.

The global ostomy market is expected to grow at 4.7% a year out to 2026 according to consultancy Coherent Market Insights. Ostomy involves the provision of prosthetic medical devices for the collection of waste in patients with diseases of the digestive system such as Crohn’s.

Continence and critical care and global wound care markets are expected to grow at 4.6% a year to 2026.

ConvaTec had by management’s own admission fallen behind competitors in wound care and ostomy but has since rectified the situation by introducing new products and better marketing.

The pandemic has created uncertainty around the timing of the inflexion point for ConvaTec to return to profitable growth, but the performance during the past year points to increasing momentum across the business.

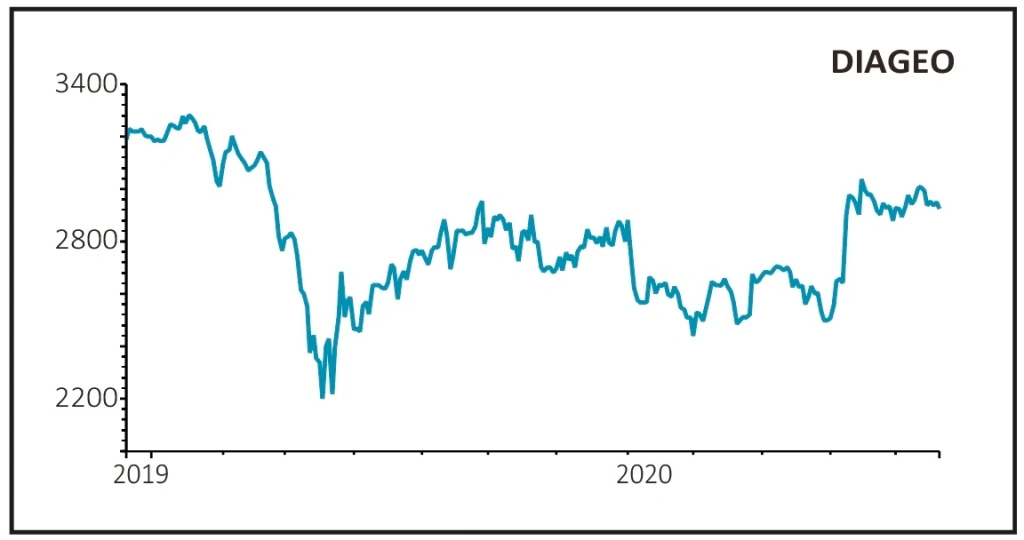

Diageo

Quality business Diageo (DGE) should benefit from a reopening of society and we think its shares will reward investors handsomely in 2021.

Diageo and the wider beverages space have underperformed a relatively buoyant wider consumer staples piece in 2020 as they have suffered from Covid’s substantial impact on sales in pubs, restaurants, hotels and at events.

We think Diageo will play catch-up in the coming months as hospitality reopens and with supermarket and convenience store sales likely to remain resilient. The market focus will soon turn to the 2022 financial year which starts in July 2021, where forecasts suggest earnings will largely recover to pre-Covid levels.

While it may be familiar to some for making Guinness, Diageo is principally a manufacturer of spirits. In the 2020 financial year upwards of 70% of its sales came from rum, scotch, vodka, whisky, gin, liqueurs, gin or tequila.

The spirits industry has several attractive qualities for a dominant player like Diageo. Consumption is steadily rising in the West and in emerging markets, manufacturing costs are relatively low, it is sold at a premium price and, crucially, brand power counts.

People will typically have a favourite brand of rum, gin, vodka or whisky. Fortunately for Diageo its roster of brands includes many people’s favourites – names like Johnnie Walker, Smirnoff, Baileys, Captain Morgan and Tanqueray.

Diageo certainly felt an impact from coronavirus, and it had to flex its balance sheet to cope with the crisis. As a result, its net debt to EBITDA (earnings before interest, tax, depreciation and amortisation) ratio was running above its three times target at the last count.

However, we see little sign that the business is in financial distress. The dividend was hiked 2% at the half-year stage even if share buybacks were paused.

The company recently demonstrated its commitment to targeted acquisitions to refresh its portfolio by agreeing to buy Aviation American Gin, backed by actor Ryan Reynolds, in a deal worth up to $610 million.

As fund manager Nick Train, a holder of Diageo, observed: ‘It is a reassuring sign that boards aren’t just in fire-fighting mode and that balance sheets and liquidity are in good enough shape to make investments for the future.

‘As others have remarked, the deal is reminiscent of its acquisition of George Clooney-sponsored Casamigos in 2017. A transaction that raised eyebrows at the time, including ours – because of the headline cost. But a deal that looks smarter and smarter as the US spirits boom continues, with premium brands leading the way.’

Eurofins Scientific

Paris-listed Eurofins Scientific (ERF:EPA) is the world leader in food, biopharmaceutical and cosmetics product testing and environmental laboratory services. It employs over 48,000 people in more than 800 laboratories across 50 countries.

Roughly half of annual turnover comes from food and biopharmaceutical product testing and services, businesses which are set to grow due to ageing populations and increasing regulation.

Eurofins’ laboratory network was well placed to assist the global effort in tackling the Covid pandemic and drawing on its experience of SARS it rapidly developed testing services, solutions and products to support over 20 million patients per month.

While this generated revenues for the group, some of its core businesses experienced a drop over the summer due to the global slowdown, although by June the firm was already beginning to see a sharp recovery in demand.

Commenting on the half-year results, which saw sales rise by 7.4% to €1.18 billion and pre-tax profit rise by 28.4% to €264 million, chief executive Gilles Martin said that had the pandemic not occurred the firm’s performance would have been better. Even where sales hadn’t quite got back to pre-Covid levels, cost cuts meant profitability was higher as demonstrated by the faster growth of earnings.

The positive news on the Pfizer/BioNTech vaccine sent Eurofins’ shares down 8% on the day, and they continue to languish at the levels they saw in the summer even though analysts and the company weren’t factoring in much revenues from testing beyond next year.

The firm has typically generated a 10% or greater return on capital employed, partly thanks to small bolt-on deals in niche, high value-added areas.

With its two latest acquisitions it became the leading genetic analysis firm in Japan and the market leader in environmental testing in Taiwan, increasing its global footprint in genomic services, diagnostics and agroscience.

The company forecasts sales growing at a 5% organic rate per year from this year to 2022 and beyond, supplemented by acquisitions, while analysts at Berenberg believe it has significant under-used lab capacity and see strong operational gearing and margin improvement being the next drivers of the growth story.

Rapid growth in free cash flow is expected to reduce gearing to less than two times EBITDA, while the firm’s investment-grade rating and clear ESG credentials mean it should enjoy above-average governance ratings.

Despite its appeal, Eurofins trades at a significant discount to its peers including Intertek (ITRK) and Switzerland’s SGS.

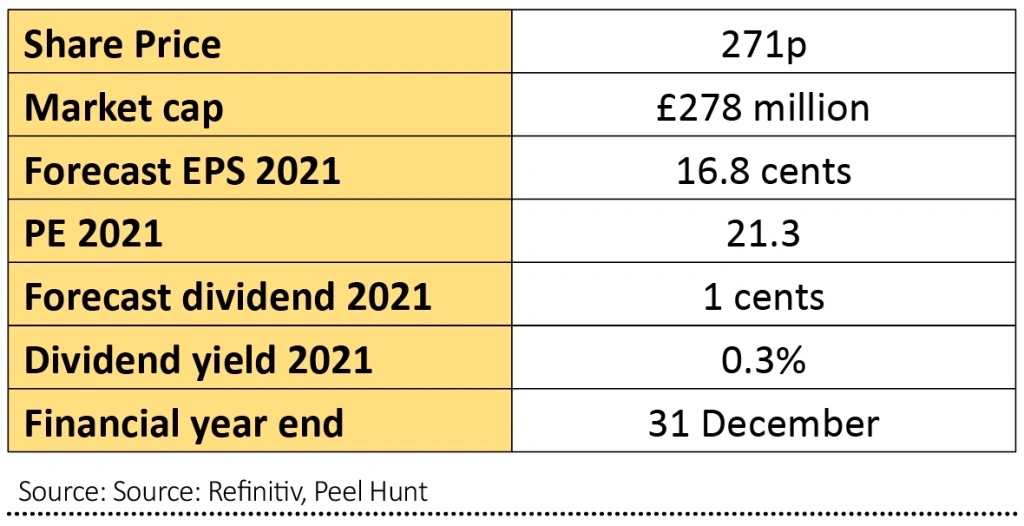

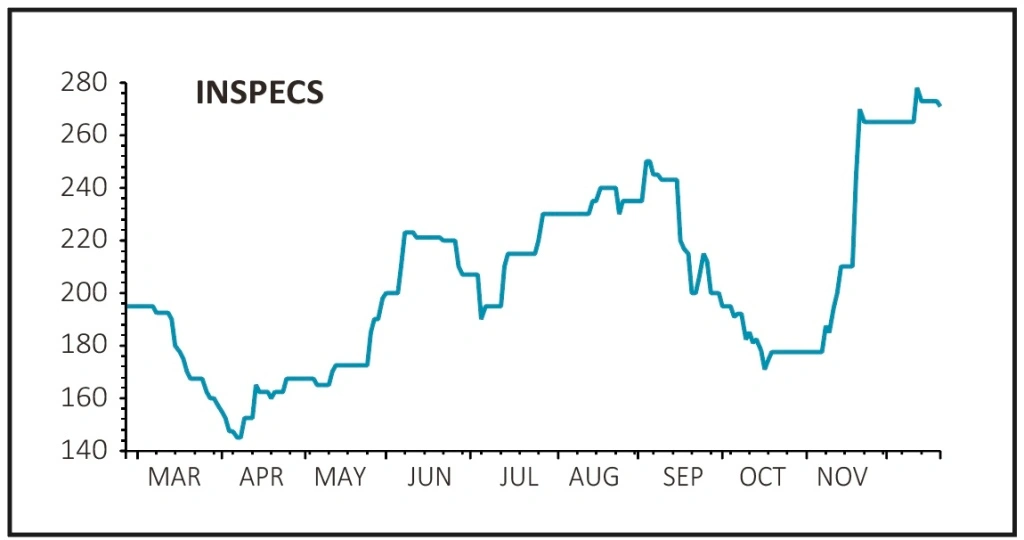

Inspecs

Eyewear frames and optically advanced spectacle lenses maker Inspecs (SPEC:AIM) joined the stock market in February 2020 and its shares have since risen by 40%. We see a lot more upside at the Bath-based company which is still in the early stages of its global growth journey.

The eyewear industry has bounced back from Covid-enforced closures with opticians operating safely, Inspecs’ end-October order book was 25% above that of 2019, while the recent acquisition of Germany’s Eschenbach provides a further platform for growth.

Guided by founder and chief executive Robin Totterman, Inspecs’ broad range of frames covers optical, sunglasses and safety and are either branded or private label. July’s purchase of lens maker Norville from the administrators also significantly increased Inspecs’ lens expertise and manufacturing capability.

Vertically integrated and with factories in Vietnam, China and Italy, Inspecs is one of few companies that can offer a one-stop-shop solution to global retail chains. This leaves it well positioned to continue taking market share in the expanding international eyewear market. Customers include global optical and non-optical retailers, global distributors and independent opticians.

Key brands produced under licence include Superdry (SDRY), O’Neill, Caterpillar and Radley, while major customers include opticians such as Specsavers, Boots, Vision Express and National Vision, as well as retailers such as WalMart, ASOS (ASC:AIM) and TK Maxx.

Broker Peel Hunt upgraded its earnings estimates following the recent acquisition of German-headquartered eyewear supplier Eschenbach, a deal which dramatically increases Inspecs’ global distribution.

Greater scale is expected to yield opportunities to acquire bigger global licences and make acquisitions to increase the enlarged group’s brand portfolio.

Enhancing Inspecs’ presence in key eyewear markets including Germany, the US and France, Eschenbach also gives the new owner a presence in the independent opticians channel, complementing its existing focus on retail chains.

And whereas Inspecs is currently focused on more affordable eyewear, Eschenbach takes the business into the premium and luxury segment. As if that weren’t enough, Eschenbach’s Optics division provides Inspecs with an entry into the low vision technology market, which serves people with severe visual impairment.

Peel Hunt’s updated forecasts point to a jump in sales from 2020’s estimated $45 million to $241 million in 2021, sending adjusted pre-tax profit up from $3.6 million to $19.5 million next year, ahead of an estimated $24.9 million of profit from $256.5 million of sales in 2022.

We think those forecasts will look conservative given the upside to come from purchasing, operational and revenue synergies post-Eschenbach.

Income-seekers should also note the broker sees Inspecs initiating a dividend next year.

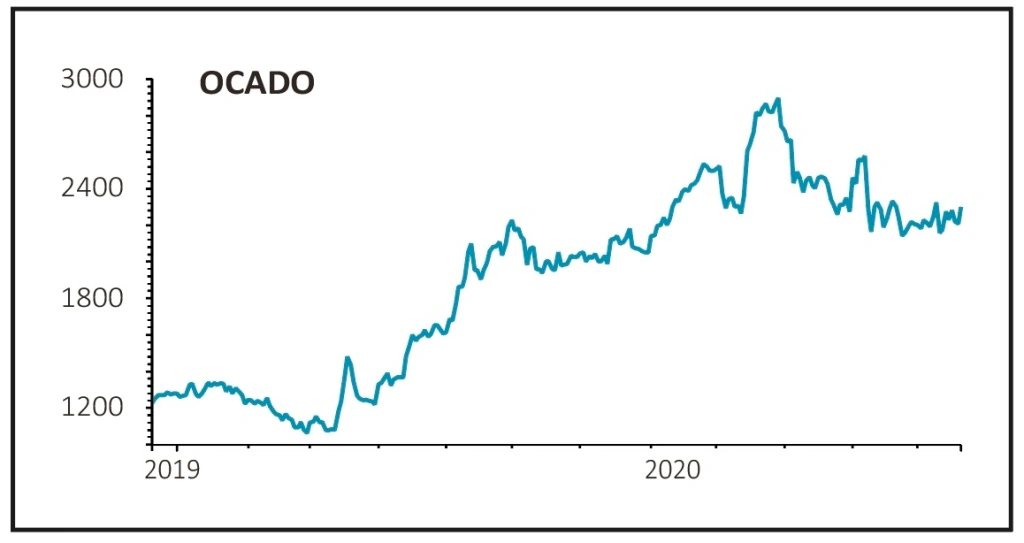

Ocado

Very few UK stocks are targeting global domination but that is the ambition driving the Ocado (OCDO) story.

The Covid-19 pandemic has shifted the market in its favour, with a significant jump in people around the world shopping for groceries online. This behaviour is likely to accelerate investment by supermarkets in their online fulfilment capabilities.

A joint venture with Marks & Spencer (MKS) provides a nice income stream to Ocado but the latter is fundamentally a robotics and automation business rather than a delivery company.

It licences systems to grocery companies to power their fulfilment centres, essentially large warehouses where a lot of the picking is done by robots.

To date Ocado has signed up seven supermarkets outside the UK as partners including names in the US and Japan, where growth opportunities are massive. Two partners, Sobeys in Canada and Casino in France, now have operational centres.

In the US, Kroger will launch its first centre using Ocado technology in 2021 and has big plans to add more automated warehouses. It is also paying Ocado to improve the efficiency of picking goods in-store for click and collect orders.

Ocado typically incurs £20 million to £30 million cost for the technology hardware and software for each warehouse, while each supermarket partner pays for construction of the property. Ocado gets a cut of sales from each warehouse.

In August, broker Peel Hunt said: ‘Ocado’s deals to date add up to £210 billion in gross sales, which is 7.5% of its £2.8 trillion key markets. Ocado believes it could hit 25% market share, as the market leader, and over time 75% to 80% could go online. As it takes a 5% fee as its revenue, this turns into an annual revenue stream of £26 billion+.’

Future initiatives could see Ocado play a role with robotic preparation of ready meals or salads and it has invested in a business involved in vertical farming, which is shelving to grow herbs, salad, fruit and vegetables. That could see fresh produce grown next door to a supermarket.

The company is not forecast to make a profit in the next two years as it will take time to get partners’ operations up and running. As such, investing in Ocado means taking a longer-term view of the opportunity.

Risks include competition, although Ocado is off to a strong start in its bid to be a market leader, and legal action being pursued by Norway’s AutoStore over robot technology patents. Ocado has issued a strong rebuttal but it’s worth monitoring the situation.

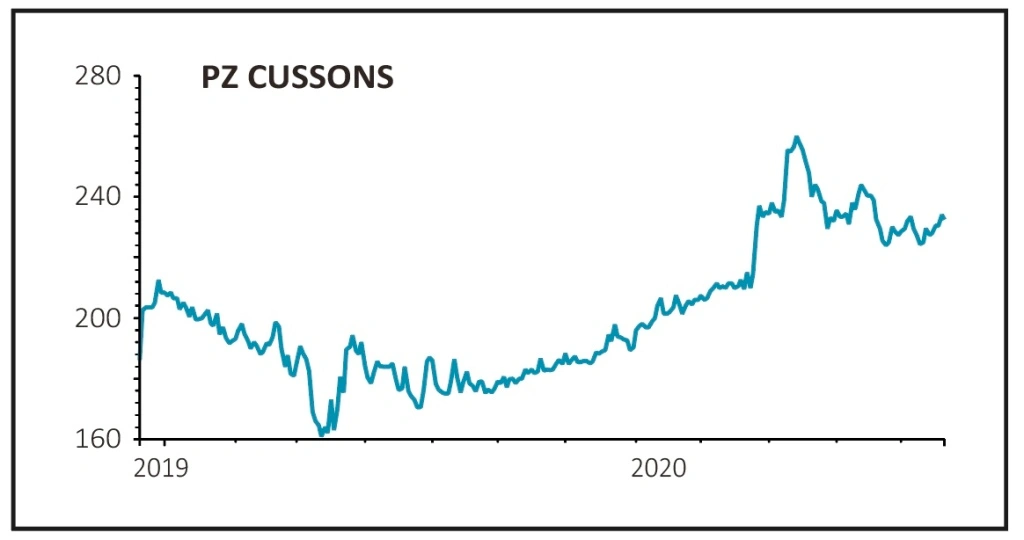

PZ Cussons

Risk-tolerant investors should follow respected fund manager Nick Train into PZ Cussons (PZC), the branded consumer goods group embarking on a multi-year turnaround under new chief executive Jonathan Myers.

Admittedly, the company’s profits have disappointed in the past, but there is extraordinary value in its portfolio of personal care, home care and beauty brands which Myers can unlock with the help of finance director Sarah Pollard, a new recruit from Nomad Foods.

Shares believes a refocus behind PZ Cussons’ strongest brands in key markets can boost sales growth, while a simplification of the business is eliminating unnecessary costs, actions which should eventually narrow a wide price to earnings discount to the group’s European home and personal care peers.

Discerning investor Nick Train backs companies that own beloved or essential consumer brands such as PZ Cussons, held in his Finsbury Growth & Income Trust (FGT).

PZ Cussons’ enviable portfolio of personal care and beauty brands includes Carex, the UK’s number one hand wash brand; Imperial Leather soap-to-shower gel; and tanning brand St Tropez.

Train believes owners of trusted brands can not only negotiate but harness digital disruption, giving us added confidence that Myers’ turnaround strategy can pay off.

He has already set about streamlining and focusing the business following an initial review, which helped PZ Cussons deliver 19% first quarter sales growth in combination with a Covid-driven boost in demand for its hand hygiene wares.

Conducted to account for pandemic-induced changes in consumer behaviour, the results of a further review, including Myers’ strategy to deliver sustainable revenue growth and improved margins, will accompany the half-year results on 26 January, potentially acting as a positive near-term catalyst for the share price.

Over the long term, we see scope for strong growth driven by a return to profitability in Africa, increased investment behind the company’s prized portfolio of brands and sharper execution under Myers’ leadership.

Encouragingly, the first quarter update highlighted ‘excellent’ performances in the UK and Indonesia, as well as recovery in the beauty business, Australia and Nigeria, the key Africa market that has long proved a trouble spot for PZ Cussons, yet boasts dramatic long-term potential for consumer goods brands.

Liquidity is strong and net debt is coming down at PZ Cussons, de-risking the investment case. Numis’ current estimates for the year to May 2021 suggest that PZ Cussons will deliver improved pre-tax profit of £63.7 million (2020: £62 million), ahead of £72.7 million in 2022.

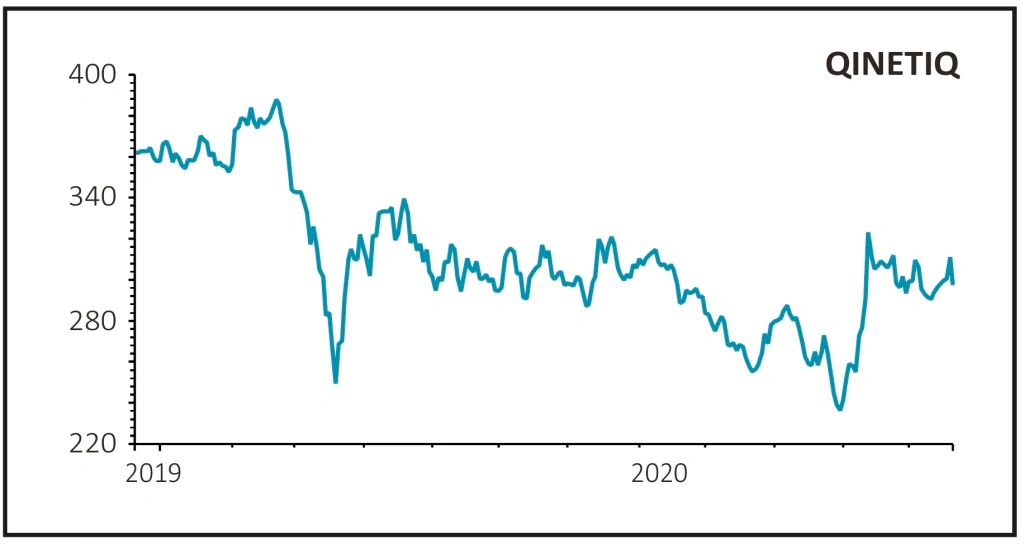

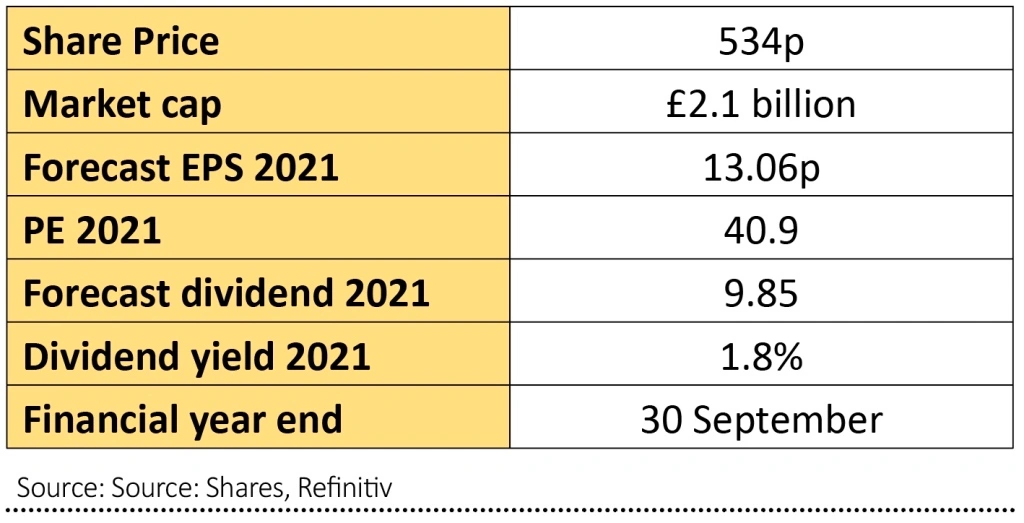

Qinetiq

Strong revenue gains delivered by QinetiQ’s (QQ.) international business is underappreciated by investors and will continue to drive double digit growth. At some point the market will wake up and value the business on a higher rating.

Defence, cyber security, evaluation and testing company QinetiQ initiated a new growth strategy four years ago to increase the proportion of international sales from 20% to half of the business.

Impressively, international revenues have grown at a compound annual growth rate of 30% a year over four years to reach £213 million, reaching 35% of total revenues.

In the recent first-half update (12 Nov) QinetiQ raised full-year guidance for operating profit to be above £130 million and reinstated medium-term targets for revenue growth in low double-digits and an operating margin in the 12% to 13% range. Analysts have been upgrading their estimates for full year profits.

The company has diversified into faster growing niches by acquisition such as advanced sensory solutions through the purchase of US-based MTEQ and data analytics through the acquisition of Naimuri. MTEQ provides unmanned robotic bomb disposal devices for the US army.

QinetiQ has 30% market share of the UK’s testing and evaluation of military equipment as well as training through a long-term Ministry of Defence (MOD) contract. Management has identified a global market opportunity for its services worth around £8 billion.

The company was formed in 2001 when the MOD split is Defence Evaluation and Research Agency (DERA) into two parts. The larger part including most of the non-nuclear testing evaluation businesses was rebranded QinetiQ, which is derived from kinetic, a scientific word for motion.

In 2003 the company signed a 25-year long-term partnering agreement under which it supplies the MOD with innovative testing and evaluation of military and civil platforms and weapons for land, sea and air. Essentially QinetiQ makes sure equipment works as intended and provides training which sometimes includes simulated battle exercise.

Around 75% of revenues are derived from assurance, evaluation and training with the rest coming from building products.

Critics can justifiably point to earnings growth lagging revenue growth. This will normalise as past investments translate in faster profits growth.

It is a high-quality business with most work delivered on long-term contracts which provide high visibility on revenues as well as good cash generation.

We believe investors have yet to appreciate the growth opportunity and consistent management execution of the strategy.

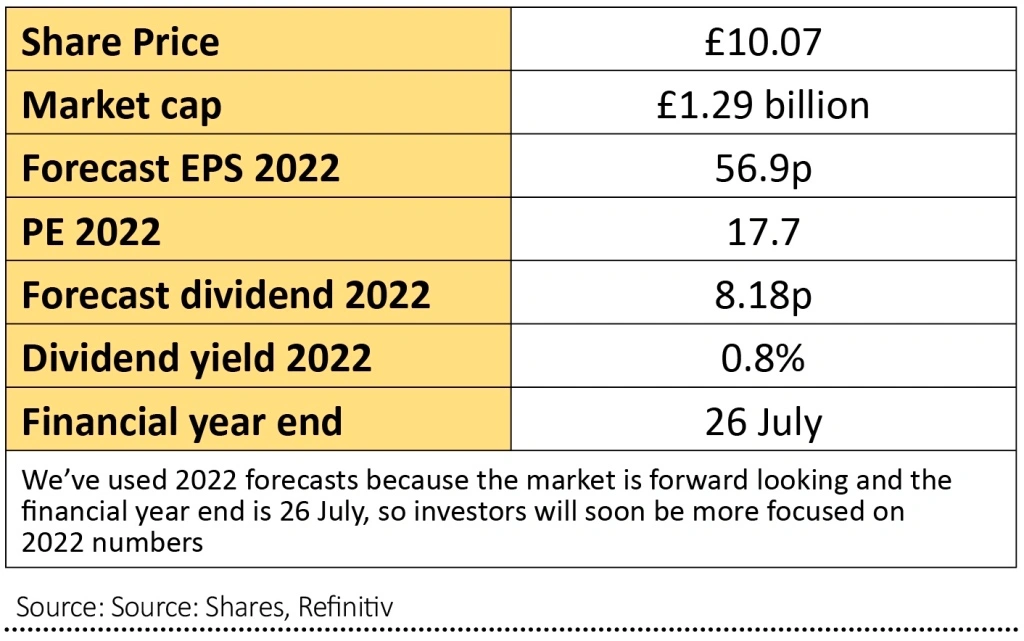

RWS

RWS (RWS:AIM) is the world’s leading provider of language services and language technology to firms in sectors such as technology, pharmaceuticals, medical equipment, telecoms and chemicals.

The recent acquisition of SDL marks a step change for the business with significant opportunities to grow, and the cost synergies from combining the businesses could be much greater than guided by RWS.

Before the SDL deal, half of RWS’s sales came from RWS Moravia, which works with technology companies such as Facebook to make sure their content, websites and apps are tailored to each geography and to ensure brand consistency.

Revenues in the year to 30 September rose 5% to £174 million driven by strong sales to its technology customers at the start of lockdown and increased demand from online sales platforms, web services and financial services clients.

A third of group revenue in the year came from IP Services, which provides patent translations and filing solutions as well as a range of intellectual property search services.

The third business is Life Sciences, which provides technical translations and linguistic validation to large pharmaceutical companies, clinical research organisations and medical equipment manufacturers.

Revenues were up 6% in the year to a record £69 million thanks to strong growth in Covid-related clinical trials, translation work for vaccines and anti-virals, and antibody testing equipment.

In November RWS completed the £854 million acquisition of UK rival SDL, cementing its position as the world’s largest language services and technology group with 90 of the top 100 brands by value, all of the top 10 pharmaceutical firms, most of the major West Coast technology businesses and half of the top 20 patent filers worldwide.

Chief executive Richard Thompson told Shares that even though the deal was only weeks old, his team had already identified annual synergies above the £15 million initially predicted.

The group’s new targets will be outlined in April, but RWS management expects the combination to generate double-digit earnings per share (EPS) accretion in its first full year.

Numis is bullish on cost savings and ‘the long-term combination of RWS’s operational excellence and SDL’s differentiated base’.

Berenberg says RWS is ‘highly attractive’ with an undemanding valuation and sees earnings upgrades as the synergies from the SDL acquisition – which it thinks could be £40 million per year – flow through, creating ‘material value for shareholders’.

Analysts at Jefferies believe annual cost savings could be as much as £50 million, which combined with higher revenues from cross-selling could lead to 17% growth in EPS for the next four years.

Tracsis

There are important reasons why 2021 could be a really good year for the Leeds-based transport infrastructure and analytics software company Tracsis (TRCS:AIM).

For years Tracsis has scored highly for earnings quality, cash flow and operating efficiency, based on Refinitiv data.

It has had a golden touch with acquisitions, always self-funded from internal cash flow and struck on relatively attractive terms. This has earned the company a growing number of fans.

We believe 2021 will herald a more ambitious phase for the company that will accelerate core growth and crank profit margins higher.

This may seem an odd time to be taking the proverbial bull by the horns, given the huge disruption Covid-19 has had on transport networks and mobility for individuals this year. But Tracsis has used the pandemic to assess its opportunities and will in future concentrate on the rail sector which makes sense once you look at the facts.

Tracsis’ business is largely split into rail technology – including software, consultancy and remote condition monitoring that play into automation, analytics and Internet of Things (IoT) investment themes – and traffic and data services.

In the financial year to 31 July 2020 the rail technology and services division generated revenue of £25.6 million while the traffic data services achieved £22.4 million.

The rail side is by far more profitable. Operating profit margins were 36% versus 5.8% from the traffic arm last year, the latter being significantly harder hit by lockdowns, work from home and other Covid impacts. Average traffic and data margins are still barely a third of the rail side (about 11% to 12%).

Aiming for mid-teens rail technology growth in future, you can see how profits down the line could grow much faster as this part of the business becomes dominant. Tracsis is aiming for double-digit organic growth and this will be topped up by more acquisitions in the future.

Bigger deals will be considered, albeit vetted as carefully and with the same focus on innovation and technology, but potentially loosening stock liquidity, a minor investor bugbear in the past.

This could also accelerate recurring revenues and international expansion, something that hasn’t come as quickly as hoped. Last year just 13% of revenue came from outside the UK, mostly from Europe.

Broker FinnCap is already factoring in faster growth and fatter profits, with this year’s estimated £9.3 million adjusted operating profit expected to hit £12.4 million in the following year. That’s 33% growth and something which should drive the shares much higher.

JD Wetherspoon

Hospitality has borne the brunt of the economic impact from the coronavirus pandemic and businesses in the sector have seen an unprecedented drop in income with people either blocked under Government restrictions or too nervous to go to the pub or to a restaurant.

The future of many firms in the industry are in doubt, but one company which has survivor written all over it is pub favourite JD Wetherspoon (JDW).

Described by Shore Capital analyst Greg Johnson as the ‘cockroach of the high street’, Wetherspoons is seen as best placed of any hospitality business in the UK to not only survive what is set to be a noticeably smaller market for a sustained period, but also gain considerable market share as a result of the shakeout in the pub and hospitality sector.

Given its reputation as being more affordable than many rivals, even if the economy doesn’t bounce back as expected in 2021 firms with value-led propositions are expected to outperform their peers. Wetherspoons is arguably best placed of all in the leisure sector, with its cheap meals, strong brand and easy-to-use table service app which make it a lot more adaptable to the current climate than its peers.

This was evidenced by the 32 million customer visits it had in the 10-week period from 4 July across 861 operational pubs as lockdown restrictions in the previous months were eased.

One of Wetherspoons’ competitive advantages during this pandemic is the fact the company operates from larger sites than its peers. Along with accommodating landlords and local authorities with regards to using more outside spaces, this helped entice customers back into its pubs.

The company reported a pre-tax loss of £34 million in the year to 26 July. However, according to the consensus forecast compiled by Refinitiv, Wetherspoons is expected to swing back into a profit next year.

Buying the shares ultimately means taking a view that society is going to start returning to normal in 2021. The stock is likely to be volatile until the vaccine is rolled out to a big chunk of the UK population, but we expect decent upside for the share price if people are allowed to move around more freely and feel confident enough to start to get out and about again.

The flipside is that if there are delays to the vaccine roll-out and the pandemic isn’t brought under control in 2021 then investors could lose money on this stock. As such, Wetherspoon’s shares are not suitable for nervous investors.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Stock pick for 2021: Alibaba

- Stock pick for 2021: Tracsis

- Stock pick for 2021: Eurofins Scientific

- Stock pick for 2021: JD Wetherspoon

- Stock pick for 2021: BHP

- Stock pick for 2021: Inspecs

- Stock pick for 2021: Convatec

- Stock pick for 2021: RWS

- Stock pick for 2021: PZ Cussons

- Stock pick for 2021: Diageo

- Stock pick for 2021: Qinetiq

- Stock pick for 2021: Ocado