Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

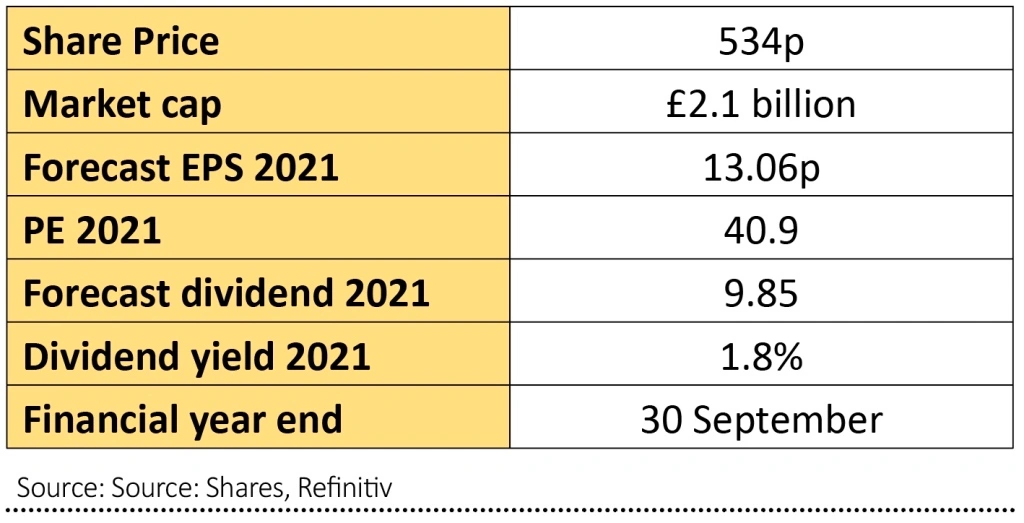

magazineStock pick for 2021: RWS

RWS (RWS:AIM) is the world’s leading provider of language services and language technology to firms in sectors such as technology, pharmaceuticals, medical equipment, telecoms and chemicals.

The recent acquisition of SDL marks a step change for the business with significant opportunities to grow, and the cost synergies from combining the businesses could be much greater than guided by RWS.

Before the SDL deal, half of RWS’s sales came from RWS Moravia, which works with technology companies such as Facebook to make sure their content, websites and apps are tailored to each geography and to ensure brand consistency.

Revenues in the year to 30 September rose 5% to £174 million driven by strong sales to its technology customers at the start of lockdown and increased demand from online sales platforms, web services and financial services clients.

A third of group revenue in the year came from IP Services, which provides patent translations and filing solutions as well as a range of intellectual property search services.

The third business is Life Sciences, which provides technical translations and linguistic validation to large pharmaceutical companies, clinical research organisations and medical equipment manufacturers.

Revenues were up 6% in the year to a record £69 million thanks to strong growth in Covid-related clinical trials, translation work for vaccines and anti-virals, and antibody testing equipment.

In November RWS completed the £854 million acquisition of UK rival SDL, cementing its position as the world’s largest language services and technology group with 90 of the top 100 brands by value, all of the top 10 pharmaceutical firms, most of the major West Coast technology businesses and half of the top 20 patent filers worldwide.

Chief executive Richard Thompson told Shares that even though the deal was only weeks old, his team had already identified annual synergies above the £15 million initially predicted.

The group’s new targets will be outlined in April, but RWS management expects the combination to generate double-digit earnings per share (EPS) accretion in its first full year.

Numis is bullish on cost savings and ‘the long-term combination of RWS’s operational excellence and SDL’s differentiated base’.

Berenberg says RWS is ‘highly attractive’ with an undemanding valuation and sees earnings upgrades as the synergies from the SDL acquisition – which it thinks could be £40 million per year – flow through, creating ‘material value for shareholders’.

Analysts at Jefferies believe annual cost savings could be as much as £50 million, which combined with higher revenues from cross-selling could lead to 17% growth in EPS for the next four years.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Stock pick for 2021: Alibaba

- Stock pick for 2021: Tracsis

- Stock pick for 2021: Eurofins Scientific

- Stock pick for 2021: JD Wetherspoon

- Stock pick for 2021: BHP

- Stock pick for 2021: Inspecs

- Stock pick for 2021: Convatec

- Stock pick for 2021: RWS

- Stock pick for 2021: PZ Cussons

- Stock pick for 2021: Diageo

- Stock pick for 2021: Qinetiq

- Stock pick for 2021: Ocado