Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStock pick for 2021: JD Wetherspoon

Hospitality has borne the brunt of the economic impact from the coronavirus pandemic and businesses in the sector have seen an unprecedented drop in income with people either blocked under Government restrictions or too nervous to go to the pub or to a restaurant.

The future of many firms in the industry are in doubt, but one company which has survivor written all over it is pub favourite JD Wetherspoon (JDW).

Described by Shore Capital analyst Greg Johnson as the ‘cockroach of the high street’, Wetherspoons is seen as best placed of any hospitality business in the UK to not only survive what is set to be a noticeably smaller market for a sustained period, but also gain considerable market share as a result of the shakeout in the pub and hospitality sector.

Given its reputation as being more affordable than many rivals, even if the economy doesn’t bounce back as expected in 2021 firms with value-led propositions are expected to outperform their peers. Wetherspoons is arguably best placed of all in the leisure sector, with its cheap meals, strong brand and easy-to-use table service app which make it a lot more adaptable to the current climate than its peers.

This was evidenced by the 32 million customer visits it had in the 10-week period from 4 July across 861 operational pubs as lockdown restrictions in the previous months were eased.

One of Wetherspoons’ competitive advantages during this pandemic is the fact the company operates from larger sites than its peers. Along with accommodating landlords and local authorities with regards to using more outside spaces, this helped entice customers back into its pubs.

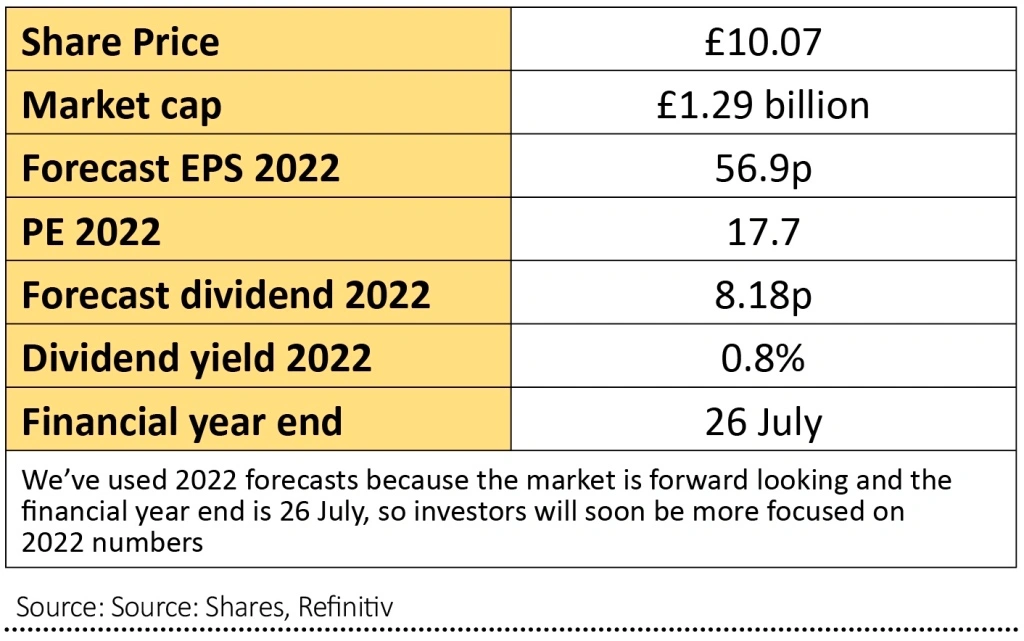

The company reported a pre-tax loss of £34 million in the year to 26 July. However, according to the consensus forecast compiled by Refinitiv, Wetherspoons is expected to swing back into a profit next year.

Buying the shares ultimately means taking a view that society is going to start returning to normal in 2021. The stock is likely to be volatile until the vaccine is rolled out to a big chunk of the UK population, but we expect decent upside for the share price if people are allowed to move around more freely and feel confident enough to start to get out and about again.

The flipside is that if there are delays to the vaccine roll-out and the pandemic isn’t brought under control in 2021 then investors could lose money on this stock. As such, Wetherspoon’s shares are not suitable for nervous investors.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Stock pick for 2021: Alibaba

- Stock pick for 2021: Tracsis

- Stock pick for 2021: Eurofins Scientific

- Stock pick for 2021: JD Wetherspoon

- Stock pick for 2021: BHP

- Stock pick for 2021: Inspecs

- Stock pick for 2021: Convatec

- Stock pick for 2021: RWS

- Stock pick for 2021: PZ Cussons

- Stock pick for 2021: Diageo

- Stock pick for 2021: Qinetiq

- Stock pick for 2021: Ocado