Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow our 2020 stock portfolio stayed afloat despite Covid

What a year. At the start of 2020 it was all about the political certainty in the UK delivered by the 2019 General Election but within a couple of months attention had turned to a nasty new virus emerging from China.

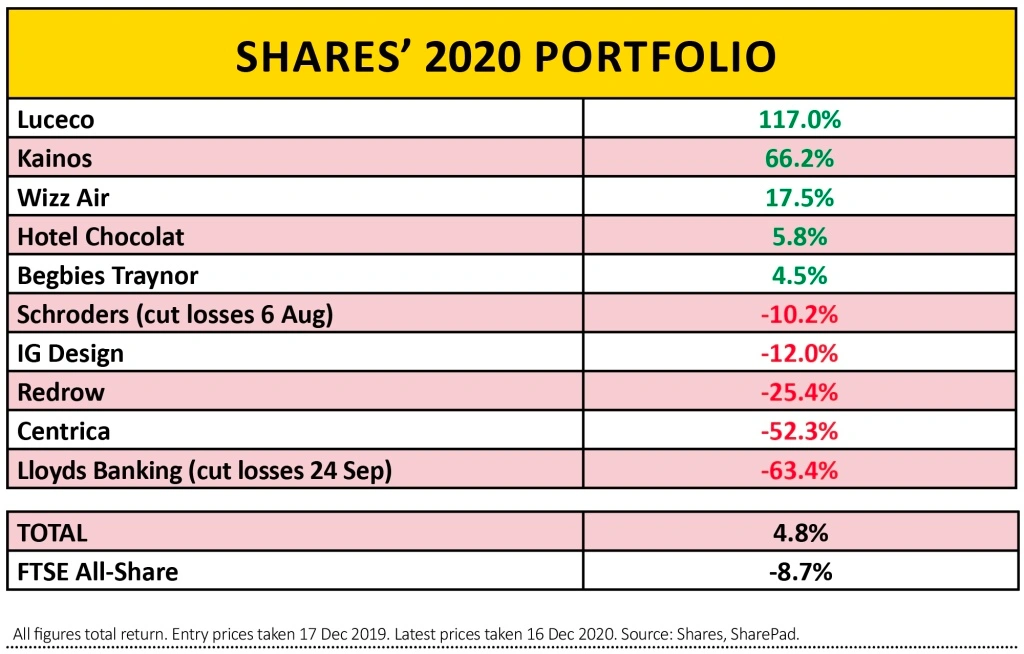

In the circumstances the 4.8% total return from our picks was a solid effort, given they were selected for a reality which was entirely overturned by the pandemic. Certainly, we did better than the wider UK market with the FTSE All-Share down by 8.7% despite the recovery from its March lows.

However, this doesn’t tell the whole story. We enjoyed some big hits and big misses along the way. Appropriately the list of winners is split exactly 50-50 with five of our selections in positive territory and five in the red.

It is also fair to acknowledge that the return we eked out is less than the broader MSCI World index which achieved a 16% total return over the same timeframe.

LUCECO LIGHTS UP

Let’s start with the good news. Our faith in a recovery at electronic products supplier Luceco (LUCE) has paid off in spades with a 117% return.

The company, which also specialises in LED lighting, upgraded its earnings guidance several times in 2020, most recently on 20 October when it upped its full year adjusted operating guidance from at least £23 million to a range of £28 million to £30 million.

Luceco has seen higher margins by delivering improvements in its business model as it addressed historic issues around stock and currency management.

Coming in a somewhat distant second but still with a bumper profit is digital transition specialist Kainos (KNOS) with a 66% return.

We couldn’t have anticipated how the Covid-19 pandemic would drive demand for the company’s services – not least from several key government departments in the UK and the NHS.

The shares have given back some of their stellar gains since November 2020 – perhaps due to a rotation out of perceived Covid winners into reopening value plays thanks to the development of a Covid vaccine.

However, the earlier surge in the share price is not based on thin air. The increase in demand for its services was likely accelerated rather than inflated by the pandemic.

OTHER POSITIVE PICKS

Three other stocks managed to weather Covid to close out the year in positive territory. One of these names may be a bit of a surprise.

Everybody knows the aviation sector has faced an outsized impact from Covid, so to see Wizz Air (WIZZ) finish in the black is somewhat remarkable. It has been achieved thanks to several factors including limited debt, resilient load factors in growth markets in Eastern Europe, strong cost control and better ancillary revenue than its rivals.

Chocolatier Hotel Chocolat (HOTC:AIM) has, perhaps unsurprisingly given its web-based roots, been effective at switching channels from its stores to online and third-party partners in response to the pandemic.

As such digital demand was up 150% year-on-year in the early part of the 12-month period running to June 2021.

FINANCIALS FAIL TO PERFORM

Bigger gains might have been expected for insolvency specialist Begbies Traynor (BEG:AIM) given the impact on the economy of coronavirus. However, at least some of this impact was forestalled by unprecedented levels of state support.

In general, exposure to the financial sector turned out to be a mistake and we cut our losses on both our larger picks in this space before the end of the year, namely Lloyds Banking (LLOY) and asset manager Schroders (SDR).

Ultra-low interest rates, the risk of rising bad debts and regulator interference which prevented banks from paying dividends all contributed to an exceptionally poor performance for Lloyds.

DEBT MASSIVELY OUT OF FASHION

It has been an up and down year for the housebuilders, with a period of deep freeze during the first lockdown switching to a massive rebound amid pent-up demand in the remainder of the year.

However, Redrow (RDW) underperformed the wider peer group with its higher level of borrowings at the start of the pandemic not helping sentiment towards the stock, even if it has subsequently built back to a net cash position of £115 million (at the last count).

Equally, heavily indebted energy firm Centrica (CNA) may have made some progress on fixing its balance sheet but this hasn’t been enough to spare the stock from further weakness in 2020.

It has continued to be dogged by operational issues, exposure to commodity prices and difficulties in its consumer-facing British Gas business and on a five-year view the shares are now down as much as 80%.

Meanwhile the performance of another laggard, gift wrap to greeting card manufacturer IG Design (IGR:AIM) won’t be earning us any warm Christmas messages.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Stock pick for 2021: Alibaba

- Stock pick for 2021: Tracsis

- Stock pick for 2021: Eurofins Scientific

- Stock pick for 2021: JD Wetherspoon

- Stock pick for 2021: BHP

- Stock pick for 2021: Inspecs

- Stock pick for 2021: Convatec

- Stock pick for 2021: RWS

- Stock pick for 2021: PZ Cussons

- Stock pick for 2021: Diageo

- Stock pick for 2021: Qinetiq

- Stock pick for 2021: Ocado