Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSmaller company funds are staging a comeback

In recent years small caps globally have suffered from investor risk aversion and concerns over everything from Covid-19 perceptions to trade war and Brexit-related worries. Until the recent rotation into value, investors had continued to show a preference for larger companies, driving down the weighting to small caps held by both passive and active funds.

As 2020 draws to its conclusion, investors should ask themselves how much of an allocation should they continue to have with larger companies, and whether now is the time to focus more on global small caps in order to find the big success stories of the future?

We can already see the performance of many small cap funds having improved in recent months, so get on board if your portfolio is missing this part of the market.

‘ATTRACTIVE ENTRY POINT’

Robin Geffen, manager of Liontrust Global Smaller Companies Fund (B29MXF6), is convinced there’s ‘a really attractive entry point for buying global small caps’ at present.

He says that despite strong long-term returns, the past three years have been the worst for global small caps on a relative basis since the 1990s, creating an opportunity for long-term investors who buy now.

‘One of the best kept investment secrets is that smaller companies outperform larger companies consistently over the medium and long term,’ enthuses Geffen. ‘Since 1994, the start date of the World Small Cap index, small caps have consistently outperformed large caps and the longer you hold them for, the greater the probability of outperformance.

‘There’s a treasure trove of exciting smaller companies out there,’ continues Geffen. ‘This current level of underperformance by global smaller companies makes me very excited, as global smaller companies have a history of outperforming during periods of recovery in the market,’ he adds.

Interestingly, the most pronounced underperformance has been in the US, which Geffen regards as a fertile hunting ground for quality companies capable of exponential growth and where over 70% of the Liontrust Global Smaller Companies Fund is invested.

ROARING AHEAD

Liontrust Global Smaller Companies has trounced both the IA Global and MSCI World SMID Cap Index since its inception. Geffen’s investment philosophy is to buy tomorrow’s winners when they are no less than £2 billion. They are sold on reaching £10 billion, unless he thinks they can reach £50 billion or £100 billion or beyond, in which case he’ll bank some profit, but hold onto a smaller proportion of the shares.

Once a company surpasses £10 billion in value, its prospects are evaluated, and the best opportunities migrate to a sister fund run by the asset manager called Liontrust Global Alpha Fund (3119055). Recent examples of stocks that have made the jump include cloud communications platform Twilio, US-based voice-over-internet supplier RingCentral and software developer HubSpot.

Despite global small caps enduring one of their longest and most pronounced periods of underperformance relative to large caps since the 1990s, Liontrust Global Smaller Companies has performed strongly during this period against both the small cap index, the large cap index and in absolute terms, stresses Geffen.

His portfolio includes names such as security solutions company Rapid7, identity software management play SailPoint and eco-friendly decking products group Trex.

AROUND THE WORLD

Investors seeking exposure to smaller companies around the world have a wide choice of funds, both actively and passively managed.

For example, ASI Global Smaller Companies (B7KVX24) generated a 28.3% return in first 11 months of 2020 versus 8% from benchmark MSCI ACWI SMID index, according to Morningstar. Over the past five years it has achieved 17.7% annualised returns versus 12.6% from the benchmark.

There are also plenty of options for investors happy holding a series of funds in different geographies for small cap exposure rather than just having a global fund.

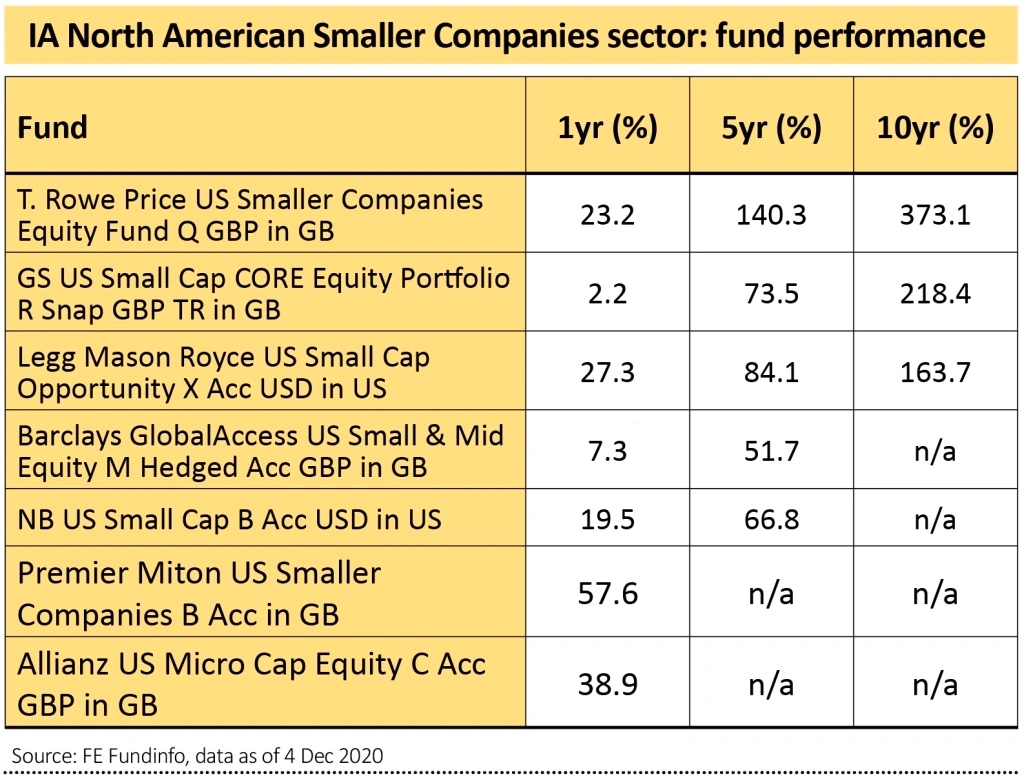

Shares has run the numbers to find the best five-year performers in the IA Japanese Smaller Companies, IA European Smaller Companies and IA North American Smaller Companies sectors.

According to Trustnet, they are Baillie Gifford Japanese Smaller Companies (0601492), Janus Henderson European Smaller Companies (0747642) and Artemis US Smaller Companies (BMMV576) respectively, the latter managed by Cormac Weldon and ranked first quartile over five years, during which it has materially outperformed its IA sector.

EXAMPLES OF ETFS

Investors who prefer low-cost passive funds have several options when it comes to global small caps. SPDR MSCI World Small Cap UCITS ETF GBP (WOSC) and iShares MSCI World Small Cap UCITS ETF GBP (WLDS) both track the same index, and the iShares product is cheaper with a 0.35% ongoing charge (versus 0.45% for the SPDR product).

The MSCI World Small Cap index tracks approximately 4,200 smaller companies from across 23 developed market countries. As of 30 October 2020, the average market cap size for companies in the index was $1.38 billion, with the largest being $14.4 billion and the smallest $32.7 million.

The index has generated 7.2% annualised returns, on a US dollar basis, over the past five years, or 8.8% annualised over 10 years.

Alternative ways of getting exposure to overseas small caps include ETFs that track relevant indices in key regions such as Europe, emerging markets and the US, such as Xtrackers MSCI Europe Small Cap UCITS ETF GBP (XXSC), WisdomTree Emerging Markets Small Cap Dividend UCITS ETF GBP (DGSE) and iShares MSCI USA Small Cap ETF USD Acc GBP (CUS1) respectively.

INVESTMENT TRUST EXAMPLES

The closed-ended structure of investment trusts is an advantage for fund managers investing in small, often illiquid stocks, where investment theses can take time to play out, as it means they aren’t forced sellers of stocks when investors want their money back, as can happen to open-ended fund managers.

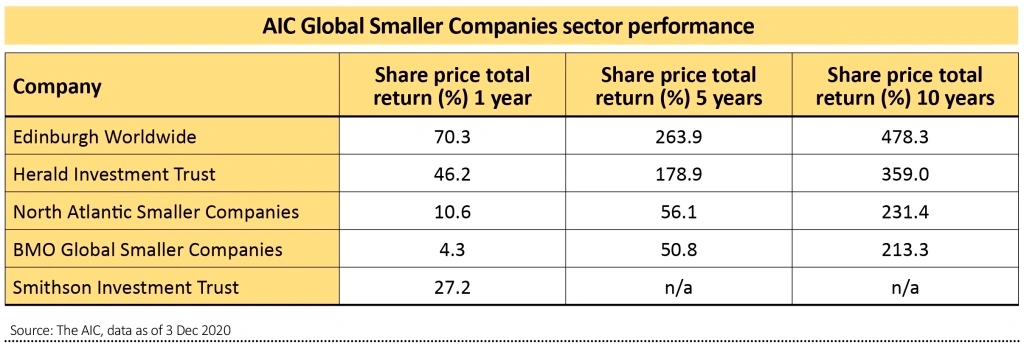

Investment trust options within the Association of Investment Companies’ (AIC) Global Smaller Companies sector include Smithson (SSON), the quality small-to-mid cap seeker which invests in firms that are too small for inclusion in Terry Smith’s flagship Fundsmith Equity (B41YBW7).

On a share price total return basis, the best performer of the past decade is Edinburgh Worldwide (EWI) with a 478.3% gain. The Baillie Gifford-managed trust’s strong showing is reflected in the shares trading at a 3.5% premium to net asset value.

Some would argue this isn’t strictly a small cap fund. Baillie Gifford starts off by investing in ‘initially immature entrepreneurial companies’ but manager Douglas Brodie runs his winners which means the best performing stocks are retained rather than sold when they get too big, explaining why $567 billion electric vehicle company Tesla and £16.5 billion supermarket technology group Ocado (OCDO) still feature in the portfolio.

Hot on Edinburgh Worldwide’s heels with 359% share price total return over the past 10 years is the Katie Potts-managed Herald Investment Trust (HIT), an investor in small caps in the tech space.

Trading on a 5.3% discount to net asset value and offering exposure to a diversified portfolio of international small caps is BMO Global Smaller Companies (BGSC). The trust invests in stocks as well as other collectives and has increased its dividend in each of the last 50 years.

‘Under the management of Peter Ewins, the strategy invests in a manner that has not only helped the trust outperform its benchmark over the long term, but has done so in a risk-conscious way,’ explain the analysts at Kepler Trust Intelligence.

‘Peter also makes use of externally managed collective investments for Japan and the emerging markets, such as open and closed-ended funds, leveraging members of BMO’s multi-asset and multi-manager teams to aid in identifying external managers.’

Disclaimer: Editor Daniel Coatsworth owns shares in Smithson and units in Fundsmith Equity referenced in this article.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

Money Matters

News

- Supply chain issues could mean a bleak winter for UK consumers

- Big Goco shareholder Peter Wood throws weight behind Future tie-up

- Questions still linger over National Grid and SSE dividends

- Key catalysts for markets before the end of 2020

- Flutter Entertainment secures prize US asset

- Fast growing hydrogen stock Ceres gets closer to fulfilling its potential