Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHigher margins should drive big share price gains for DiscoverIE

Electronics engineer DiscoverIE (DSCV) has been on quite a journey in recent years, pulling itself up the supplier value chain by executing a clear strategy.

This ambitious adventure is far from over. We believe the company’s success will soon lead to its share price trading beyond 750p for the first time in 20 years.

We have followed the DiscoverIE growth story for quite some time and flagged its appeal many years ago when it was called Acal.

SHARPER FOCUS

The company used to be a simple distributor of parts and components to the electronics manufacturing industry. It still makes about a third of its revenue from supplying bits of kit on long-run contracts (£76.6 million of the first half to 30 September’s £217.9 million group sales) through its Custom Supply (CS) arm.

During the past few years, it has made a deliberate attempt to design and make bespoke pieces of equipment to highly regulated industries, now called the Design & Manufacturing (D&M) operations.

It focuses on sectors where unique custom designs are often required and where corners simply cannot be cut, such as medical, aerospace, transport and renewables. These are sectors where equipment needs to be high-performance, reliable, efficient and regulations-compliant, and that should mean fatter profit margins.

There are also high barriers to entry, providing reasonable defence against lower grade, me-too products from low-cost places like China and elsewhere.

For example, it makes components such as blade controls for wind turbines, artificial intelligence-based telematics and connectivity components, and sensing and power systems.

The customised nature of many designs helps raise the value of these products and often creates a virtuous cycle of replacements over years.

This strikes us as a very sensible strategy and one that, presuming all goes to plan, could prove very profitable for the company and its shareholders.

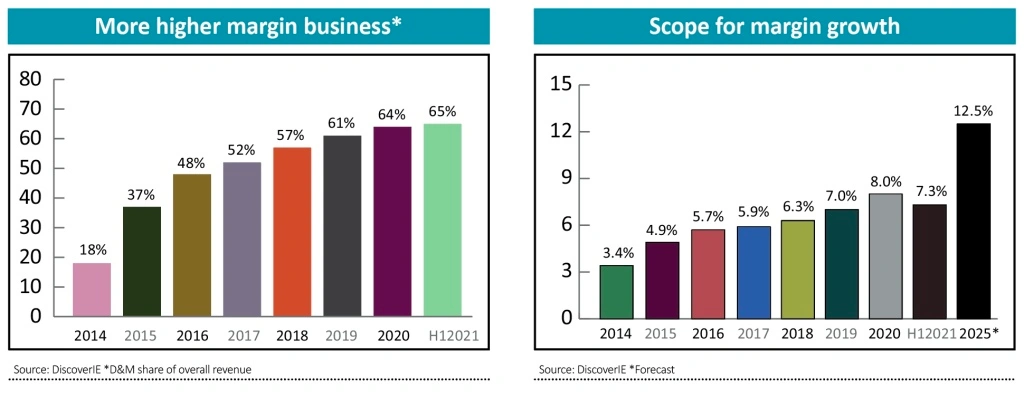

IMPROVING MARGINS

Because a large part of income still comes from distribution it means that operating profit margins are coming from a comparatively low starting point.

Operating profit margins were just below 6% a couple of years ago, but they had improved to 7.3% across the company in the latest half year period to September.

Some analysts see the opportunity to improve low single-digit supply margins, but the real profit boost will come as DiscoverIE continues to expand its higher, double-digit margin D&M side. This combined transition should see overall operating margins move to 8% in the next year or two, with 12.5% targeted by 2025.

To put that into context, an 8% operating margin in the first half this year would have added £1.6 million on top of the £15.8 million operating profit reported.

ACQUISITION PROSPECTS

Progress was slowed by the Covid-19 pandemic this year, which suggests that with the widening deployment of vaccines through 2021, recovery could come quickly.

This will be bolstered further through buying in new growth opportunities and expertise. Mergers and acquisitions have always been a part of the story – DiscoverIE has done around 15 deals over the past decade, but the company is now increasingly looking to expand beyond its UK/Europe traditional stomping ground.

The €14.5 million purchase of thermal components and sensors business Limitor earlier this month is a good example. While it will mainly bolster sales in Europe, about 15% of its €8.5 million income in 2019 was spread over the US, Asia and European nations outside the EU.

The Limitor deal pushed net debt to about 1.5-times earnings before interest, tax, depreciation and amortisation (EBITDA), comfortably within the company’s preference not to exceed two-times, and way below the three-times level when lenders typically start to get nervous.

DiscoverIE is also fantastically cash generative, throwing off 159% of operating profit as cash flow in the first half (2019: 106%). This means that borrowings can be paid down quickly if needs be, or additional debt can be managed if the right acquisition crops up.

Analysts are forecasting diluted earnings per share (EPS) of about 22.5p for the current Covid-impacted full year to 31 March 2021, about 25% to 30% down on last year. But EPS recovery is expected to be sharp, with 26.5p and 28.5p pencilled in for the following two years. We wouldn’t rule out a takeover from a larger peer in the future.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

Money Matters

News

- Supply chain issues could mean a bleak winter for UK consumers

- Big Goco shareholder Peter Wood throws weight behind Future tie-up

- Questions still linger over National Grid and SSE dividends

- Key catalysts for markets before the end of 2020

- Flutter Entertainment secures prize US asset

- Fast growing hydrogen stock Ceres gets closer to fulfilling its potential