Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBig drug companies: The ones to make the world and your portfolio healthy

This year has reminded the world about the importance of the pharmaceutical industry and investors have understandably become very interested in the sector’s big players.

With a vaccine for Covid-19 now being rolled out, the market’s attention is moving on to earnings prospects for companies involved in this treatment as well as those tackling other illnesses.

It’s plausible that governments globally will be more committed to combating health issues following the pandemic, and the rapid speed at which the Covid-19 vaccine has been developed raises the question of whether other drug developments could be accelerated.

All these factors make the pharmaceutical industry very interesting and so investors naturally want to know which stocks to own. We’ve got three top picks in this article and one to avoid.

GIVING THE INDUSTRY A BOOST

The Pfizer-BioNTech vaccine, which received emergency approval from the UK regulators last week, marks the fastest ever development of a vaccine.

This could provide a much-needed boost for an industry that prior to 2020 was struggling with its public image in the face of increasing criticism over alleged ‘predatory’ drug pricing and shareholders losing faith in the growth story.

Finding a vaccine in record time has the potential to radically improve the image of the industry and permanently change the way new drugs are developed.

The global effort and collaboration between public bodies, academic institutions and pharmaceutical companies has also been a game-changer.

SPEEDING UP DRUG DEVELOPMENT

A lot of the processes that would be normally have been done sequentially were done in parallel, saving valuable development time.

In addition, key manufacturing capacity has been built ahead of approvals from regulators so that distribution can begin as soon as safety data has been validated.

Government financial support lowered the financial risk and encouraged some drug companies to take more risk on cutting edge technologies and innovative solutions.

Good examples are the Pfizer and Moderna Covid-19 vaccines which came about by experimenting with mRNA technologies which until now have never been commercialised.

Traditional vaccines infect people with a modified harmless version of the virus so that the bodies’ immune system can recognise the threat.

With an mRNA injection the body’s immune cells are told how to recognise the virus so that the body can make antibodies. This means the virus doesn’t need to be grown in the lab, saving valuable time. It also means there is zero chance of accidentally infecting people with the virus.

TOO GOOD TO BE TRUE?

While it’s generally thought the required safety protocols have been followed, there is a risk that the public might view the speed of approval as a sign that corners were cut or that longer-term effects of taking a vaccine haven’t been given enough consideration.

The confusion surrounding the AstraZeneca (AZN)/Oxford University Covid-19 vaccine trial results is a good example of the fine line that big pharma and governments need to tread to keep the public trust. Making vaccination mandatory is unlikely to be a successful long-term strategy.

The announcement from AstraZeneca focused on an average effectiveness of 76% depending on the level of dosage. But it turned out that the higher 90% rate was effective only on patients under the age of 55 and involved a half dose followed by a full dose which wasn’t the originally intended dosage.

The efficacy rate is still way more effective than the average flu jab, but this got lost in the debate, leaving some observers questioning the credibility of two of the most respected institutions in the world.

In any event AstraZeneca’s chief executive Pascal Soriot has said the company will conduct another trial to confirm the true relationship between dosing pattern and efficacy.

One important point to bear in mind is that all the vaccine makers have said they will submit clinical data for peer review, so when all the dust settles, only the most effective vaccines with the best safety data will be on the market.

PHARMA TO THE RESCUE

In addition to Pfizer and AstraZeneca, other large pharma companies such as GlaxoSmithKline (GSK) and French group Sanofi are also collaborating on a Covid-19 vaccine. Eli Lilly recently signed an agreement with the US government to supply 300,000 of its investigational neutralising antibodies called Bamlanivimab. It is seeking emergency approval use.

The big pharma groups involved in developing vaccines for Covid-19 have said they don’t intend to make a profit from the pandemic, at least initially.

That doesn’t rule out doing so in the future if, for example, annual vaccinations are required like the flu jab. But most analysts’ forecasts don’t include any financial benefits from successfully developing a vaccine at this stage.

That said, there may be longer-term benefits to flow through to the pharma industry if it has the appetite and the will to apply what has been learnt from fighting Covid-19.

For example, it is intriguing to think what might be achieved if similar co-ordinated efforts and faster drug development were used to fight cancer and rare diseases.

At the least it may result in faster drug development which would have big implications for returns on investment. That’s because the faster and cheaper a drug is developed, the greater the return on the research and development spending. And greater interest in the sector and increased funding may be a welcome by-product.

NO GROWTH PRICED IN

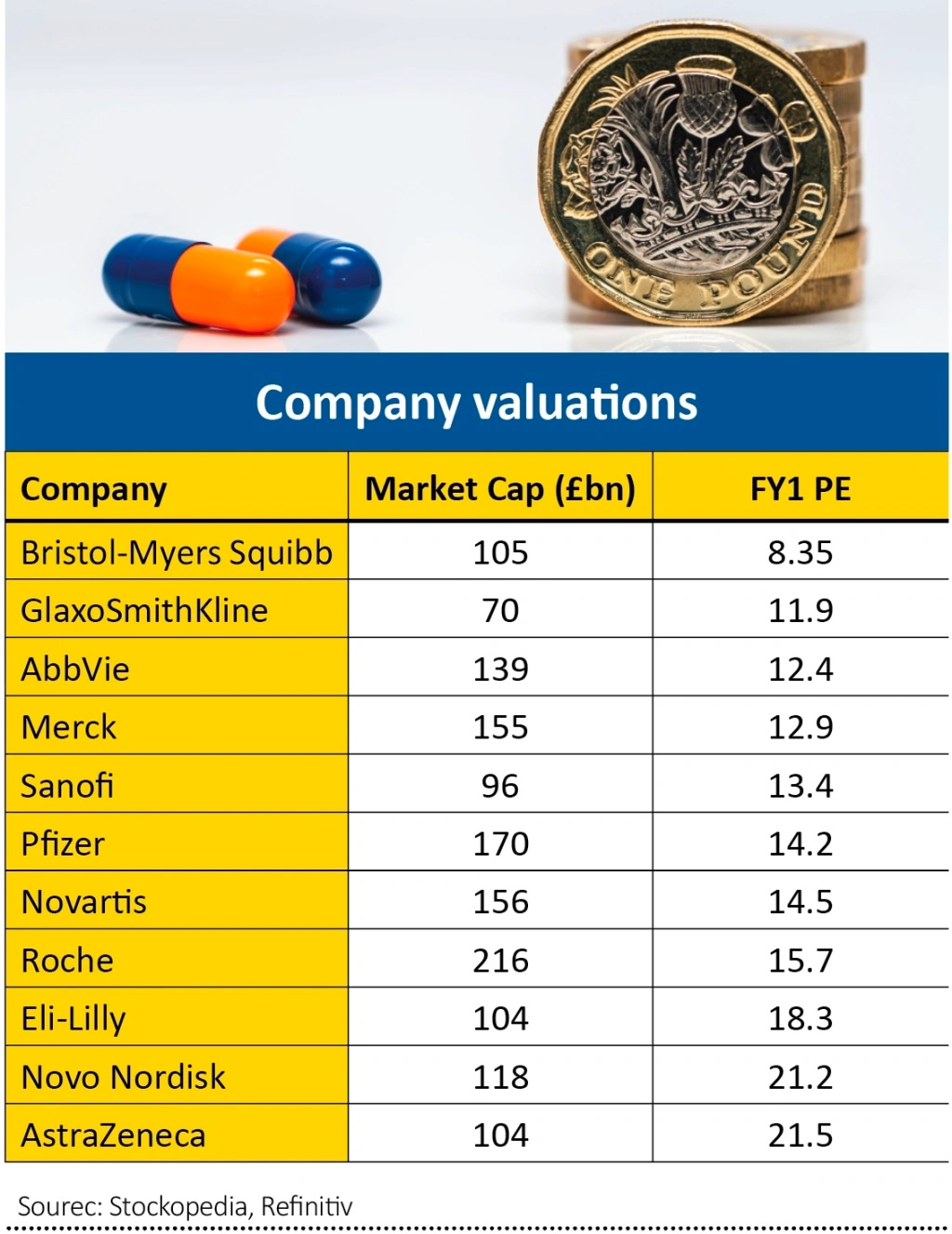

It might seem surprising that European and US pharma are trading at depressed valuations relative to the long-term averages.

During the late 1990’s pharma used to command a price to earnings (PE) ratio almost double that of the market. As the charts show the sector has since fallen out of favour with investors.

According to research published by Berenberg on 28 September this year, the sector just over two months ago was not only trading at a discount to its historical average but also to the general stock market in the case of the US, namely a 37% PE discount at the time of the study. European pharma traded at a small 6% premium to the European stock market.

This means from an investment perspective, there isn’t much of a growth premium priced into the sector. This looks anomalous given significant long-term growth potential stemming from increased demand for new drugs as a result of an ageing global population.

HAVING A TIGHTER FOCUS

Many of the big companies have in recent times shed non-core assets to become pure-play specialist pharma groups focused on specific areas of science.

For example, GlaxoSmithKline plans to divest its consumer healthcare business into a joint venture with Pfizer’s in 2022, to focus on its vaccine and cancer franchises.

Lastly there is the prospect of the industry becoming more efficient which will boost profitability and cash generation.

MANAGING PATENT EXPIRIES

The key to delivering growth and shareholder value is creating the right balance between revenue growth today and future growth from a strong pipeline of new drugs.

That’s because patented drugs generally expire after 20 years, which means drug companies need to replace lost revenues from expiring patents.

Once drugs lose their patent exclusivity and protection, they are quickly challenged by generic drug makers who undercut on price and rapidly take market share.

Not having a balanced portfolio can lead to a so-called patent cliff, which refers to a sudden loss of revenues which aren’t immediately replaced.

US firm Pfizer is a good example of a company which faces a deep cliff from 2026 according to Berenberg analysts who reckon it will lose $18 billion of sales between 2025 and 2030.

It is forecast to make incremental sales of $1.7 billion a year from growing assets but an average $4.4 billion of lost sales to eroding assets in the second half of the decade.

In contrast AstraZeneca has relatively few eroding assets and a strong pipeline of new drugs. Its cancer franchise growth is expected to result in an estimated $6 billion of incremental sales over the next two years.

Later stage growth from the pipeline is expected to come from its cancer, lupus and respiratory products currently in development as well as expansions to its successful Imfinzi/Lynparza cancer treatments.

The potential value of Eli-Lilly’s pipeline stands out and represents a relatively high 20% of its total portfolio value according to Berenberg estimates. This is encouraging given the benign erosion of sales over the coming decade at just 4% a year.

The company has also successfully streamlined its activities to become a pure-play pharma business after it exited animal health in 2018.

Eli Lilly is focused on the diabetes market and has a strong market position. Trulicity, one its drugs used in the treatment of type II diabetes, is expected to be one of the top selling diabetes drugs in the market by 2024 according to management.

INVESTING IN PHARMA VIA FUNDS

Investors who prefer funds to individual stocks can get exposure to the pharma sector through various means including Polar Capital Global Healthcare (PCGH), an investment trust which seeks to generate capital growth by investing in a global portfolio of healthcare stocks.

Its top holdings include Roche, Medtronic, UnitedHealth, Sanofi, Amgen and Eli Lilly. The trust trades on a 10.6% discount to net asset value and has generated a 7.7% annualised share price return over the past five years to 3 December, according to Morningstar.

Another way to get exposure is via exchange-traded fund Amundi ETF MSCI Europe Healthcare UCITS ETF GBP (CH5). This track the MSCI Europe Healthcare index which contains mid and large healthcare stocks from 15 developed market countries in Europe. The top holdings are Roche, Novartis, AstraZeneca, Novo Nordisk, Sanofi, GlaxoSmithKline and Bayer.

The index has delivered a 5.8% annualised return over the past five years to 30 November, says MSCI. The Amundi ETF has a 0.25% annual ongoing charge.

GETTING A GOOD RETURN ON RESEARCH AND DEVELOPMENT

Another key component of delivering good shareholder returns is to ensure that the investments into the pipeline of new drugs achieve an adequate economic return.

The key levers are development costs and the level and duration of commercial success of those drugs that make it to market.

AstraZeneca is a standout performer, being the most efficient developer of new drugs, spending an average of around $1.2 billion and achieving a return on investment of around 11%.

At the other end of the spectrum are Bristol-Myers Squibb and Swiss-based Roche which spend more than double in development costs, some $2.6bn but do manage to achieve decent returns on investment of between 8% and 9%.

THE PHARMA STOCKS TO BUY

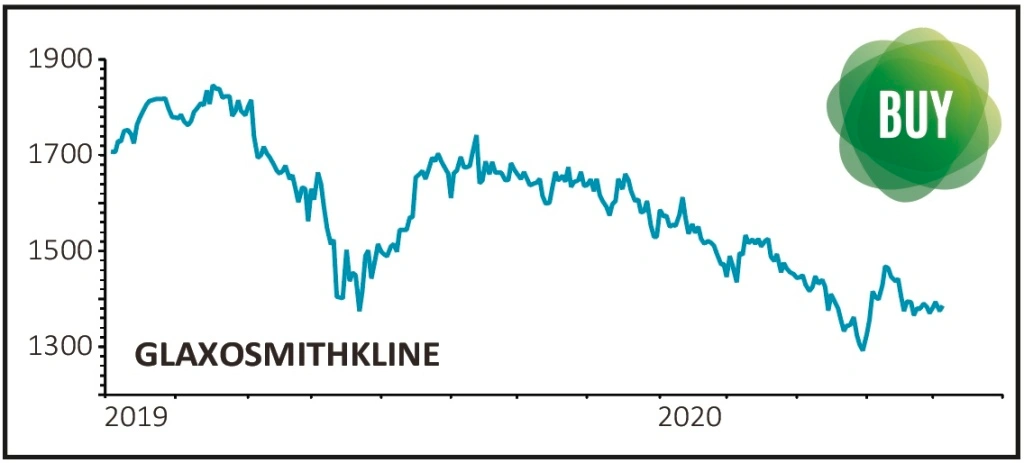

GlaxoSmithKline

Price: £13.96. Market Cap: £69.3 billion

We believe GlaxoSmithKline offers investors underappreciated growth with margin uplift potential as it prepares to spin off its consumer healthcare division into a joint venture with Pfizer’s consumer healthcare business, unlocking value.

The short-term drag on the sales momentum of its vaccines business due to access disruption in the early part of the year will lift at some point in 2021. The fast-growing shingles product Shingrix will benefit from increased capacity in 2023, allowing entry to key markets such as China.

The cancer franchise has a strong pipeline with Liberum forecasting revenues to reach $4 billion by the end of the decade.

The performance of ovarian cancer drug Zejula and Blenrep for treating multiple myeloma, a type of bone marrow cancer, is key to delivering future growth above the industry average.

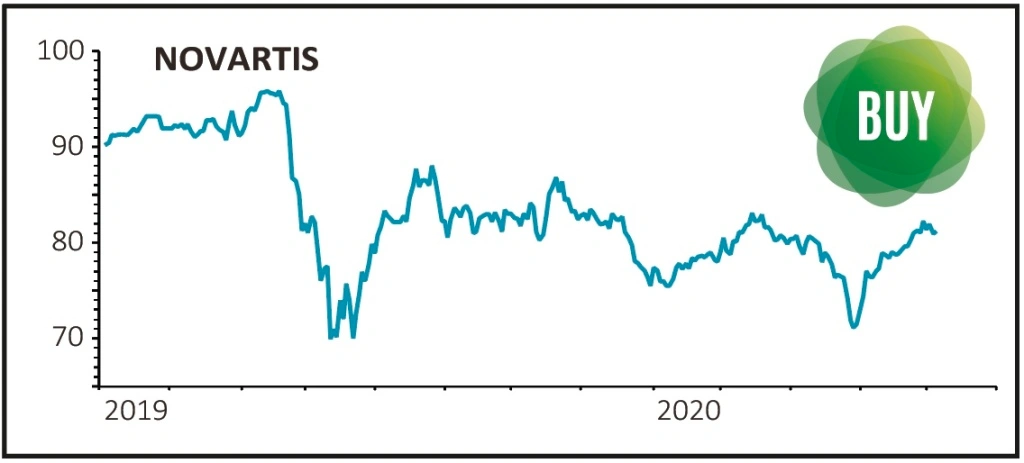

Novartis

Price: CHF 82.2. Market Cap: £153.3 billion

With its shares trading on the Swiss Stock Exchange and the New York Stock Exchange, Novartis consists of two divisions: Sandoz which manufactures generic medicines and a branded pharmaceutical division called Innovative Medicines.

Chief executive Vas Narasimhan has simplified the structure of the business with the separation of ophthalmology company Alcon while business costs have been streamlined, giving a boost to margins.

While the scope for incremental margin expansion has narrowed profit growth from established drugs like Cosentyx (treatment of psoriasis and psoriatic arthritis), heart failure drug Entresto should drive near-term growth.

The shares trade on a PE of 14.5, an unwarranted discount to the sector average compared with the growth potential.

Bristol-Myers Squibb

Price: $62.37. Market Cap: $105.1 billion

The $80 billion acquisition of Celgene in 2018 made Bristol-Myers Squibb a leading biopharmaceutical company with a more diversified revenue steam.

The company has dominant positions in cancer, immunology (using the body’s immune system to fight infection) and cardiovascular disease.

The deal was seen by analysts as a unique opportunity to combine complementary portfolios and thereby reduce reliance on a single cancer drug.

The combined pipelines have numerous opportunities to launch new drugs in an area of dominance and expertise.

Berenberg sees several possible catalysts over the next 12 to 18 months which secures the long-term outlook.

None of this potential is reflected in the valuation of the shares which trade on 8.4 times next year’s earnings, which is too cheap given the potential growth.

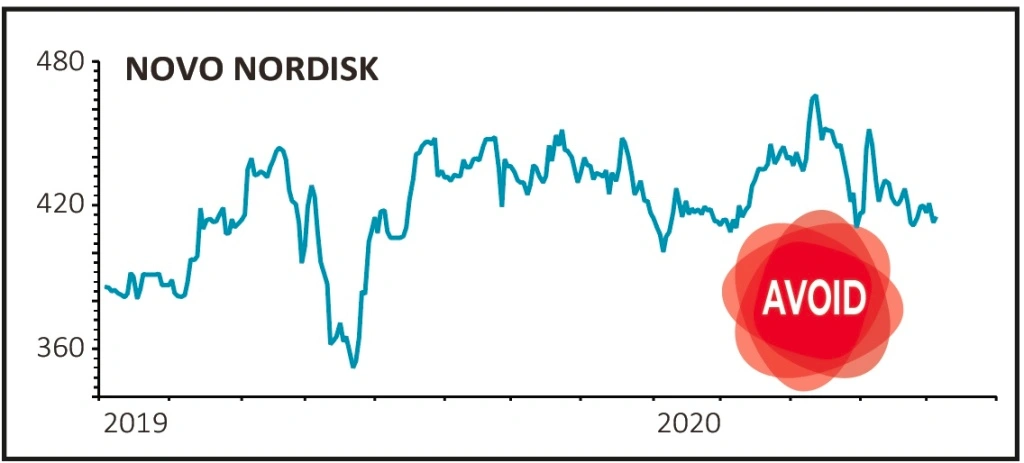

THE PHARMA STOCK TO AVOID

Novo Nordisk

Price: DKK 413.7. Market Cap: £118 billion

Novo Nordisk is a pure-play biopharmaceutical company focused on diabetes, obesity and haemophilia (impaired ability to make blood clots, to stop bleeding).

While the company’s returns on R&D spending has been best in class at around 22%, the shares trade at a PE premium to the sector which fully reflects past success as well as growth expectations for anti-diabetic drug Ozempic.

Berenberg notes the relatively ‘light’ pipeline which is expected to grow around 8.4% compared with the sector average of 12.4%.

In addition, the company has said it faces some headwinds in the US market from the impact of higher unemployment which moves more people into the lower price rebated government funded Medicaid system.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

Money Matters

News

- Supply chain issues could mean a bleak winter for UK consumers

- Big Goco shareholder Peter Wood throws weight behind Future tie-up

- Questions still linger over National Grid and SSE dividends

- Key catalysts for markets before the end of 2020

- Flutter Entertainment secures prize US asset

- Fast growing hydrogen stock Ceres gets closer to fulfilling its potential