Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe secret formulas employed by the experts

The main reason investors care about valuation is because of the risk of suffering underperformance if they overpay for a stock.

There are many different approaches used to value companies ranging from discounted cash flow based measures, relative valuation and multiple based methods.

In this article we take a closer look at specific valuation metrics used by four fund managers and discuss how they are incorporated into the investment process.

We have selected screening criteria to identify stocks which could qualify under each valuation approach although these are just a starting point for further research. All the managers we spoke with emphasised that screening was just one part of the overall investment process.

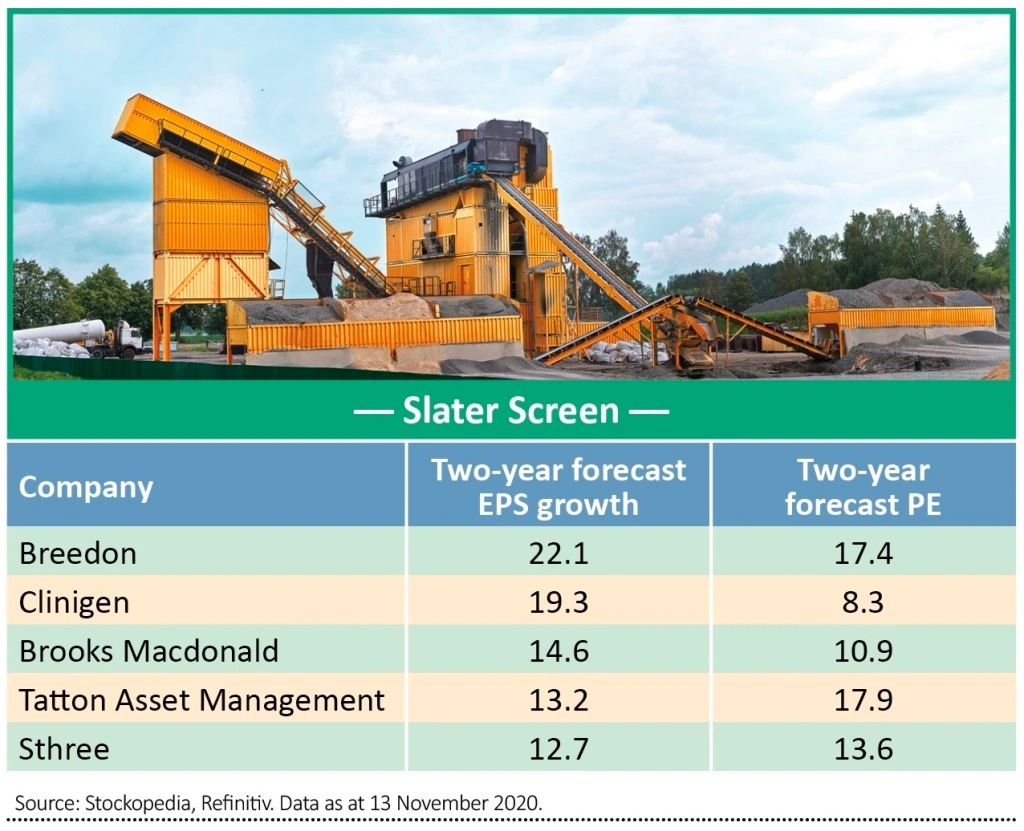

THE PEG RATIO

The PEG (price-to-earnings growth) ratio is the PE (price-to-earnings) ratio divided by growth and was effectively first referenced by Peter Lynch in his book One Up on Wall Street where he said: ‘The PE ratio of any company that’s fairly priced will equal its growth rate.’

Lynch managed Fidelity’s Magellan Fund from 1977 to 1990 with assets under management growing from $14 million to $14 billion under his tenure.

In the early 1990’s Jim Slater popularised the PEG for UK investors and it is still used to manage money at Slater Investments under the tutelage of his son Mark Slater. For Slater the PEG ratio adds another dimension to the PE by incorporating growth into the equation.

After all, growth is what investors pay for and the PEG has the added advantage that it allows investors to compare companies with different growth rates and PE’s.

Mark Slater told Shares that stipulating at least double-digit expected earnings growth eliminates 95% of the universe of available investments leaving the team a more manageable list of investments to scrutinise and to conduct qualitative assessments.

What the Slater Growth Fund (B7T0G90) is looking for is companies which can grow sustainably over the medium term, so the team removes cyclical companies and those with no history of consistent growth. At the same time Slater doesn’t want to overpay for growth, so he insists on a PEG ratio below one, that is to say, the PE should be below the expected growth rate.

Slater says the firm had never paid more than a PE of 20 for a share over its 26 year history. Another important consideration is that companies are generating cash in line with profits. Once the team have identified potentially good growth businesses trading at attractive prices, they conduct further qualitative work. The goal is to ascertain the reliability of the growth.

One very important part of the qualitative work is to make a distinction between a ‘very good growth’ business and ‘an excellent’ one. The team would be minded to take profits if the PE of the former gets ‘ahead’ of its sustainable growth rate, essentially sticking to the PEG valuation discipline.

However the fund would look to hold an excellent growth business forever, irrespective of value as long as the growth credentials remained intact. Slater emphasised that running winners was key to delivering top-notch returns for growth oriented mangers.

A good example and the largest holding in the Slater Growth Fund is media company Future (FUTR) which was initially purchased for 200p for a PE of 12 compared with the current £19.90 and forward PE of 24 according to data provided by Stockopedia and Refinitiv.

CASH FLOW RETURN ON INVESTMENT (CFROI)

The CFROI measures a company’s cash flow in relation to its cost of capital, adjusted for inflation. The model ‘looks through’ reported earnings numbers to the underlying cash flows and attempts to calculate a ‘true economic return’.

Guinness Asset Management differentiates its investment approach by filtering the global equity universe through Credit Suisse’s proprietary Holt CFROI model. To qualify as an investment candidate for its funds, companies must first demonstrate a CFROI of at least 10% a year for every year of the past decade.

This reduces the global universe to around 500 companies. It also ensures the screen only captures companies which have maintained high returns through thick and thin.

Companies passing the initial screening are thought to have an 80% chance of continuing to earn higher than 10% CFROI over the subsequent three-years.

One of the advantages of CFROI is it provides a consistent approach to compare operating performance across a portfolio, or markets with different accounting rules.

The Guinness Global Income fund (BVYPNY2) then applies a valuation tilt to find those companies which are cheap versus the market, peers and the company’s own history, using more traditional metrics such as price to cash flow.

It is also on the lookout for situations where the market has wrongly assumed a company’s returns will fall back to average.

The value tilt differentiates the income fund from other quality focused managers that tend to be exposed to growth rather than value.

We don’t have access to the Holt product, and have used return on capital employed as a proxy measure combined with earnings yield to isolate qualifying stocks. Earnings yield is operating earnings divided by enterprise value, or the total value of a company including net debt.

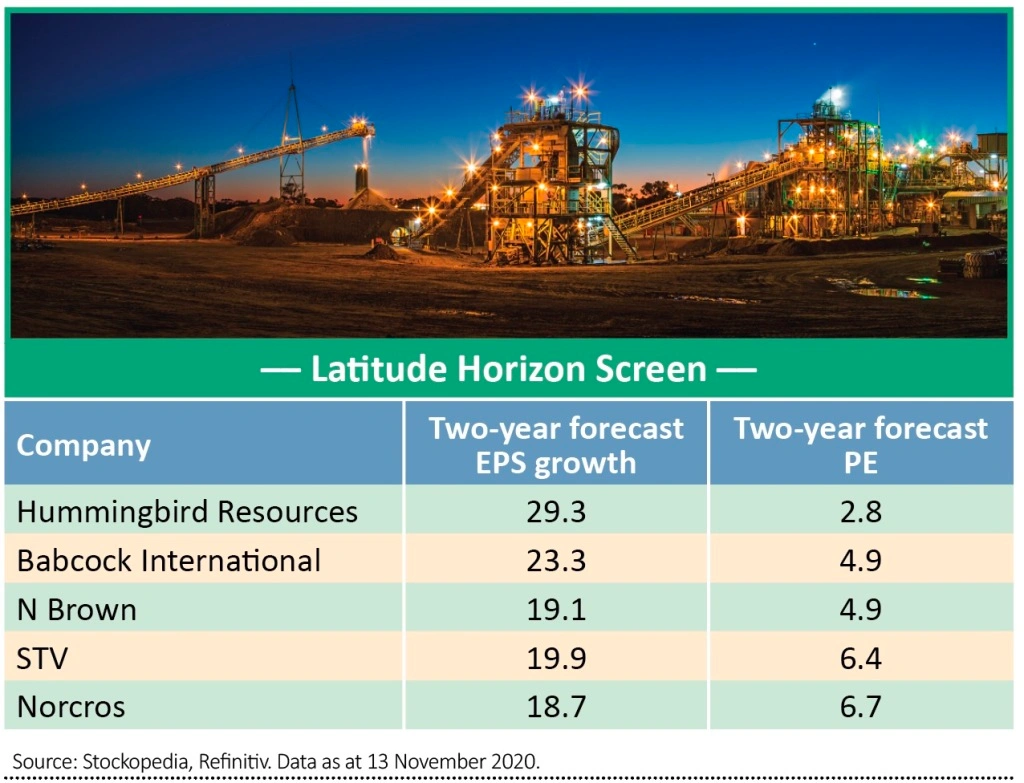

GROWTH IN INTRINSIC VALUE

Freddie Lait, manager of the Latitude Horizon Fund (BDC7CZ8) believes the most important factor in delivering investment success is to focus on the growth in intrinsic value as well as capital returned to investors via dividends.

The team is very patient with Lait telling Shares they ‘buy only when prices are demonstrably cheap. Although by no means a fixed rule, stocks trading on roughly 12 times forward PE, 8% FCF (free cash flow) yield or around one times tangible book value, are highly attractive provided the business is of high quality.’

The firm believes the best metrics for capturing intrinsic value are EPS, free cash flow and in the case of capital intensive industries book value per share. High returns on capital are also considered an attractive characteristic.

Essentially the team are looking for businesses with strong market positions and competitive advantages which can grow their intrinsic value sustainably at between 8% and 12% a year. The premise is that over the long term share prices follow earnings.

Focusing on intrinsic value is considered more predictable and preferable than relying on the ‘quick fix’ of multiple expansions. This refers to the PE ratio going up or down irrespective of earnings or cash flow.

Lait expects the bulk of the fund’s returns to come from growth in intrinsic value with an additional 1% or 2% coming from the PE moving ‘back to trend’ or mean-reverting as it also referred to sometimes. In other words, the team’s patience and value discipline is also expected to pay off.

It is worth noting that around half of the portfolio is held in low risk bonds and inflation protected bonds. This part of the portfolio offers protection in volatile market conditions and provides a very safe positive return of around 3% a year.

FREE CASH FLOW YIELD

While investor favourite Fundsmith Equity (B41YBW7) is focused on finding the world’s best quality companies and holding them for a long time, it is also keen not to overpay for those businesses.

In the owners manual, Terry Smith outlines a valuation approach based on the forecast annual free cash flow yield. This metric compares the annual free cash flow per share with the share price.

The manager is looking for yields which are high relative to long-term interest rates and when compared with the free cash flow yields of other investment candidates.

Free cash flow here is calculated after deducting taxes and interest expenses but adding back discretionary capital expenditures, sometime shortened to capex, so as not to penalise the company for investing in growth.

It’s worth pointing out that calculating what part of capex is discretionary or growth related and what is necessary for maintaining operations isn’t as straightforward as it sounds because companies don’t readily split it out this way.

One way to estimate it according to famed investor Warren Buffett is to add-up capex over the last five-years and then deduct depreciation charges. What’s left over is a good guide to the amount of growth capex spent.

In more recent market commentaries the Fundsmith team has said it is comfortable paying a premium for quality businesses, because it argues that valuation is not as important as sustainable growth, especially over the long-run.

High quality businesses with sustainable growth prospects are a key focus for the team when conducting fundamental research. These companies are characterised by higher than average returns on capital employed and consistent rather than explosive growth.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.