Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy fund investors are under-allocated to the US and does it matter?

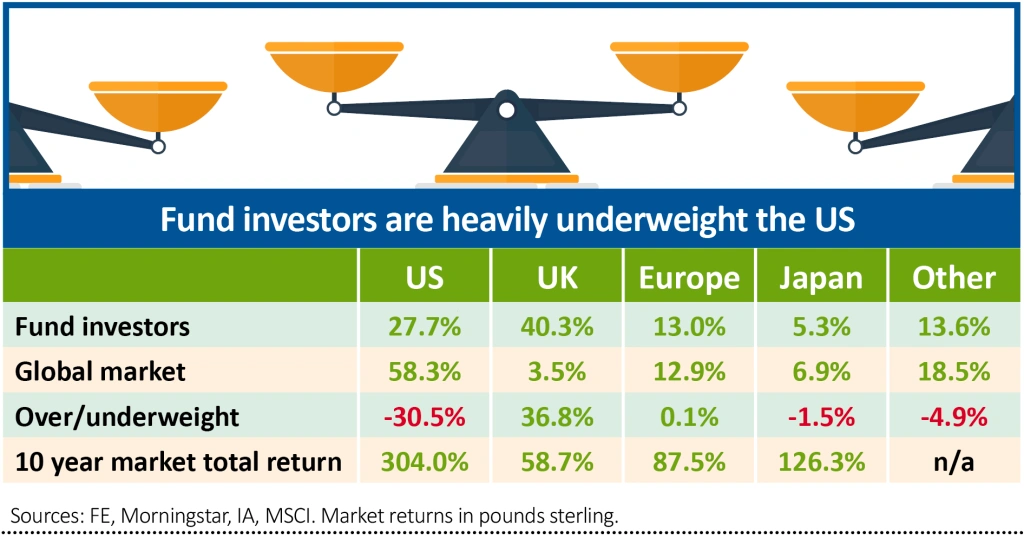

It’s been a cruel ten years for investors in this country, who have watched the US stock market go from strength to strength while our home market brings up the rear. This is particularly galling because the typical fund portfolio is significantly underweight the US, and overweight the UK.

While the US stock market has turned £1 into over £4 over the last ten years, the UK market has turned that same £1 into just £1.60. Meanwhile the typical fund portfolio is around 30% underweight the US, and 37% overweight the UK.

PERFORMANCE GAP

The performance gap between the US and UK markets can in large part be attributed to currency effects, the overhang of Brexit, and the sectoral composition of the indices. The biggest companies in the US stock market are new economy tech titans, while the top end of the Footsie is packed with cyclical stocks in oil, mining and financial sectors, which have found it tough going of late.

In recent years investors have sold out of UK funds, but this sector still tops the charts in terms of the amount of assets invested, followed closely by global funds. There are longstanding reasons for the funds market being skewed to the UK over the US, not least the fact that the UK market has historically been a great source of dividends for income seekers.

Even fund managers in the global sector, with a worldwide remit, are underweight the US. Of the 210 funds we analysed in the sector, 170 were underweight the US market compared to its weighting of 66.5% in the MSCI World Index of developed markets. This goes some way to explaining why the IA Global Sector has underperformed the MSCI World Index by around 45% over 10 years.

Again there are reasons why global fund managers are underweight the US market. It’s a well-analysed market, and adding value through stock selection is therefore theoretically harder than in the UK. Seeing as it makes up two thirds of the global stock markets of developed countries, you also have to have a very high conviction in that market to put that much of your portfolio there.

DRIVING FORWARDS

While it’s undeniable that the US stock market has been the place to be over the last ten years, looking in the rear-view mirror isn’t the best way to navigate if you’re planning on driving forwards.

The US might well continue to shine if the strong keep getting stronger. The likes of Amazon, Apple and Netflix have thrived in the pandemic, and while valuations look lofty, that’s been the case for some time, and that hasn’t stopped investors turning a healthy profit. What’s more, a shake up in the US market can be expected to dampen markets around the globe, so if you’re negative on the US, it’s hard to be positive on other markets.

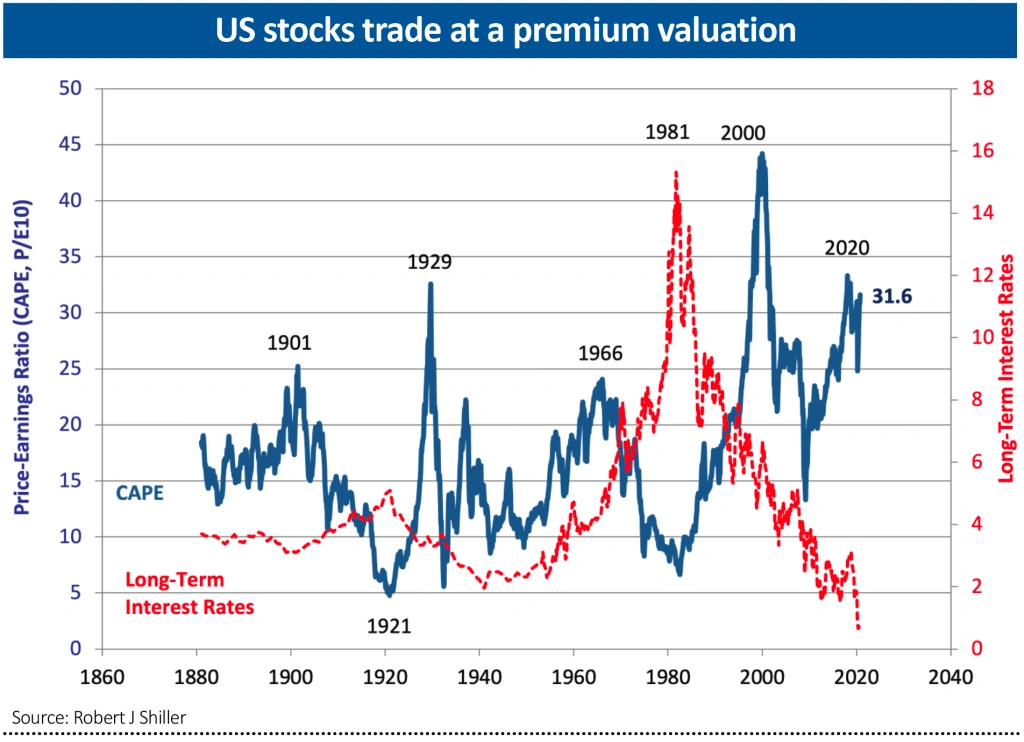

However the valuation of the US stock market is extremely elevated, according to the Shiller CAPE ratio, despite the pandemic wreaking havoc on global economic growth. It takes a brave investor to shrug that off and go overweight the US stock market, particularly seeing as that means putting over two thirds of your portfolio in US stocks.

Meanwhile the UK has at least been pretty badly beaten up and valuations look more reasonable. Things could get worse before they get better for the UK market however. A Brexit trade deal could strengthen the pound, which would dampen any returns from the international-facing blue chips of the FTSE 100.

That would be even more of a drag on US returns for UK investors though. More problematically, with the pandemic looking like it’s set to get a firmer grip over the winter, the cyclical industries in the UK market could continue to find themselves battling a weakening economic picture.

Investors needn’t pay too much attention to the weightings in the MSCI index, unless they’re overly concerned with performance relative to that particular benchmark, the investment equivalent of FOMO (fear of missing out).

DOWNSIDE RISK

What’s most important to investors is getting a decent absolute return without taking too much risk. In that regard there is some downside protection in the low valuation of the UK stock market, and some downside risk in the premium on US stocks. Any slip ups by the US tech titans in delivering growth will likely be punished harshly by the market.

Dividends are also still not a priority for US companies, which like to reinvest for growth, or return cash through share buybacks. The yield on the S&P 500 currently stands at a little over 2%, while on the FTSE 100 it’s getting on for 5%. That’s important for income seekers clearly, but UK growth investors can also take comfort from reinvesting those dividends year in year out to boost long run total returns.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.