Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat investors should do after the latest correction

October is often referred to as ‘the cruellest month’, as it tends to see more than its fair share of abrupt market sell-offs, including famously 1929 and 1987.

A study of the Dow Jones index going back to 1896 shows that volatility, as measured by the standard deviation of daily moves, is statistically much higher in October than in any other month. And with the whole of the UK in some form of lockdown, there is little reason for sentiment to improve much in November.

A MONTH AGO EVERYTHING LOOKED BRIGHTER

It was almost inevitable that, just as investors had begun to relax in September and life seemed to be getting back to something like normal – coronavirus cases falling, the world economy getting back on track, Europe having passed its stimulus bill and Democrat candidate Joe Biden the clear favourite to win the race White House – markets went into reverse last month and the FTSE 100 broke below its 5,800 ‘support’, plumbing the levels of late April.

There’s a theory that October’s volatility stems from the fact it falls just before the US presidential and mid-term elections, but even

taking only the first and third years of a presidential cycle it is still the most volatile month by some margin.

To be fair, the FTSE hardly had the bit between its teeth when the sell-off started: having rallied just over 50% from the 18 March low in a matter of eight weeks, it spent the summer repeatedly flirting with the 6,000-point level before settling into a 200-point range.

TECHNOLOGY RETURNS UNDER PRESSURE

Meanwhile, US indices like the S&P 500 and Nasdaq Composite had not just passed their pre-crisis levels but were making new all-time highs.

In fact it wasn’t that long ago that Apple shares were trading at $135, making it the most valuable company in the world with a market value of more than $2 trillion. Today they may trade 16% below their highs, but they are still above where they were a month earlier.

Is there worse to come? With the final shape of any Brexit deal still to be finalised, and the direction of the pound therefore still an unknown, it’s tempting to say wait and see.

What’s most interesting is that US tech stocks, which were seen by many as a ‘safe haven’ trade when volatility is rising, have failed to step up to the mark this time meaning there have been few hiding places.

IT’S BEGINNING TO LOOK A LOT LIKE [CHRISTMAS] LOCKDOWN

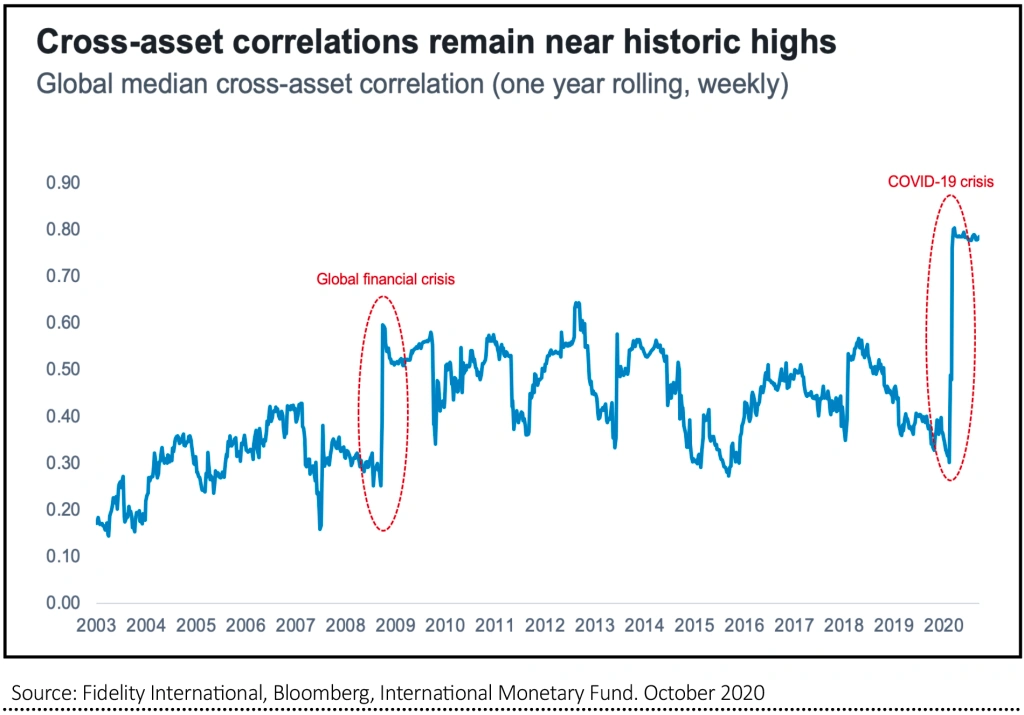

With France and Germany introducing emergency restrictions, several Spanish regions closing their borders, Wales and Scotland under localised controls and England back in a full national lockdown, surfing a second wave of infections could prove trickier than first time round. With the chart over the page showing how different types of investment asset are becoming increasingly correlated.

Like technology, many healthcare stocks have been priced for perfection in recent months and offer little in terms of ‘margin of safety’.

Banks may be cheap, and are having a moment in the sun as investors lick their lips at the prospect of (much-reduced) dividends from next year, but ultimately lending is a cyclical business and interest rates are not helping them.

Putting aside fewer provisions isn’t the same as growing, and if the housing market stalls there really is nothing to cheer about for them – or for the housebuilders, builders’ merchants or equipment

rental firms.

Travel and hospitality stocks are a no-go zone, with few exceptions, and energy stocks – like the banks, cheap but not very cheerful – are vulnerable to falling crude prices if industrial activity and global trade slows.

A ‘tin hat’ portfolio of supermarkets, tobacco, utilities and other ‘must-have’ rather than ‘nice-to-have’ products and services could be a sensible strategy, although these type of defensive stocks are often categorised as ‘value’ and are likely to get left behind in the event that the herd switches back to a ‘growth’ mentality.

DO NOT PANIC

In the final analysis, investors should consider one thing above all else. That is not being tempted to do too much, too quickly with their portfolios – the lesson from the sell-off in March was that anyone who crystallised losses by panic selling in March would have been kicking themselves three months later as stocks staged a rapid recovery.

It may also be best avoiding trying to pick stocks in such an uncertain environment and go for ESG (environmental, social, governance) funds, which have proven themselves to outperform in down markets as well as up markets, and capital preservation funds which aim to minimise the impact of volatility by owning a mixture of assets such as precious metals and bonds, alongside equities.

You could also consider holding a bit more cash than usual which, should provide some protection against further market volatility as well as giving you the opportunity to take advantage of opportunities when they come about.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.