Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow paying off debt can transform a company’s share price

Among the stock market’s most spectacular share price appreciation stories of recent years is Premier Foods (PFD). The cake, gravy and cooking sauces maker known for brands including Mr Kipling, Bisto, Ambrosia, Sharwood’s and Loyd Grossman.

Languishing at 19.4p in March, Premier Foods’ shares are now priced at 95p, having enjoyed a stunning re-rating thanks to improving earnings momentum as well as a transformational deleveraging of the balance sheet which combined to resurrect this erstwhile corporate zombie.

WHY PREMIER FOODS RE-RATED

Investors typically react positively to a material reduction in a company’s debt pile, as this usually de-risks the business, lifts strains on its cash flow and sometimes makes a group more desirable to potential suitors, a point which the 2019 takeover

of cheese and spread maker Dairy Crest by Canada’s Saputo helps to illustrate.

Dairy Crest’s 2015 sale of its loss-making dairies operations to Muller transformed the business, providing an exit from the troubled UK dairy industry, removing a considerable cash drain and also reducing leverage, making it a less problematic acquisition for Saputo to stomach a few years later in 2019.

Shares added Premier Foods to our Great Ideas list in April this year at a 41.45p entry price, drawing confidence from the positive momentum in the business and the share price alike. We had long held a bearish stance on the food producer due to a debt mountain and pension black hole which were huge factors in a lack of free cash flow; Premier Foods had become a lifeless zombie, unable to invest in its assets and competitive position.

Our interest followed a transformational pensions agreement that reduces future contributions and frees up cash for reinvestment in what is now a significantly de-risked business with the scope to start paying dividends in the future.

Combined with strong trading driven by marketing and innovation spend and a Covid-19 tailwind – lockdowns have stoked bumper demand for meal preparation items including cooking sauces, gravy and baking ingredients – this refinancing has completely turned sentiment towards Premier Foods around.

Results for the year to 28 March revealed trading profit at the top end of market expectations as well as a £62 million net debt reduction, lowering Premier Foods’ leverage ratio to 2.7-times, beating its previous 3-times target. And more recently, Premier Foods revealed (6 Oct) its intention to redeem £40 million of £130 million of outstanding bonds, in addition to an £80 million redemption completed in June. The move is expected to save up to £2 million a year in interest costs.

Shore Capital nudged up its estimates yet again following the news, while also pointing out that if Premier Foods’ 49% investment in Hovis is sold, ‘then Premier will deleverage further and quicker still, so augmenting the re-rating process’.

Who is your company being run for?

When interest rates are low and business conditions are healthy it is tempting for companies to add some debt to their business which amplifies returns on equity. If done in a prudent way debt financing can make good business sense, where it provides access to growth through investment in new capacity or acquiring a

new business.

The trade-off for shareholders is that some ‘interest costs’ are deducted from profits that otherwise would go to them in the form of dividends or better still in terms of growth, be reinvested in the business. Debt has the additional advantage of reducing taxes paid and increasing after-tax profits available for shareholders.

However, when companies go too far down the debt route, the relationship between shareholders and debt holders can become more confrontational. Bondholders are only concerned with getting the interest (also called a coupon) paid on time and having their capital returned. They don’t receive any benefit from growth of the business apart from potentially higher cash flows to better service debts.

Banks, creditors and bond investors are higher up the legal pecking order when it comes to bankruptcy proceedings, potentially leaving shareholders out of pocket. Even before it gets to that point, banks and bondholders can start calling the shots such as forcing management to abandon dividend payments.

An increasingly desperate management may be forced into raising more funds via shareholders, reducing their economic interests, if they don’t cough up their share of the funding.

Shares has screened for companies where it appears debt holders are calling the shots. We looked for companies where profits cover interest costs less than two times, net debt to equity above is 150% and the Altman-Score is below 1.2. This is a measure designed to predict bankruptcy.

Ignoring utilities and bus companies which generally run with higher debts because of perceived visibility of revenues, the most vulnerable companies on these measures are British airways owner IAG (IAG), office space company IWG (IWG), furniture retailer DFS (DFS) and hospital group Spire Healthcare (SPI).

THE IMPORTANCE OF FREE CASH FLOW

Smart investors love companies that produce plenty of free cash flow (FCF), which signals a company’s ability to pay down debt, pay dividends, buy back stock, and fund the growth of the business organically or via acquisition.

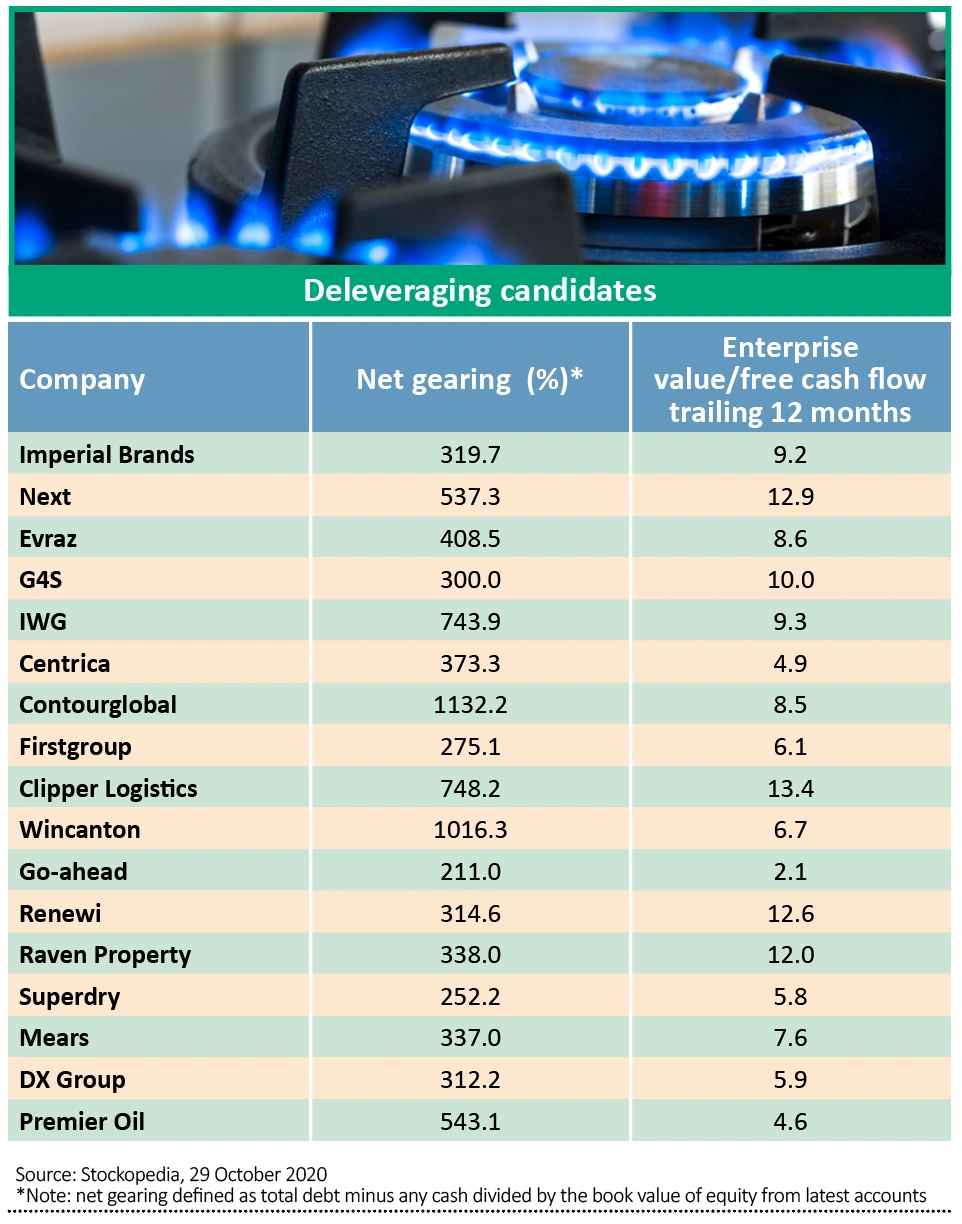

Investors searching for the next Premier Foods could begin by scrutinising the table, where we have compiled a list of companies that not only carry debt, but which enjoy material free cash generation that could enable them to pay borrowings down within a reasonable time frame.

However, it is very important to stress these should be considered candidates for further research not guaranteed winners. Cash flow can easily be interrupted if business takes a turn for the worse – which in turn could imperil firms’ ability to service their debts placing them at the higher risk end of the spectrum for investors.

Names in the list include the likes of tobacco manufacturer Imperial Brands (IMB), trading on a lowly forward price-to-earnings (PE) ratio of 4.7 and an 11.3% dividend yield according to Refinitiv data.

This combination of a low earnings multiple and a high yield implies the market is very sceptical over Imperial’s ability to maintain its profitability and cash flow, and thus its dividend-paying potential, over the long term, due to the regulatory pushback on smoking, increased public health awareness and disappointing sales from its next generation product (NGP) portfolio.

Another deleveraging candidate is Centrica (CNA), the British Gas-owner whose shares have more than halved from around 90p at the start of the year to 39.3p. At these levels, Centrica swaps hands for a grudging prospective price-to-earnings ratio of a shade over eight times prospective earnings for 2020 and 2021.

Tellingly, the shares rallied in July after Centrica agreed to sell its North American business, Direct Energy, in a $3.63 billion deal, to US energy supplier NRG Energy. Set to complete in the current fourth quarter, the disposal will significantly ease Centrica’s balance sheet borrowings – net debt rose 18% to £2.8 billion during the first half of the year, although free cash flow improved by 74% to £750 million – and make a ‘material’ contribution to its defined benefit pension schemes.

Also on a deleveraging path is Anglo-Dutch waste treatment firm Renewi (RWI), where first half trading and cash came in ‘materially’ ahead of management’s Covid-19 adjusted expectations.

Core net debt, excluding IFRS 16 lease liabilities, at the end of August amounted to €407 million, down by €50 million since the March year, which is encouraging. Furthermore, leverage is expected ‘to remain below 2.9 times as at 30 September 2020, with significant headroom against the adjusted covenant of 5.5 times’, according to Renewi, which also stressed that pandemic-induced ‘levels of customer insolvency have so far remained low’.

AND KEEP AN EYE ON

Other stocks with potential to deleverage balance sheets

include Mothercare (MTC), transformed from an ailing brick and mortar retailer into a global baby product brand manager, which remains in talks to refinance its outstanding debt, as well as the unloved NewRiver REIT (NRR), where asset disposals are helping the company to meet deleveraging targets.

Digital specialist fit fashion purveyor N Brown (BWNG), the business behind the JD Williams, Jacamo and Simply Be brands trading on multiple of forecast earnings.

A targeted reduction in debt is now ‘underway and continuing’ at N Brown, where chief executive Steve Johnson holds sway. Thanks to the retailer’s focus on cash generation, tight cost control, reduction in capital expenditure and the suspension of the dividend, together with a smaller debtor book, N Brown has ‘started its objective of reducing its level of indebtedness’.

In the six months to 29 August, net debt was reduced by 17.3% to £411.1 million, and management expects year-end net debt to be in the range of £380 million to £400 million. Though the dire retail backdrop means there could well be further pressure put on its cash flows, broker Shore Capital believes N Brown is ‘a comfortably liquid business and has remained so through a more than significant balance sheet shock’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.