Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy this newly-listed gold giant for lower risk and high rewards

Just like buses, two come along at once. No sooner had Canadian gold giant Yamana Gold (AUY) come back to the London market, another big player has joined the fray.

And while there is always risk with mining stocks, this one could be an even lower risk way to play the rising gold price, but still with the potential to offer excellent returns given its business model and the elevated gold price environment which doesn’t look like subsiding anytime soon.

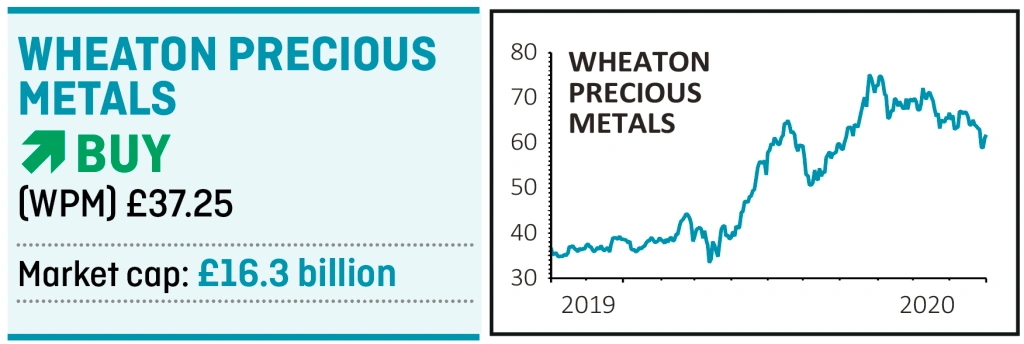

Wheaton Precious Metals (WPM) joined the London market in a secondary listing last week, accompanying its primary listing in Toronto and dual listing in New York.

The firm has taken full advantage of the rising gold price this year, and seen its shares in New York and Toronto gain over 60% year-to-date.

STREAM OF PROFIT

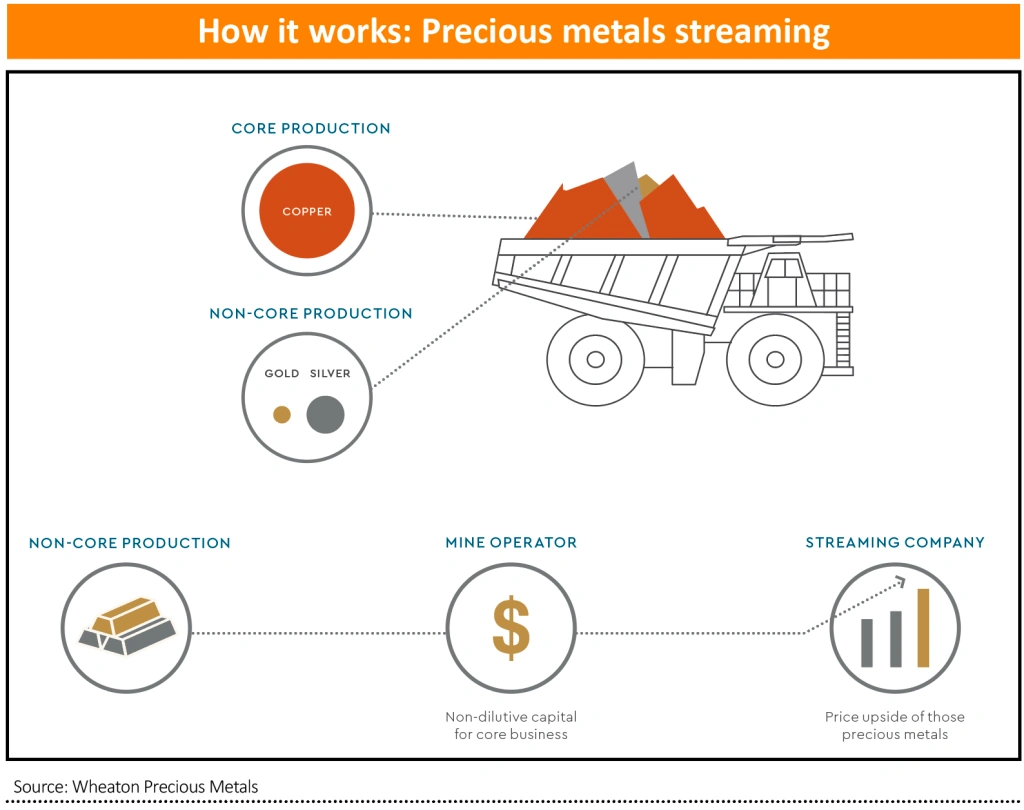

The £16.3 billion market cap company is a precious metals streaming company, meaning it provides money to miners to help them build their mines, and in return takes a percentage of what the mine subsequently produces, but doesn’t take on the risk of building and operating a mine.

The only other such type of company on the London market is Anglo Pacific (APF), but this is far smaller at a £195 million market cap and isn’t involved in commodities like gold and silver. It focuses on copper, nickel and zinc but still most of its money from coal.

Mining streaming companies generally don’t have the best reputation in the industry, and in the past have been seen as something of a lender of last resort, with desperate miners only turning to them if they can’t fund a project through an equity raise or bank debt.

But this is not the case with Wheaton at all. The company only partners with big players like Vale, the world’s largest nickel producer, for example or Glencore (GLEN), the FTSE 100 mining giant. Other partners include gold giants Newmont and Barrick Gold.

UNIQUE MODEL

It has a pretty unique business model which helps set it apart. Take its deal with Vale for example. Wheaton paid $3.1 billion to help it build the Salobo mine in Brazil, the country’s largest copper deposit. In exchange, Wheaton then takes 75% of the gold coming out of the mine (gold is a by-product of copper) at a price of $300 per ounce.

The benefit for Wheaton is obvious, given that under the terms of the deals it strikes it is allowed to then sell that gold at spot price, which at the moment is around $1,900 an ounce, meaning its gross profit margins can be huge.

In the new contracts it is signing with partners, Wheaton has agreed to buy gold off them at 20% of the spot price.

While in addition to being able to get money for a selling non-core asset and focus on producing copper, where the likes of Vale claw back some of the value is in how much they get Wheaton to pay upfront.

Speaking to Shares, Wheaton’s CEO Randy Smallwood says the company is ‘really focused on the technical side’, and when valuing a potential project has a team of geologists that ‘goes into projects, tears them apart and rebuilds them – then we come up with our vision as to what’s possible’.

He adds: ‘It’s a discounted cash flow model where we discount on political risk, corporate risk – how strong is our partner’s balance sheet – resource risk. We take all of that into account and then we try to come up with a dollar amount. And then the negotiations begin.’

Smallwood also emphatically rejects the idea Wheaton is

any way a lender of last resort, and says streaming is becoming a more mainstream way of financing for mining companies now.

He says, ‘When the mining company CFOs (chief financial officers) need to raise capital, everyone now considers streaming… We don’t have to do a lot of business development anymore.’

SHINING IN 2020

So far this year the company’s model has helped it take significant advantage of the rising gold price.

In the six months to 30 June Wheaton reported an operating profit of $212 million, compared to a $40 million loss in the same period last year, on the back of a higher realised gold price.

The company has low fixed costs (for example it employs around 40 people) and so was able to generate an operating margin of 42%. It also generated operating cash flow of $329 million, a 45% increase year-on-year.

Wheaton focuses on gold in particular as well as silver, but it also has small interests in cobalt and palladium, with the price of the latter in particular having soared in the past few years and up and around 25% in dollar terms this year. Overall Wheaton has 23 long-term purchase agreements with 17 miners across 30 mines.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.