Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAmazon: Can it keep winning as lockdown resumes?

There are not many stocks that can hold a candle to the staggering returns earned from Amazon and we continue to see the business as a long-term winner and a stock worth owning to benefit from the accelerating digitisation of society and the economy.

Over the past 10 years it has delivered an average 34.5% a year trouncing the meagre low single-digit average returns from the FTSE 100.

To put it another way, $5,000 invested in the shares a decade ago would now be worth more than $90,000.

If you had put five grand into the broader market your returns would be no match – something like $10,000 from the S&P 500. For UK investors, the FTSE 100 would have turned a £5,000 investment into just £6,850, based on Morningstar data, barely beating inflation.

The company has turned founder Jeff Bezos into the world’s wealthiest man, worth tens of billions.

Given the company’s sheer scale and track record, the company has a large retail investor following – it is the third most popular overseas stock on AJ Bell’s Youinvest platform, for example. That makes it natural for investors to wonder if Amazon can keep on growing robustly and continue to handsomely reward shareholders.

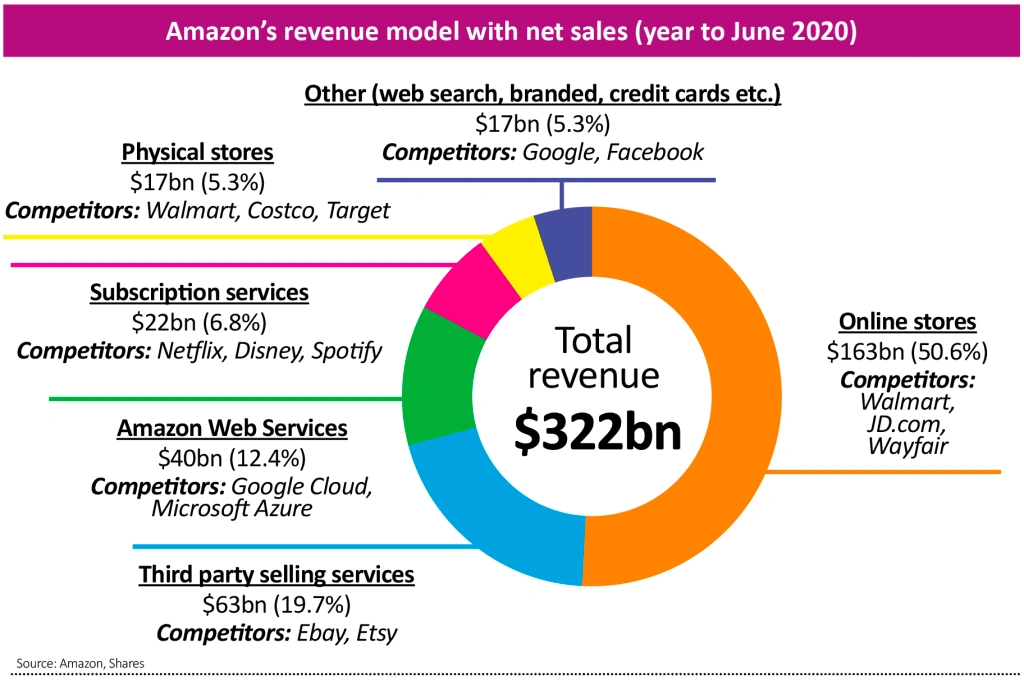

Without getting bogged down in the history, Amazon was set-up by Bezos in Seattle, US, in 1994 selling mainly books and CDs. It has since grown into one of the world’s biggest online marketplaces selling millions of products and providing various entertainment services, such as streaming TV, music and games. It also operates the largest cloud computing infrastructure business in the world, Amazon Web Services, or AWS for short.

Operating performance is split into three categories; North America, International and AWS.

A LOCKDOWN SUCCESS

There are few, if any, bigger winners from the Covid-19 pandemic, and leaving aside the obvious and ugly side of the virus, the world’s biggest online marketplace and cloud computing provider has made hay by the bale-load during 2020.

Third quarter 2020 revenues and earnings per share (EPS) topped $96.1 billion and $12.37, smashing estimates pitched at $92.5 billion and $7.38 respectively. Net income rose to $6.3 billion vs $2.1 billion in the same quarter a year before despite spending significant amounts on coping with the virus.

In total, Amazon has incurred more than $7.5 billion in incremental Covid-related costs in the first three quarters of 2020, and expects to run-up an extra up another $4 billion bill in Q4 as it bolstered staff numbers by 175,000 to cope with surging demand and manage social distancing rules.

Amazon has to balance large scale hiring with the health and safety of all its employees and ensuring that appropriate quarantine and sick pay is provided, said Alison Porter, co-manager of Janus Henderson Global Technology Leaders Fund (0771607).

‘Online delivery is becoming an essential service for the elderly and those self-isolating’, and more popular with the widespread introduction of social-distancing.

This was true before the pandemic and online shopping already had its claws sunk deep into consumer behaviour, but the virus has added jet fuel to pace of adoption. Pre-pandemic, just 16% of US retail sales were online, said Gary Robinson, manager of the Baillie Gifford US Growth Trust (USA).

‘To my mind, online shopping is clearly superior to bricks and mortar retail’, he said. ‘You get access to lower prices, better selection and is more convenient’, he said. So while online shopping had been already growing, ‘it’s been a slow and steady grind – that’s what lockdown changed’, said Robinson.

THE COST OF ONLINE SHOPPING EXPANSION

Amazon continues to invest heavily on fulfilment centres, TV shows and movies, grocery, AWS, India expansion and other areas. In India, the company is making massive investments (about $5 billion worth, according to some estimates) to build a logistics network that would cover the entire country. It also recently announced plans to ramp-up in Latin America.

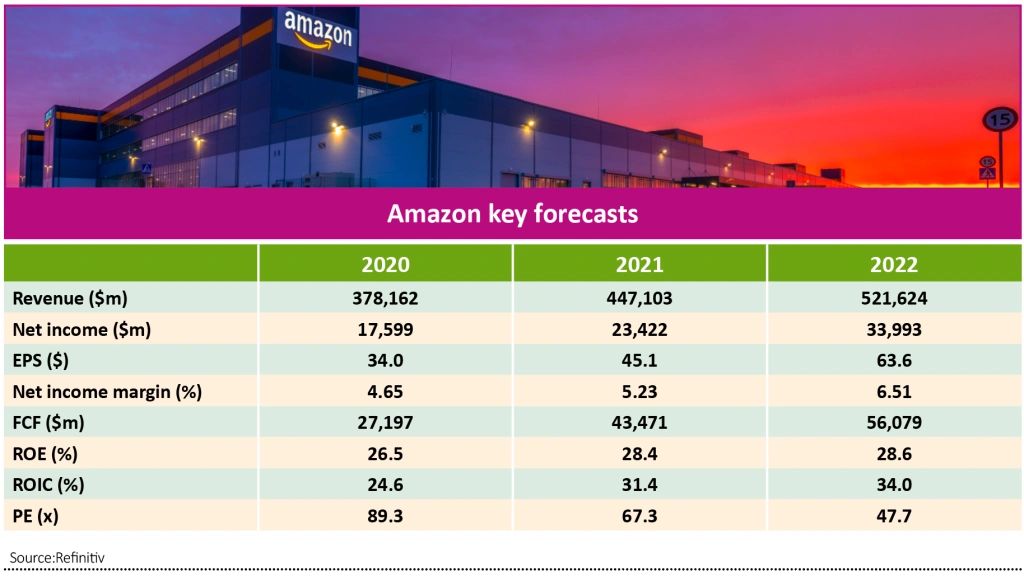

This is theory, should be great for revenue and possibly earnings, as it opens up its marketplace to hundreds of millions of new potential consumers. Last year’s $0.23 EPS is forecast to hit $0.33 in 2020, and rapidly increase to around $0.45 and $0.63 over the next two years.

‘The issue is the risk to those earnings as Amazon has a habit of deciding not to make money and returning to a very low level of profitability’, points out Richard Windsor or the Radio Free Mobile analysis website.

This is apparent in Q4 guidance where revenue expectations are ahead at $112 billion to $121 billion (mid-point $116.5 billion versus £116 billion forecast) but the earnings before interest and tax (EBIT) forecast range of $1 billion to $4.5 billion ($2.75 billion mid-point) is well behind Refinitiv consensus of $5.4 billion.

Running massive distribution and delivery networks is very expensive and most operators make precious little profit from them, Amazon is no different. This implies huge investment in staff and other network costs to meet demand could come at the cost of global margins.

Net profit margins have risen quickly since 2015’s 0.6%, but stalled last year at 4.1%, and it remains to be seen if 2020’s average 5.3% margin can be maintained given the huge investment. That said, starting from a low base means even small improvements in efficiency can have a big impact on profits.

This is exactly why Amazon has invested so much into drones and automated driving technology, to push down its biggest operating cost – staff salaries.

‘This is where the risk lies in Amazon and the shares are pricing in steady profit generation with no sudden slips,’ said Windsor.

However, analysis shows that Amazon’s historical income statement growth and balance sheet growth have diverged. ‘Revenue growth has paralleled asset growth; earnings growth has exceeded equity growth’, say analysts at Price Target Research (PTR), a Seattle- based firm.

According to their calculations, annual revenue growth has been 23.6% per year against 29.4% in total assets, while average annual EPS growth of circa 40% outstrips ‘equity growth of 27.5% per year’, they claim.

While PTR’s number crunching comes out lower than Morningstar’s 34.5% average share price return over the past decade, as we stated earlier, both figures are significantly below earnings expansion, which helps explain the PE compression from triple-digits in recent years.

‘With future capital returns forecasted to exceed the cost of capital, Amazon is expected to continue to be a major value builder’, said PTR’s analysts.

GROWTH ENGINE AWS

Amazon Web Services (AWS), its fast-growing cloud infrastructure business that helps massive customers like Facebook, Netflix, Twitter, Disney and multiple government agencies, saw revenue jump 29% to $11.6 billion from $9 billion, subscription services grew 32% year-on-year during Q3, the highest growth so far in 2020.

These two most recent quarters in the high 20s percent growth have followed four in the 30s and 10 in the forties, according to Megabuyte analyst Philip Carse, although he notes that that the incremental new revenues of $793 million was the second highest, eclipsed only by the $955 million added in the seasonally busy fourth quarter of 2019.

‘AWS represented 12% of Amazon sales but 57% of operating profit’, Carse calculates.

Subscriptions include annual and monthly fees from Amazon Prime members, plus audiobooks, digital video, digital music, e-books, and other non-AWS subscription services.

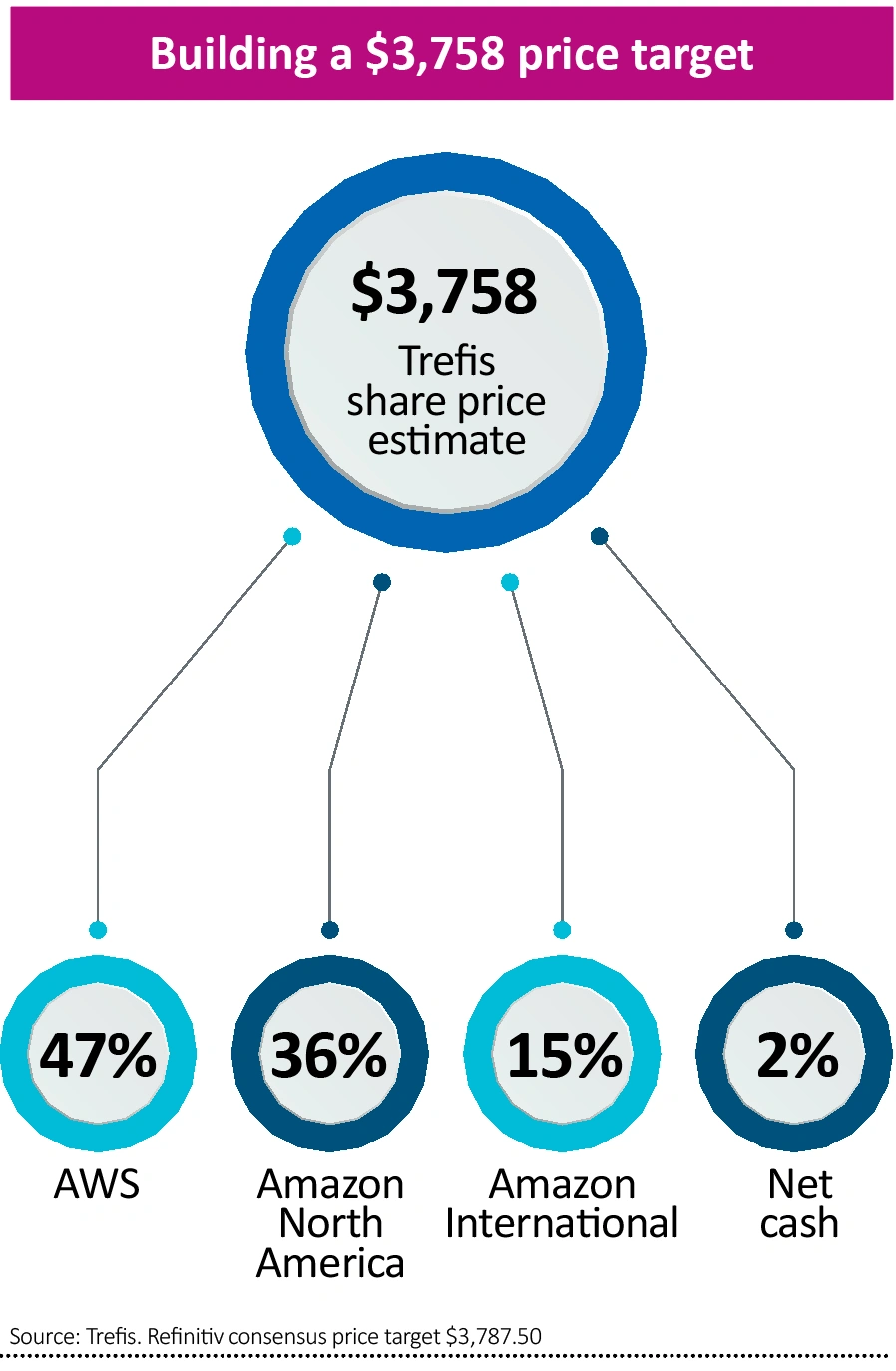

Yet despite a blowout quarter that steamed past forecasts the stock actually fell about 2% in after-hours trading on the day they were announced (29 Oct), implying a share price of $3,151.04.

This cuts to the chase of the investment decision that investors must grapple with; can Amazon keep up this type of growth and, is that enough to justify the valuation?

Amazon stock is currently changing hands on a next 12 months price to earnings (PE) multiple of 72.4, according to Refinitiv data, way above the 21.7 industry average.

Effectively, Amazon subsidizes the growth of its lower-margin North American unit and its unprofitable international retail operations with AWS’ profits. That’s the opposite of Alibaba’s business model, which subsidizes the growth of its unprofitable cloud business with its higher-margin core commerce revenue.

AWS profits enable Amazon to consistently sell its products at low prices while expanding its ecosystem with brick-and-mortar stores (including Whole Foods and Amazon Go), streaming media platforms, and cheap hardware devices.

All those efforts strengthen Amazon Prime, which surpassed 150 million paid members globally at the end of 2019.

Amazon Prime’s discounts, free shipping options, digital services, and other perks lock shoppers into its e-commerce ecosystem and prevent them from buying products from rival retailers. Therefore, Prime’s growth buoys the long-term expansion of Amazon’s online marketplaces, which still generate the lion’s share of its revenue.

‘I think the EPS story is going to accelerate; Q4 EPS could be nuts’, said Chaim Siegel in September, an analyst at US broker Elazar Advisors. Yet in the wake of the recent numbers his mood had changed. ‘I do think this is a great play for Q4 and stay-at-home but I no longer have the EPS upside to make this a buy’, he said.

Short-term pivots like this understandably create confusion for ordinary investors, which is why it is so important to take the bigger and longer-run picture into account given the hefty valuation.

Jeremy Gleeson, who has run the AXA Framlington Global Technology Fund (B4W52V5) since 2007, accepts that some technology businesses fail to warrant their inflated valuations, but that Amazon is not one of them.

‘Many of the firms we hold – even Apple and Amazon – are not mature businesses’, he said. ‘They are still in growth mode so their earnings are not yet at an optimal level. It’s the potential they offer that is exciting.’

OPPORTUNITIES FOR MORE GROWTH

‘We see two potential catalysts for shares over the next 12-month period, ‘ said Tom Forte of institutional research house DA Davidson, ‘stronger than expected operating results from the company’s cloud computing efforts, which we believe remains the primary driver of its share price and its increasing mix of highly profitable third-party sales’.

Healthcare is another area that could create substantial value in the years ahead after its 2018 acquisition of Pillpack, the online pharmacy and medication delivery service.

‘We see Amazon exiting Covid-19 with a much larger healthcare related effort, which could be a long-term driver of sales and profits’, said DA Davidson’s Tom Forte.

‘While the margins may appear low, it is the massive revenue base and continued growth that the market has continuously rewarded, and is likely to continue to do so.’

‘One of the most striking things to me is how early we are in digital transformation’, says Baillie Gifford’s Gary Robinson, and the opportunities for growth for years to come from well-funded, dominant businesses like Amazon are both large and long-term. Shares firmly believes that investors should have exposure to these trends and that Amazon is among the best stock selections to play this theme.

Amazon’s rivals profiled

Alibaba (BABA) $304.69

China’s answer to Amazon, and in some areas, its superior (such as a better digital blend between physical stores and online sales). Alibaba operates China’s largest e-commerce platforms Taobao and Tmall, and while it has expanded elsewhere in Asia, its enormous home market remains all-important. Ambitious plans include two billion users of its digital ecosystem by 2036 helped by savvy digital vertical investments into things like smart logistics, payment services, cloud computing, online marketing services, travel booking, music and video streaming. Listed in New York and Shanghai, the stock is substantially cheaper than Amazon on a PE of 28, although that likely reflects potential governance issues around its Chinese roots.

Ebay (EBAY) $47.63

A possible blast from the past, Ebay became a superstar stock during the dot.com era with its online auction platform but failed to keep up with growth hopes. Recent years have seen the company emerge to some degree from Amazon’s shadow with its own online marketplace, although its rate of growth remains miles behind its larger rival, illustrated by its discounted 12-month PE of just 13.

Mercadolibre (MELI) $1,214.05

Argentine online marketplace that has grown into the Latin American leader, becoming the first tech company from the region to list on Nasdaq in 2007. Lots of local expertise comes in handy across a region beset with transport difficulties from often poor infrastructure, which should give it a huge advantage over outsider rivals, including Amazon.

Shopify (SHOP) $925.43

Shopify is riding the illustrious e-commerce wave caused by the coronavirus, as more businesses have moved to online sales in 2020 than over past 14 years, according to one analyst, and Shopify has been able to make the most of this. The company runs tools across a platform that makes going digital super easy for retailers and other consumer-facing businesses, catapulting Shopify towards first ever profits this year. It’s been one of the best-performing stocks in an industry dominated by Amazon and since its $17 per share IPO five years ago its stock has soared 5,300%-plus, giving an eye-watering PE of 317.

Twilio (TWLO) $278.97

Operates in the UCaaS space, or unified communications as a service. This basically means enterprises to embed things like instant messaging, automated call answering, email and more into their own online operations easily, paying for Twilio tools on monthly subscription. The stock has jumped 170% so far in 2020 as the pandemic has supercharged the scramble from both old and new customers to update their operations for a new digital age. Any prospective investors would need a long-run view as it will take several years to grow into a PE currently at 2,700!

Funds to gain Amazon exposure

Janus Henderson Global Technology Leaders (0771607) £31.49

About 3% of the fund’s £1.16 billion of assets are tied up in Amazon stock, helping returns beat its Technology and Telecommunications Investment Association (IA) benchmark by nearly 12% over five years. Also a big investor in Alphabet, Apple, Microsoft and Facebook.

AXA Framlington Global Technology (B4W52V5) 799.2p

The £1.21 billion fund is run by Jeremy Gleeson, a popular choice with retail investors thanks to a track record of benchmark beating performance over three, five and 10 years. Its Amazon stake isn’t as large as some other funds, with approximately 2.3% of assets invested across a broad range of household names and less familiar stock, including Visa, PayPal, Apple and Qualcomm.

Baillie Gifford Long Term Global Growth (BD5Z0Z5) £11.46

A very popular pick with ordinary investors from the highly-rated Baillie Gifford stable. As the name suggests, suits those taking a five year view or more in the hunt for super-normal returns, Amazon is its second largest selection at 7.76%, and its longest running stake. Tesla remains its biggest bet, while Alibaba, Tencent and Shopify are also among its largest stakes.

Polar Capital Global Technology (B42W4J8) £60.99

Run by the respected Ben Rogoff/Nick Evans team at Polar, the fund’s performance has been knockout, smashing its benchmark over three and five years and returning more than 300% since 2015. It’s Amazon stake stands at 2.95% currently and sits alongside a who’s who of big capo tech names, including Apple, Alphabet, Facebook, Samsung, Alibaba and Tencent.

Natixis Loomis Sayles US Equity Leaders (B8L3WZ2) 368.51p

Like the Baillie Gifford vehicle, this fund makes a big play on Amazon’s future growth potential with 7.5% of its £1.45 billion assets in the stock, its biggest single stake. Another impressive five year performer, returning 149.4% from its mainly US-based portfolio. Alibaba, Nvidia and Visa also in the portfolio.

DISCLAIMER: AJ Bell is the owner of Shares magazine. Tom Sieber who edited this article and its author Steven Frazer own shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.