Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvestors finally get a steer on Novacyt’s earnings potential

Investors in diagnostics specialist group Novacyt (NCYT:AIM) have been treated to two important pieces of news.

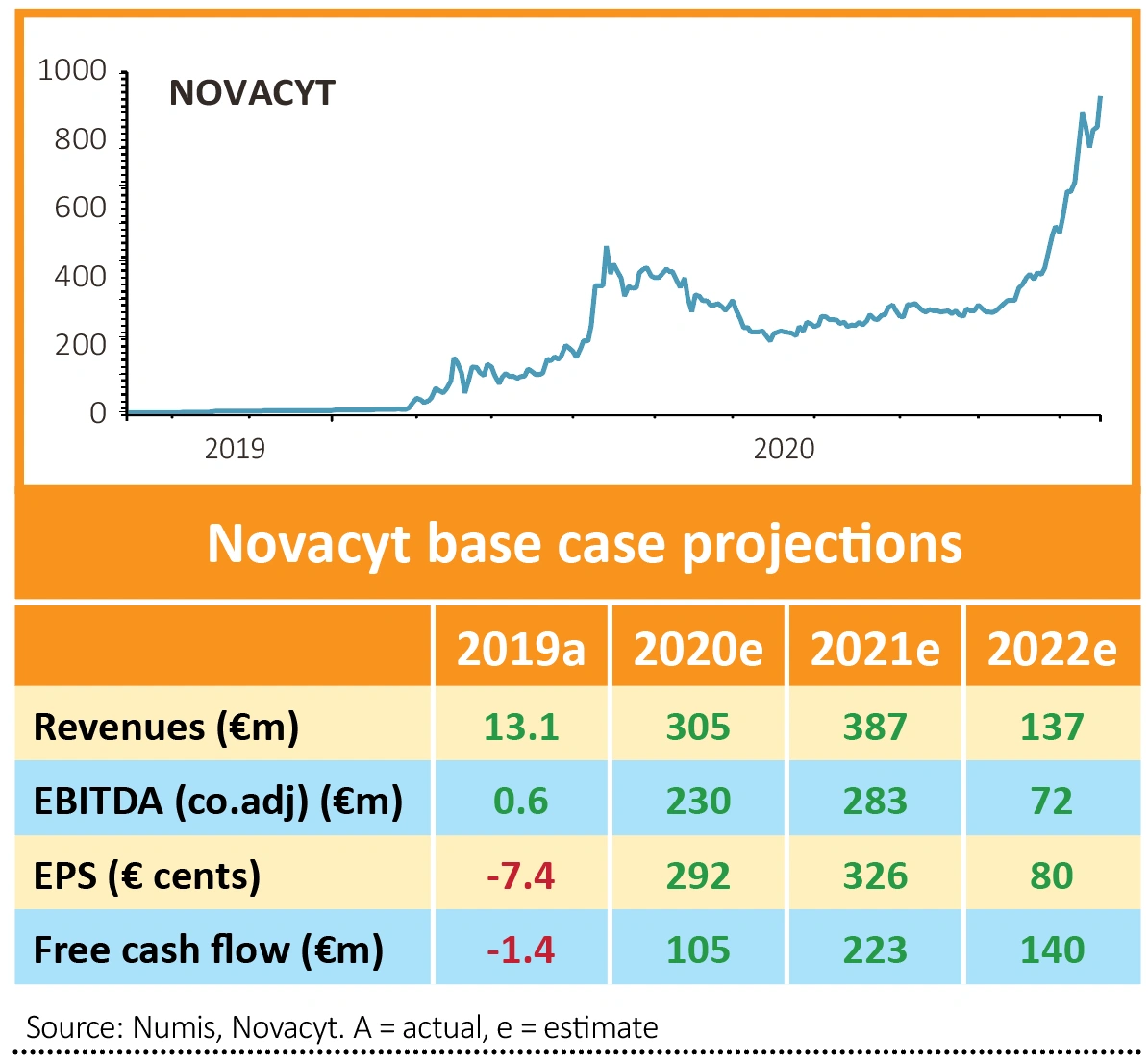

Earnings estimates are available for the first time since the company listed on AIM in 2017 after Numis starting research coverage on the stock, which has gone up by 7,190% in value this year.

Numis analyst Stefan Hamill believes Novacyt could emerge as a ‘long-term diagnostics winner’ based on a credible three-pillar strategy of organic, research and development, and accretive acquisitive growth.

Given the uncertain nature of when and if an effective vaccine becomes available, Hamill has modelled four scenarios labelled bear, base, bullish and blue-sky and then weighted them with the base and bullish cases each receiving 40% and the bear and blue-sky cases each getting 10%. The calculation values the business at £13.65 per share versus a 930p price at the time of writing.

Shares previously highlighted the possibility of a revenue cliff from 2021 as demand for testing abates and it should be noted that all of Hamill’s scenarios model for revenues and profits to fade by 2024.

In the base case, revenues reach €390 million in 2021 driven by testing demand growing during the peak flu months in the first half, before falling back to €81 million in 2024. Hamill estimates the shares are worth 950p in this scenario.

Bull case revenues reach €600 million in 2021 on the basis that the second phase of the UK Department of Health and Social Care (DHSC) contract is triggered and the blue-sky case has revenues of over €1 billion reflecting the contract hitting its maximum potential and Novacyt becoming a strategic supplier into the NHS. The bull case has the shares valued at £15, while the blue-sky value is £34.

Meanwhile the bear case factors in no upside from the DHSC contract with revenues forecast to reach €210 million in 2021 before slipping back to €41 million in 2024. The shares are expected to be worth 450p under this scenario, says Hamill.

The second piece of positive news was Novacyt’s acquisition of IT-IS International which is the exclusive manufacturer of its real-time polymerase chain reaction instrument range. The deal increases vertical integration and evolves the company into a broader diagnostic platform instrument and reagent manufacturer.

It gives the company end-to-end control of its near-patient testing system and increases the significant potential to win further contracts in decentralised settings such as the NHS and care homes.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

- The UK stock market has a new gold giant in town

- More to come from Touchstone despite doubling in price since the summer

- Very large earnings upgrades for Kainos

- Luceco knocks the lights out

- Ford shares start to motor after impressive third quarter trading

- This trust offers big potential if you believe value investing will thrive