Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to calculate enterprise value and when to use it

Enterprise value (EV) is often underappreciated by investors who tend to focus on the market value of a company. It is arguably a better way to value a business than market capitalisation (also known as market cap) because it takes account of debts, preferred shares, minority interest and cash.

Put simply, it is the value of the whole business, not just the portion financed by shareholders. In calculating EV, the former items are added to market cap while cash items are deducted.

This rounded view is why enterprise value plays a crucial role in takeovers.

WHY DO THE OTHER BITS MATTER?

If someone is looking to buy a business, they need to work out the sum of the liabilities to purchase 100% of a company’s cash flow.

Preferred shares pay fixed dividends and take legal priority over payments to ordinary shareholders. They are considered more like a debt instrument.

Minority interest refers to situations when a company owns less than 50% of a subsidiary. Someone looking to buy the parent company and control 100% of the cash flow would also have to buy out the other shareholders of the subsidiary.

Looking only at a company’s market capitalisation can sometimes give a misleading picture of the real size of a business. For example, energy supplier Centrica (CNA) has a market cap of £2.4 billion, but adding net debts of £3.5 billion brings its EV to £5.9 billion, two and a half times bigger than its market cap.

At the other extreme is engineering firm Costain (COST) which has a market cap of £108 million, but net cash of £140 million, giving the company a negative EV, implying the operating assets of the business are worthless.

Fantasy miniatures company Games Workshop (GAW) is an example of a business which doesn’t rely on borrowed money to operate. It generates a lot of cash and produces high returns on the operating assets it deploys, more than enough to maintain operations, invest in its future growth while also paying dividends to shareholders.

Therefore, Games Workshop’s market cap represents the true size of the underlying business. Market cap is calculated by taking the latest share count which can be found in the company’s annual report and multiplying by the latest share price, (33 million shares and £106 per share) resulting in £3.5 billion of value as determined by investors.

Whenever there is a change in the number of shares in issue, companies are required to update the market with the correction information, so investors are armed with the latest data to calculate the market cap.

USING ENTERPRISE VALUE

Enterprise value crops up most often in various valuation metrics such as EV to EBITDA and EV to sales ratios. The main advantage is that investors can make like-for-like comparisons of companies with different capital structures operating in the same industry. Using EV across different industries can give unreliable results because of different margins and capital requirements.

Private equity investors popularised the use of EBITDA during the leveraged buy-out boom in the 1980s. They used it as a proxy for cash flow when appraising acquisitions because it ignored non-cash items like depreciation and amortisation. This made cash flow look better and allowed investors to justify using higher amounts of debt financing.

However, depreciation is a real business expense which can be significant for capital intensive industries. Depreciation relates to capital expenditures which are required to maintain operations.

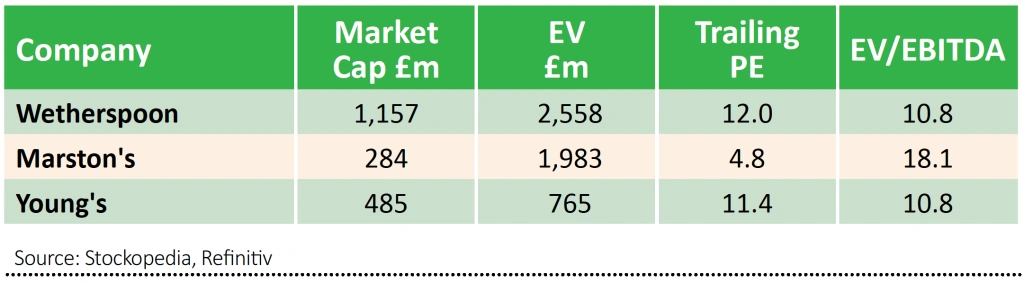

Let’s look at an example using EV to EBITDA and compare it with the traditional price to earnings ratio (PE). Pubs group Marston’s (MARS) looks cheaper relative to J D Wetherspoon (JDW) and Young’s (YNGA:AIM) on the basis of PE, but much more expensive through the lens of EV, because of the different financing structures.

The enterprise value for Marston’s is seven times its market cap compared to around two times for Wetherspoon and Young’s. All these groups have significant asset backing through ownership of freehold properties which must be acknowledged when looking at each company’s capital structure and debt.

Investors should be careful when using EBITDA in capital intensive industries. It can be better to use more traditional measures like net operating cash flow, which takes into account changes in working capital and capital expenditures.

Another sector where Investors need to apply some caution is when looking at certain software businesses, especially where a company capitalises development expenditures, rather than expensing them. The difference between EBITDA and cash flow can often be significant.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

- The UK stock market has a new gold giant in town

- More to come from Touchstone despite doubling in price since the summer

- Very large earnings upgrades for Kainos

- Luceco knocks the lights out

- Ford shares start to motor after impressive third quarter trading

- This trust offers big potential if you believe value investing will thrive